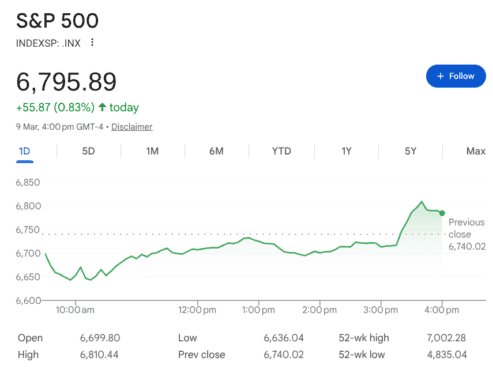

Good news: The ASX is up 7.4% over the past 12 months, plus probably somewhere around 4% more for dividends.

So let’s call it a total gain of 11.4%, give or take.

That’s better than the market’s long term average of just over 9% (depending on your source and the start date, but it’s about right over the past 120 years (per Credit Suisse / UBS) and the last 30 (according to Vanguard).

Beauty. Pop the champagne andâ¦

Oh? That’s not the news you’re seeing and hearing today?

You’re seeing something different? A lot of carry-on about a one-day fall?

Yeah, me too.

Which is kinda understandable, but alsoâ¦Â a little too short-term, I reckon.

Yes, big falls make news.

Yes, we feel the pain of losses two- or three times more than the joy we get from similar gains.

Yes, we worry that one bad day might lead to more.

Yes, sometimes that happens, and things get worse.

Yes, sometimes a lot worse⦠for a long time.

And yet.

And yet, the market is up over 11% over the past 12 months. Plus franking credits.

It is up 25% over the past 5 years, plus something like 20% more in dividends. (That’s 45%, close enough to 9% per annum, as as simple average. Less, compounded, but then you have to compound the dividends⦠so close enough for our purposes).

But that’s chicken-feed.

The Vanguard data I mentioned before?

9.3% per annum, on average, over the 30 years to 30 June 2025 (the most recent data available).

Or, if you prefer dollars rather than percentages (I do!), enough to have turned $10,000 into $143,000 (before fees and taxes).

You’d reckon that should be the headline story every day, right?

Now, the realists among you will reply with one of two thoughts. Either:

1. It wouldn’t be a headline because it’s taken 30 years to happen; and/or

2. No-one would click on it.

True, and true.

And yet, that is the far, far more useful and powerful stat, rather than worrying about what happened today.

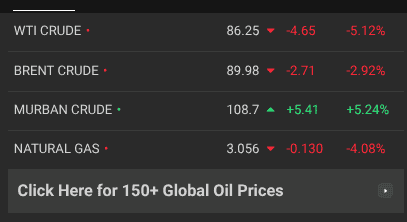

Here’s the other thing: yes, oil was up more than 28% in a single day earlier today. That is absolutely notable.

But here’s the other thing.

The headlines say ‘Oil over $100 per barrel for the first time since⦒.

The alternative headline? ‘Oil has cost less than $100 a barrel for every day in between’.

See, framing matters.

No, we’re not being taken for mugs (necessarily) by the headline writers. And they’re not wrong.

The clue is in the first three letters of the word ‘news’.

It’s not their job to provide long-term perspective. I mean, a little wouldn’t hurt, but again, the clue is in the name.

It’s our job, as investors, to bring the common sense. To bring the timeframe that’s all too often missing in the rest of the conversation.

The market probably fell 3% or more in a single day a few dozen times over the 30 years during which that 14-fold return occurred.

Each of those times would have felt scary, unsettling, and like they might be the harbinger of something worse.

Here’s the thing: sometimes they even were.

And yet, that 14-fold return was the long term return.

That is, as I’ve repeatedly written: astounding long term gains accrue despite, not in the absence of these sorts of things.

Not only that, but if you don’t remain invested, and try to guess when the next ups and downs will come, you risk missing out on those astonishing gains!

I can’t make investing anxiety-free. I can’t make the volatility go away.

I can’t tell you whether today’s falls will be a one-off, or the beginning of something worse.

And frankly, I can’t tell you if the future is going to look like the past, either.

But isn’t that the most likely outcome?

Every time the market fell, someone said ‘it’s different this time’. The circumstances might have been, but the outcomes never were.

So sure, maybe ‘it’s different this time’, but I doubt it.

Today’s falls aren’t fun. Losing money isn’t fun.

(There’s a silver lining if you’re still adding to your portfolio â prices are cheaper today! â but that doesn’t help if you’re in retirement and living off the proceeds of your portfolio.)

Tomorrow?

I have no idea what it’ll bring. Maybe things get worse. Maybe they bounce back.

The same for the next week, month and year, for that matter.

But over the long term? Well, unless we’ve hit peak human ingenuity, I suspect the market will be higher in 5 years, much higher in 10 years, and higher again in 20 and 30 years.

And if that’s true, obsessing over daily, weekly, monthly or even yearly falls is understandable⦠but not very productive.

I can’t make the process easy to endure, unfortunately, but I suspect that endurance will pay off handsomely.

My best advice? Learn from history, then keep your eyes on the horizon.

And I reckon the future is bright.

Fool on!

The post The good news you won’t read today â but really should appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right nowâ¦

* Returns as of 20 Feb 2026

.custom-cta-button p {

margin-bottom: 0 !important;

}

More reading

Motley Fool contributor Scott Phillips has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.