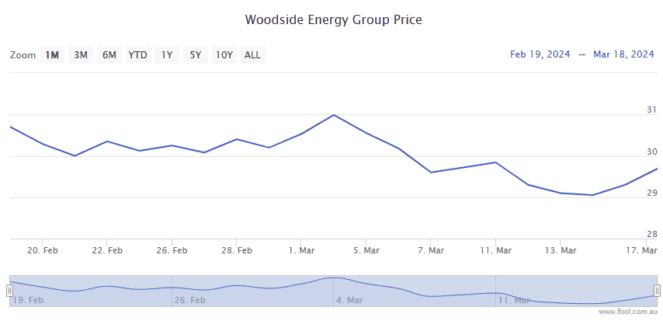

The Woodside Energy Group Ltd (ASX: WDS) share price is marching higher again today.

If the S&P/ASX 200 Index (ASX: XJO) energy stock holds these gains by close, it will mark four days of gains out of the last five trading sessions.

Shares closed up 2.3% yesterday and are up 1.2% as we head into the lunch hour today, trading for $30.62 apiece.

That sees the Woodside share price up 6.0% since last Wednesday’s close.

For some context, the ASX 200 is down 0.2% over this same time.

Here’s what’s been piquing investor interest.

Why is the Woodside share price running hot?

Investors tend to buy Woodside stock when energy prices are on the rise. And sell when energy prices are falling.

Over the past week, as you can likely guess by the strong performance of the Woodside share price, the oil price has reached levels not seen since late October.

Brent crude oil is trading for US$87.10 per barrel today, up from US$81.92 per barrel last Wednesday.

At US$ 83.12 per barrel, West Texas Intermediate (WTI) crude is also at its highest levels since October.

The big spike in oil prices follows a series of Ukrainian drone attacks on Russian oil refineries.

According to JPMorgan Chase & Co (courtesy of Bloomberg), the drone attacks have knocked 900,000 barrels per day of Russia’s refinery capacity out of action.

Adding to the potential supply-side crunch, Iraq has announced it intends to cut oil exports over the next months. This is to make up for producing more than it had agreed to in January and February under production limits with OPEC+.

And according to Jeff Currie, chief strategy officer of energy pathways at Carlyle Group, the oil price â and by connection the Woodside share price â could run significantly higher from here.

That’s based on the assumption that the US Federal Reserve will begin reducing interest rates in 2024.

Should that eventuate, Currie believes the oil price will run significantly higher than consensus expectations of US$70 to US$90 per barrel this year.

“I want to be long oil and the rest of the commodity complex in this environment,” he said.

Pointing to Europe’s replenishing its oil stockpiles and China’s efforts to boost its manufacturing sector, Currie said, “The upside here is significant.”

The post Up 6% in a week, why is the Woodside share price running hot? appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 1 February 2024

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- 5 things to watch on the ASX 200 on Wednesday

- Buy Woodside shares and these ASX 200 dividend giants now

- 5 things to watch on the ASX 200 on Monday

- Buying 350 Woodside shares in an empty investment portfolio would give me a $760 income in year one

- 5 oversold ASX shares to buy in March 2024

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/tSCBfM4