The ASX is fortunate enough to host many quality stocks that offer high dividend yields by international standards.

That’s no accident.

Australia’s rules that allow investors to reduce their income tax liability if the company has already paid corporate tax on dividends encourages this situation.

So which are some of the bargains offering more than 8% yield at the moment?

Here are two that have caught my eye:

40% discount to what the assets are worth

Growthpoint Properties Australia Ltd (ASX: GOZ), which is a real estate investment trust (REIT) that owns industrial and office properties, reported its latest results on Thursday.

High interest rates and the uncertainty in workers returning to the office are admittedly keeping the stock down, having lost 28.4% over the past year.

But that gives it plenty of cyclical upside. The stock is now trading at an almost 40% discount to its net tangible assets.

So buying Growthpoint shares now means you’re effectively becoming a landlord for far cheaper than if you bought those properties directly.

The depressed valuation also provides those willing to dive in now with a sensational dividend yield.

After Thursday’s announcement of a 9.65 cent distribution per share, the total payout for the last 12 months becomes 20.35 cents.

That equates to a yield of 8.85%.

A cheap stock paying 11% yield

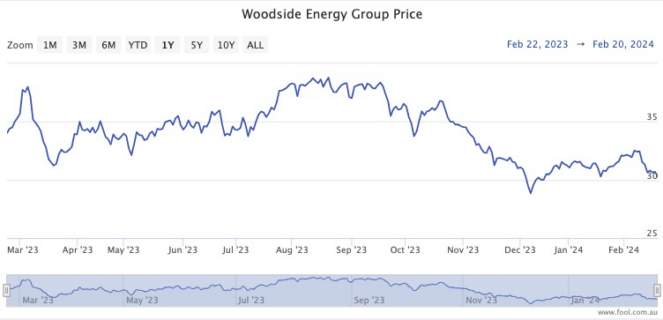

A riskier proposition, but potentially more rewarding, is Woodside Energy Group Ltd (ASX: WDS).

After a 12.2% drop in the share price over the past year, Woodside’s dividend yield now stands at a monstrous 11.1%.

Of course, the caveat here is that the fortunes for an ASX energy stock like Woodside is highly dependent on global oil prices.

If that plunges over the next year then the company may reduce the dividend.

Conversely, if the global crude prices rise then both the Woodside stock price and distribution payments could rocket.

A survey of professional investors on CMC Invest suggests many are comfortable with buying Woodside shares right now.

Eight out of 15 analysts rate the energy stock as a buy, while only three recommend selling.

The post 2 cheap ASX stocks that offer more than 8% dividend yields appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 10 November 2023

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- 5 things to watch on the ASX 200 on Thursday

- 3 ASX 100 and ASX 200 shares I’d buy now for a $1,820 passive income in 2024!

- 5 things to watch on the ASX 200 on Wednesday

- Is the 11.3% dividend yield on Woodside shares for real?

- 5 things to watch on the ASX 200 on Tuesday

Motley Fool contributor Tony Yoo has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Gk07Uo4

Leave a Reply