Predicting what any share market â whether that be the S&P 500 Index  (INDEXSP: .INX) or the S&P/ASX 200 Index (ASX: XJO) â will do even tomorrow is a big ask. But predicting what the markets might do in a month or year’s time is a devilish task indeed.

But that hasn’t stopped a few ASX experts from giving it a crack.

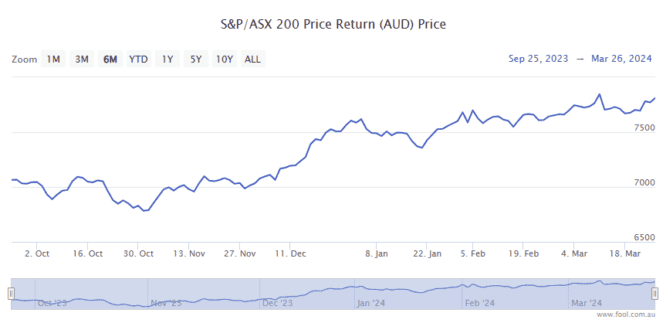

Investors all around the world are probably fairly content bunch as we close out the month of March 2024. Both the American and Australian stock markets have been rising steadily over the year to date. As it stands today, the ASX 200 has gained a decent 2.3% this year, hitting a new all-time high in the process.

The S&P 500 has done even better. Not only has the flagship index of the United States markets hit new all-time records of its own, but it’s climbed a happy 9.7% over the year so far. Not bad for three months; work.

And one expert reckons the S&P 500 might climb even higher. According to a report in the Australian Financial Review (AFR) today, analysts at investment bank HSBC have just lifted their S&P 500 forecasts.

HSBC now reckons the S&P 500 will hit 5,400 points by the end of 2024. If this does come to pass, it would see the index gain another 3.8% or so from where it is today, and hit even loftier record highs.

What’s next for the S&P 500 Index?

This target is based on an expectation of higher company earnings, resilient GDP growth and positive sentiment. However, it also assumes that US interest rates will start coming down this year. Here’s some of what the HSBC analysts said in a note:

Our target is predicated on the [Federal Reserve] cutting rates in June with 75 basis points of total cuts in 2024, in line with consensus and Fed expectations based on the recent dot plot…

We expect a more volatile second half of 2024 on US elections, elevated earnings expectations, and a shifting narrative from ‘when’ to ‘how much’ the Fed will cut.

That is HSBC’s base case scenario. However, the bank also had a ‘bull case’, which would see the S&P 500 limb to 5,700 points. For this to happen, the bank reckons we would need to see “above-trend GDP growth but with inflation remaining subdued”.

In addition, HSBC does warn that if the US economy runs “too hot” this year, it could result in higher inflation and no rate cuts. Under this bear case, HSBC sees the S&P 500 finishing 2024 at just 4,800 points.

The divergence of these three scenarios just goes to show how difficult it is to predict what might happen with a broad-market index like the S&P 500. But whatever this index does over the rest of 2024 will almost certainly have implications for our own ASX.

The post Expert: This is where the S&P 500 is going next appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 1 February 2024

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- Why ASX 200 investors are celebrating today’s Aussie inflation print

- 5 things to watch on the ASX 200 on Wednesday

- Here are the top 10 ASX 200 shares today

- 5 things to watch on the ASX 200 on Tuesday

- Here are the top 10 ASX 200 shares today

HSBC Holdings is an advertising partner of The Ascent, a Motley Fool company. Motley Fool contributor Sebastian Bowen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended HSBC Holdings. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Nf1qwvo