Microcap ASX mining share Korab Resources Limited (ASX: KOR) is rocketing higher today.

Korab Resources shares closed Friday trading for 2.7 cents and are currently trading for 3.4 cents apiece, up 25.9% after earlier posting gains of more than 30%.

So, whatâs driving investor interest in this tiny ASX mining share?

Why is the Korab Resources share price leaping higher?

Korab Resources shares are off to the races today after the ASX mining share reported its exploration license for a 172 square kilometre tenement in the Northern Territory was renewed through to 31 July 2024.

The tenement forms part of the Batchelor Project, located 70 kilometres south of Darwin.

The ASX mining share is likely leaping higher as the Bachelor Project hosts lithium mineralisation, with lithium star performer Core Lithium Ltd (ASX: CXO) among the miners owning and operating neighbouring tenements.

Investors are keeping a keen eye on developments in the lithium space, with demand for the lightweight, conductive metal widely forecast to remain strong over the coming decade amid a surge in global EV production.

In todayâs release, Korab Resources noted:

At the nearby Litchfield Pegmatite Belt, and the Finniss Lithium Project, lithium-bearing pegmatites are found within the same Burrell Creek Formation adjacent to and within aureole of I-type and S-type granites as the source of LTC pegmatites.

The ASX mining share said the geological setting of the broader Batchelor Project, and within its newly renewed tenement lease, is broadly similar.

Atop lithium, the tenement also has the potential to host rare earth oxides mineralisation. Korab said it has commenced a review of the existing exploration data. The results of that review will be reported as they become available.

How has this tiny ASX mining share been tracking?

As a microcap stock, trading in Korab Resources tends to be thin. The ASX mining share is also prone to some large price swings.

With more of those swings in the positive direction than negative over the past full year, Korab Resources shares are up 70%. That compares to a 12-month loss of 7% posted by the All Ordinaries Index (ASX: XAO).

The post Guess which tiny ASX mining share just rocketed 30% on lithium news? appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

See The 5 Stocks

*Returns as of August 4 2022

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- Down 20% in 2022, is the Lynas share price too cheap to ignore?

- Here’s why the Nickel Industries share price is racing 7% higher

- The AGL share price has tumbled 16% in a month. What’s next?

- Why this top broker is tipping 17% upside for the Telstra share price

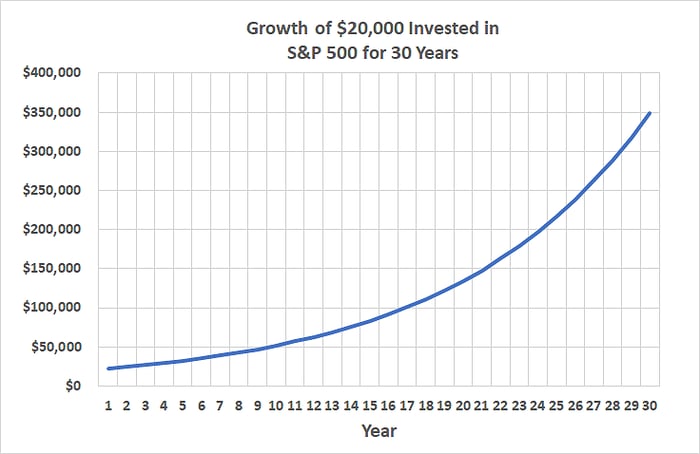

- Investing in the stock market could turn your $20,000 into $350,000. Here’s how

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/A436Byp