Aussie investors are lucky in that we have a lot of quality S&P/ASX 200 Index (ASX: XJO) shares to tap for passive income.

Unlike many international markets, many ASX 200 shares also pay out fully franked dividends. That means most investors should be able to hold onto more of that welcome cash when it comes time to pay the ATO their dues.

And there’s a lot of passive income on the table.

How much?

According to the latest Global Dividend Index from Janus Henderson, global companies paid a whopping US$339.2 billion (AU$512 billion) in the first quarter of 2024 (Q1 2024).

That’s up 2.4% from Q1 2023 on a headline basis, driven by underlying growth of 6.8%.

In a promising sign, the report also notes that 93% of companies across the world that paid a dividend in the first quarter either maintained or increased their payouts.

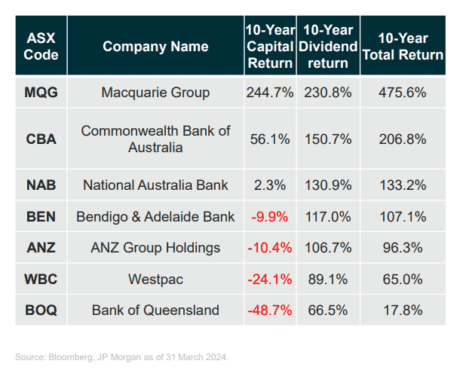

Bank stocks were the star players (and payers). With elevated interest rates across most of the developed world, the dividends paid by banks leapt 12.0% year on year in Q1,

So, how did ASX 200 shares stack up?

Q1 dividend growth for ASX 200 shares

Janus Henderson reported that Australian companies continued to dominate Asia Pacific dividend payments, making up 75% of the total. And I should note here that it’s not just ASX 200 shares that pay dividends. A number of smaller ASX stocks also contribute to the passive income pile.

The dividends paid by Aussie companies increased by 2.0% in Q1, trailing the 2.4% global growth figure.

That lag is largely due to a 20% interim dividend cut by the biggest ASX 200 share, BHP Group Ltd (ASX: BHP).

Janus Henderson noted that excluding BHP, ASX dividends would have enjoyed double-digit growth.

As with the global banks, the second biggest ASX 200 share, Commonwealth Bank of Australia (ASX: CBA), was a star dividend performer. CBA reached ninth place in the world for its dividend payouts in the first quarter. CBA was the only big four bank to make the top 20 global dividend payer list.

Commenting on the dividend growth, Matt Gaden, head of Australia at Janus Henderson Investors said, “The resilience of the Australian share market was evident over the quarter as it recorded healthy dividend growth despite the pressures on commodity prices and the mining sector.”

Gaden added:

The big four banks remain dividend darlings, showcasing the important role that they play for Australian investors.

Overall, global economies continue to face inflationary headwinds and the cost of capital is tipped to stay higher for longer.

But with a wave of government money coming into renewable energies and new opportunities are unlocked by AI technology, dividend investors are urged to remain aware of how these forces will impact global dividends over the medium to long term.

Now what?

As to what kind of passive income investors can expect from global and ASX 200 shares, Janus Henderson continues to forecast underlying growth of 5.0% for 2024.

That will see global companies shell out an eye-watering US$1.72 trillion (AU$2.6 trillion) in dividends over the year.

The report noted that lower special dividends mean the headline increase is set to be 3.9% year-on-year, equivalent to a rise of 5.0% on an underlying basis.

The post Global companies just paid a record $512 billion in Q1 dividends. Here’s how ASX 200 shares stacked up appeared first on The Motley Fool Australia.

Should you invest $1,000 in Bhp Group right now?

Before you buy Bhp Group shares, consider this:

Motley Fool investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Bhp Group wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

And right now, Scott thinks there are 5 stocks that may be better buys…

See The 5 Stocks

*Returns as of 5 May 2024

More reading

- ASX 200 bank shares: How dividends offset poor capital growth over 10 years

- Should you buy BHP shares after recent weakness?

- 5 things to watch on the ASX 200 on Friday

- Here are the top 10 ASX 200 shares today

- Beaten-up ASX 200 stock surges 12% on buyout rumour

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.