Motley Fool Australia Chief Investment Officer Scott Phillips joined Michael Thomson for Nineâs Late News on Monday night to discuss the likely rate rise, courtesy of the RBA, plus a nice jump for new S&P/ASX 200 Index (ASX: XJO) additions and the outlook for markets.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Scott Phillips has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/rBFKZj8

Following a strong 12 months of business activity, shareholders of ASX-listed companies are now set to be treated to an aggregate $42 billion in dividend payouts in September.

This follows on from a similarly pricey $45 billion collective payout back in December 2021.

The moves signal a strong period of corporate earnings for Australian listed companies, with members of the S&P/ASX 200 Index (ASX: XJO) in particular boasting record dividend payout margins.

Announced share buybacks were also amongst the highest on record as companies seek to return capital to investors en masse this year.

What’s this mean for inflation?

There’s no doubt everyone’s heard of â or felt in their wallets â the latest pandemic, that is inflation, that continues to grip the economy.

The Reserve Bank of Australia (RBA) has taken measures to clamp surging prices by increasing its key policy interest rates for the first time in years.

With that, it hopes to rein in the level of discretionary spending, credit creation, and financial asset growth in Australian markets, thereby slowing price growth.

However, a $42 billion cash injection isn’t exactly conducive to its plans.

Thankfully, not all of the capital being returned to shareholders through dividends will arrive directly into their brokerage accounts.

Some will be directly reinvested back into buying additional shares or funding additional investments, either by design or investor choice.

Another chunk will go to fund the balance sheets of retirees who use annuity-style instruments like dividends as income-producing assets to match their annual liabilities.

However, the transfer of wealth from corporate to residential and institutional Australia comes at a time when spending is on the RBA’s and the government’s radar. Certainly, there’s a good chance a portion of the proverbial cheque will be spent in the real economy.

Exactly where and to what sectors the income will flow is anyone’s guess.

However, given that a good portion of the dividend-paying shares are also tied up ‘escrow’, in vehicles like superannuation funds for instance, the impact mightn’t be as severe as it appears.

Keep in mind, the two largest companies in the world by market value, Saudi Aramco and Apple, recently released their figures. Saudi Aramco posted second-quarter net profit of $48.4 billion while Apple paid a Q2 2022 quarterly dividend of $27 billion alone.

Closer to home, the overarching impact of Australia’s dividend payout figure remains to be seen. In any case, experts are predicting interest rates will continue to rise until inflation cools.

Before you consider S&P/ASX 200, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and S&P/ASX 200 wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor Zach Bristow has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Apple. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended the following options: long March 2023 $120 calls on Apple and short March 2023 $130 calls on Apple. The Motley Fool Australia has recommended Apple. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/u3JoEQg

The infringement endangered Aussie Broadband’s own customers’ lives as the IPND is used by the Triple Zero service to locate people in emergency situations.

The database is also used by the Emergency Alert Service to communicate to residents in areas affected by natural disasters.

‘Alarming’ failure in software

ACMA chair Nerida O’Loughlin said Aussie Broadband’s failure was “unacceptable”.

“While we are not aware anyone was harmed due to the breaches, it is alarming that Aussie Broadband did not have effective processes in place to identify that its customer information was not being provided for over six months.”

The industry watchdog has directed Aussie Broadband to continue to comply with the IPND rules or risk court action that could result in penalties of $250,000 per breach.

“While the breaches should not have occurred, we are pleased to see Aussie Broadband moved quickly to upload the missing data once it was brought to its attention and has taken steps to comply in future,” said O’Loughlin.

Aussie Broadband boss apologises

Aussie Broadband managing director Phillip Britt apologised for the error and accepted the penalty.

“Whilst we had several checks and balances in place, these did not go far enough and Iâm confident that our new compliance checks will ensure this never happens again,” he said.

“We are deeply sorry that this software failure went undetected leading to inaccurate records in the IPND database.”

Aussie Broadband stated that it has now “implemented further redundancy measures, error notifications, independent monitoring and regular audits” to comply with the IPND rules.

According to the ACMA, it is on an “ongoing campaign” to improve the quality of the data in the IPND to better protect the public.

The watchdog has taken action against 30 telecommunications companies since 2018 for breaching IPND rules, resulting in almost $4 million fines.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Tony Yoo has positions in Aussie Broadband Limited. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Aussie Broadband Limited. The Motley Fool Australia has recommended Aussie Broadband Limited. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/9nW5BfO

But before these dividends can be paid, companies must first determine which investors are entitled to their upcoming dividends.

To do so, they set a cut-off date, which is also known as the ex-dividend date. If you buy shares on or after this date, those shares wonât come with the latest dividend payment.

On Wednesday, tomorrow, nine companies in the S&P/ASX 200 Index (ASX: XJO) will see their shares turn ex-dividend.

In other words, today will be the last day to secure the latest dividends from these ASX 200 shares.

Letâs check them out, starting with the company with the highest trailing dividend yield.

Upcoming dividend: 13.7 cents Franking: 100% Payment date: 22 September DRP: No Trailing dividend yield: 5.7%

The ASX 200 energy share recently announced its half-year results, posting a 218% surge in underlying NPAT on the back of strong refining margins. As a result, Viva brought forward its refining dividends, including them in the interim dividend instead of the final dividend.

Upcoming dividend: 6 cents Franking: 100% Payment date: 21 September DRP: No Trailing dividend yield: 4.4%

Progress in its sustainable improvement program and an upswing in COVID-related demand helped Healius to double its underlying NPAT in FY22. Across the full year, the ASX 200 healthcare share lifted total dividends by 21%.

Upcoming dividend: 7.3 cents Franking: 100% Payment date: 29 September DRP: No Trailing dividend yield: 3.7%

The ASX 200 health insurer served up 9% growth in underlying NPAT in FY22, helping the company to raise its full-year dividends by 6% while also marginally reducing its dividend payout ratio.

Upcoming dividend: 12 US cents Franking: 35% Payment date: 13 October DRP: Yes Trailing dividend yield: 2.6%

Bramblesâ FY22 results came in ahead of guidance as revenue climbed by 9% and NPAT jumped 18% on a constant-currency basis. The ASX 200 supply chain business boosted its total dividends by 11% compared to the prior year and has reinstated its DRP.

Upcoming dividend: 38 cents Franking: 100% Payment date: 7 October DRP: No Trailing dividend yield: 2.5%

The ASX 200 insurance broker posted NPAT growth of 14% in FY22, underpinned by organic growth in its Australian broking and agencies segments. But despite the rise in profits, AUB held its full-year dividends steady in light of its potential $880 million acquisition of Tysers. Subject to final regulatory approvals, the acquisition is on track to be completed by late 2022.

Upcoming dividend: 21 cents Franking: 100% Payment date: 4 October DRP: No Trailing dividend yield: 2.1%

Across the financial year, SEEK raised its total dividends by 10% as underlying NPAT from continuing operations soared by 81% in FY22. The ASX 200 share experienced record job ad volumes in the Australia and New Zealand (ANZ) region and volume growth across all markets in Asia.

Upcoming dividend: 13.5 cents Franking: 14% Payment date: 29 September DRP: No Trailing dividend yield: 1.0%

Finally, IDP experienced a strong rebound in demand in FY22 after previously being bogged down by COVID-related challenges. The ASX 200 education business grew revenue by 48% while adjusted NPAT shot up by 120%. This helped the company lift its full-year dividends by 10% compared to FY21.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Cathryn Goh has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Idp Education Pty Ltd. The Motley Fool Australia has positions in and has recommended Amcor Limited. The Motley Fool Australia has recommended Austbrokers Holdings Limited and SEEK Limited. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/DiNWU4L

The AMP Ltd (ASX: AMP) share price has put on a disastrous performance over the last few years. Indeed, it has dumped 77% of its value in just five years. But the S&P/ASX 200 Index (ASX: XJO) company looks a touch shinier now.

AMP posted a $117 million underlying after-tax profit for the first half of 2022 â down 24.5% on that of the prior period.

Of that, $46 million was brought in by AMP Bank â down 45% year on year. Its wealth asset management businesses, meanwhile, brought in a combined $53 million, marking a 17% drop.

Richards continued:

While recent asset sales may provide a payout boost to shareholders in the short term, they remove a key growth component from the companyâs business strategy.

The expert concluded by noting his belief that recovering AMPâs lost scale will likely demand âsignificant reinvestmentâ. Thus, he labels the stock a sell.

The last few years have been rough on the AMP share price, but the stock is outperforming year to date. It has gained 13% since the start of 2022 and is currently trading 2% higher than it was this time last year.

For comparison, the ASX 200 has dumped 10% year to date and 9% over the last 12 months.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Brooke Cooper has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/a28JqVg

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

With the market in a jittery mood thanks to ongoing inflation, interest rate hike mania, and geopolitical instability, nobody can blame investors who are wringing their hands anxiously in anticipation of a potential market crash. Thankfully, the chances of a crash happening are too difficult to determine with any certainty, so it doesn’t make much sense to worry at any particular time.Â

That probably isn’t very reassuring. But what will be reassuring is if you have a plan for what to do and what not to do in the event of a crash. For now, let’s work on three things you definitely shouldn’t do if there’s chaos in the market.

1. Sell your stocks in a panic

The first (and most important) thing you shouldn’t do if the stock market crashes is to sell all of your stocks to try to avoid experiencing any further losses. The problem with panic selling is that it feels like the right move. After all, if you can cut your losses fast enough, the market’s downward move to the tune of 30% might only lead to losses of 10% for you.

Selling eases the sense of anxiety you have about your lack of control over the situation and your fear of losing money. And if you hear from friends or relatives about how much they got whacked by holding on to their shares, you might even give yourself a pat on the back.Â

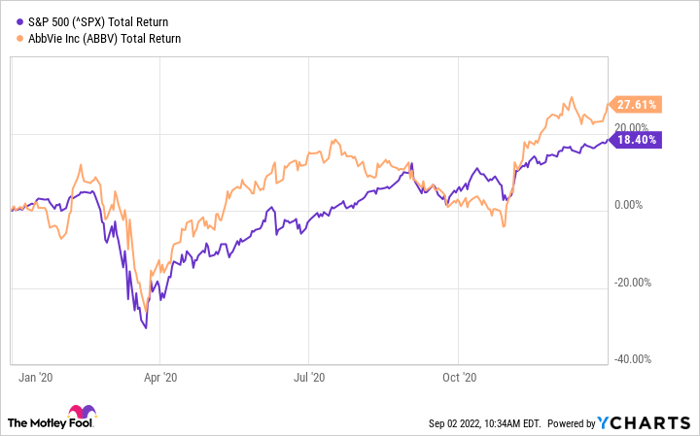

But you’ll probably end up missing out on the rebound afterward. And in many cases, that means you’ll make less money than if you’d simply stayed the course. Let’s examine AbbVie‘s (NYSE: ABBV)performance during the coronavirus crash in March 2020 as an example.

As you can see, AbbVie’s shares took a beating during the crash, as did the market. But as the catalyst for the crash, the pandemic, didn’t actually do much to affect the company’s ability to do its business of developing and commercializing drugs, its stock quickly bounced back.

Within a couple of months, it was outperforming the market, and its earlier damage was entirely reversed. The stock even ended the year significantly above where it started, and you’d have missed out on that gain if you had sold your shares. Even if you tried to restart your position, you’d struggle to time it correctly and you’d almost certainly be missing out on some upside.

There’s absolutely no guarantee that every stock will behave the same as AbbVie’s did during every market crash, and many will not. In cases where the crash isn’t caused by anything that fundamentally impacts a company’s ability to make money as efficiently as it currently does, however, selling is likely to be a poor decision.

2. Dramatically change your investing strategy without good reason

In keeping with the above, the second thing that you shouldn’t do if the stock market crashes is to switch up your game plan for investing without noodling on it for a good while. It’s a fact of life that crashes are often precipitated by economic or global events. Nonetheless, if you have a properly diversified portfolio, it should be unlikely that any specific trend or happening makes all of your stocks genuinely vulnerable to further declines all at once. And that means any changes to your approach should be at the margin, even after a crash.

For example, let’s say before the pandemic you held AMC Entertainment (NYSE: AMC) for exposure to the entertainment industry in the same portfolio as your AbbVie shares. The market’s collapse in March was caused by fears of the coronavirus, and AMC’s share price was hit plenty hard. As an intelligent and far-sighted investor, you held on to your shares at the time. But during your quarterly assessment of your positions, you decide that movie theaters are probably not going to be making a strong comeback for as long as the coronavirus is afoot, and you opt to sell your shares.

So far, so good — it’s important to make adjustments to your strategy when new information makes your original investing thesis incorrect or irrelevant.

Where many investors might go wrong, however, is to then do something like take their proceeds from the sale of AMC and invest them in a way that reduces their portfolio’s level of diversification, perhaps by buying more shares of AbbVie. Such an action is a major departure from your prior approach of buying an entertainment industry stock to give yourself exposure to that industry’s future growth. And by doing so, you’re throwing the baby — your well-reasoned desire for diversification — out with the bathwater, which in this case is AMC’s poorly performing stock in the wake of the crash.Â

3. Stay on the sidelines

The final thing investors shouldn’t do if the market crashes is to stay on the sidelines and wait for calmer waters. Instead, they should take action to buy while shares are cheaper than normal. And that’s especially true if you plan to dollar-cost average to build up your positions. For those who have some capital saved up, sharp and panic-driven downturns are opportunities to shore up your holdings with deeply discounted shares — once again, assuming that your original investing thesis about why they’re worth buying is still valid.Â

If you do decide to sit on the sidelines during a crash or correction, you won’t be actively harming your portfolio’s value, but you’ll likely be missing out on growth. It’s frightening to buy more shares of a stock when it’s down and when it seems like the sky is falling, but famous investors like Warren Buffett do it. And for companies that pay a dividend, like AbbVie, buying rather than idling means that you’ll be securing shares with higher dividend yields than you could normally get, so you’ll get paid for your smart decision to take a hot bargain for years down the line.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Alex Carchidi has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

from The Motley Fool Australia https://ift.tt/t2exvro

Itâs easy to be bearish on the stock market right now.

1) Interest rates are rising, with the Reserve Bank of Australia (RBA) widely expected to hike again today, likely by another 50 basis points, lifting the cash rate to 2.35%.

2) Inflation is running at a 32-year high, at an annual rate of 6.1%. In the United States, the annual inflation rate is 8.5%, and in the United Kingdom, itâs over 10%, with some experts saying it could reach 15% there by the start of 2023.

The picture is much worse on Wall Street, with the S&P 500 and NASDAQ indices down 18% and 27% respectively so far this year, and effectively in bear market territory, the first prolonged such event since the global financial crisis.

3) The S&P/ASX 200 Index (ASX: XJO) is down 8% since the start of the year, having been off as much as almost 14% in June.

4) According to Bloomberg, Australian consumer sentiment has declined every month since November for a cumulative drop of almost 23%, bringing it to levels reached during the COVID pandemic and 2008-09 global financial crisis.

Not much to look forward to, hey?

Admittedly, things feel bleak, although for me, thatâs probably more to do with my profession â a stock market investor and commentator â than reality. In our business, fear sells like nothing else, including article headlines, like the one you clicked on to read this.

Reality is, I donât know where the share market goes from here.

It could go higher if there are signs of inflation being tamed. Or it could grind lower if it becomes apparent interest rates will have to rise higher than current expectations.

Speaking of which, according to the Australian Financial Review (AFR), Commonwealth Bank forecasts the RBA will pause tightening for âat least a few monthsâ when the cash rate hits 2.6% or 2.85%. In contrast, the bond market implies a terminal cash rate of 3.8% by mid-next year.

Recession and prolonged bear market

Itâs an incredibly wide discrepancy and the likely difference between a softer landing and a recovering share market and a recession and a prolonged bear market.

Of the two scenarios, with my glass half-full, cap on, my money would be on the RBA cash rate not hitting 3.8% by the middle of next year.

At that level, mortgage holders and the housing market would be smashed. The Commonwealth Bankâs standard variable mortgage rate already stands at an eye-watering 6.3% â something that would likely plunge the Australian economy into recession and send the ASX 200 into a vicious bear market.

The most successful investors donât let economic forecasts â good or bad â impact their investing decisions. Itâs because they are generally unreliable.

Sure, itâs easy to say now interest rates will go higher. But it was only in October last year that the RBA was saying interest rates would not rise until 2024, and that was when the cash rate was just 0.1%.

Sure, itâs easy to say now the share market will go lower, given the somewhat dire economic outlook. But how does that account for the 6% gain in the ASX 200 index since mid-June this year, and the almost doubling of the Life360Inc (ASX:360) share price and the almost 60% gain in the WiseTech Global Ltd (ASX: WTC) share price in the same period?

As I said at the top, itâs easy to be bearish on the stock market right now.

If you are tempted to cash out now, Iâd question why you are even invested in the stock market. Volatility comes with the turf, and is the very reason why the stock market offers above-average returns.

But such returns â between 8% and 12% per annum, on average â only accrue to patient, long-term investors. Managing your emotions is often your biggest investing challenge.

In the meantime, my best advice for right now, as it is at any time in the cycle, is to methodically and consistently just keep adding money to the market. Your future wealth will thank you.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Bruce Jackson has positions in WiseTech Global. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Life360, Inc. and WiseTech Global. The Motley Fool Australia has positions in and has recommended WiseTech Global. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/FVLJfvZ

But above all else, it appeared as though ASX BNPL shares were back in vogue.

The Sezzleshare price skyrocketed 215% in July while the Splitit Ltd (ASX: SPT) share price doubled.

But the music stopped in August as ASX BNPL shares failed to keep the party going. The Zip share price tumbled 15% across the month, Sezzle shares slid 18%, and Splitit shares were dumped 21%.

It appears that investor sentiment waned throughout the month and Zipâs FY22 results only compounded the fall.

But even still, the Zip share price has doubled since the end of June.

Pick a series of time periods and youâll likely get starkly different performances, such is the wildly-swinging nature of the Zip share price.

Why has the Zip share price been sliding?

Iâd say a key factor here is investor sentiment, which continues to turn on a dime.

But the market didnât appear too impressed with the results Zip delivered at the end of the month.

Letâs take a look at some of the key points.

Customer count

Zip introduced a new metric in its FY22 results, disclosing active customers for the first time.

In order to be considered active, a customer must have had transaction activity in the last 12 months.

Prior to this, Zip had simply been disclosing total customer numbers, which were being inflated by inactive customers.

Hereâs how these figures measure up across Zipâs geographical segments.

Active customers

Total customers

Australia and New Zealand (ANZ)

2.3 million

3.2 million

United States (US)

4.1 million

6.4 million

Rest of world (ROW)

1.1 million

1.8 million

Group

7.5 million

11.4 million

Separate to this, Zip also restated its total customer count in the US, removing 600,000 accounts from the figure disclosed in 4Q22 as they were ânot yet activated as at 30 June 2022â.

Unit economics mixed

As I discussed when previewing Zipâs FY22 results, unit economics tell an important tale of the companyâs underlying performance.

The key metrics here are revenue margin, cash cost of sales (which includes bad debts), and cash transaction margin.

These metrics encapsulate how well Zip can convert the transaction value that flows through its platform into revenue. And from there, how much of this revenue it can successfully collect from customers.

Zip managed to buck a trend of declining revenue margins, improving from 6.8% in FY21 and 6.7% in HY22 to 7.1% in FY22.

But rising bad debts led to an increase in cash cost of sales, jumping from 3.7% of TTV in FY21 to 4.8% in FY22.

As a result, the companyâs cash transaction margin took a hit, dropping from 3.1% to 2.3%.

Zip has a medium-term target range of between 2.5% and 3%, so investors will be expecting this margin to improve as the platform scales and bad customers are weeded out.

Net loss blows out

When you take a cursory glance at Zipâs income statement, one thing, in particular, stands out: the big negative number on the bottom line.

Zip served up a net loss of $1.1 billion in FY22. A frightful number, especially in the context of the companyâs market capitalisation of $592 million.

But upon closer look, this $1.1 billion loss included an $821 million impairment charge relating to goodwill and intangibles. More specifically, the carrying value of some of Zipâs overseas businesses has been written down on the back of slower forecasted growth rates and rising interest rates.

So instead of looking at the bottom line, Zip believes a better reflection of the underlying business is cash earnings before tax, depreciation, and amortisation (EBTDA). Here, the company posted a cash EBTDA loss of $207 million in FY22, a notable increase from the $23 million loss in the prior year.

This came as the companyâs cost base grew at a faster clip than revenue. Bad debts and expected credit losses more than doubled to $276 million, employee expenses surged 89% to $184 million, and marketing expenses jumped 63% to $120 million.

But green shoots may be emerging after the ANZ business generated positive cash EBTDA of $28 million, up from $8 million in the prior year. Importantly, cash operating expenses grew by just $2 million to support a $22 million rise in gross profit.

What next for the Zip share price?

The Zip share price has cratered 81% this year. And there could be further downward pressure ahead as Zip shares will soon be ousted from the S&P/ASX 200 Index (ASX: XJO) in the upcoming September rebalance.

In an effort to accelerate its pathway to profitability, Zip has committed to reining in costs and focusing on the core business. Internally, this has been dubbed âOperation Blue Skyâ.

Zip is targeting cash EBTDA profitability in the first half of FY24.

The market will be closely watching how well Zip is able to execute these cost-cutting initiatives. And how this may impact the companyâs growth rates and competitive position going forward.

In the wake of Zip’s FY22 results, analysts at Macquarie maintained their underperform rating on Zip shares. Analysts at UBS also maintained their sell rating, with the 12-month price target unchanged at 45 cents.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Cathryn Goh has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended ZIPCOLTD FPO. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/YFoHA9B

Investors who own Magellan Financial Group Ltd (ASX: MFG) shares can rejoice. Today is the day that the Magellan dividend will flow into bank accounts.

Reporting season has only just finished, but some businesses are already getting on with paying shareholders the money theyâve allocated for them.

Magellan is paying its dividend only three weeks after announcing it. Thatâs a quick turnaround.

How big is the Magellan dividend for shareholders?

Magellan announced that the total dividend for the second half of FY22 is 68.9 cents per share, franked to 80%.

That final dividend comprises an ordinary dividend of 65 cents and a performance fee of 3.9 cents per share.

The franking level of 80% was an increase from the FY22 first half, which was 75%, and itâs expected to increase in future years.

This dividend is in line with the companyâs dividend policy, subject to corporate, legal, and regulatory considerations.

Magellanâs ordinary interim and final dividends are based on 90% to 95% of the net profit after tax (NPAT) of the fund’s management business, excluding crystallised performance fees.

The annual performance fee dividend is based on 90% to 95% of net crystallised performance fees after tax.

Added to the interim dividend of 110.1 cents per share, this brought the full-year dividend to 179 cents per share. That meant Magellan reduced its total dividend by 15% from FY21.

What happened to the profit?

With Magellanâs dividend tracking its profit, itâs worth noting that the business experienced a drop in funds under management (FUM), revenue, and profitability.

The average FUM fell 9% over the year to $94.3 billion. However, at 29 July, its FUM had dropped to $60.2 billion.

The fund’s management profit before tax and performance fees was down 11% to $470.6 million. The adjusted net profit before tax was down 12% to $515.2 million. The adjusted profit after tax was only down 3%. This is due to a $6.6 million profit being generated by associates (compared to a loss of $41.8 million in FY21).

Outlook for the Magellan share price and dividend

Unless Magellan can regain FUM quickly, itâs hard to see that the dividend will get back to its former heights any time soon.

The new CEO and managing director, David George, noted that client confidence has been impacted by changes in the leadership team and personnel, and underperformance of the global shares strategy.

Magellanâs focus now is on the core funds management strategy, strengthening processes, and driving consistent and improved investment performance.

George will be giving shareholders an update on his thoughts and strategies in October 2022.

Magellan share price snapshot

Starting mid-July, Magellan shares rose 33% to 11 August. But they have since dropped 18.8%. Over the last six months, Magellan shares are down 2.5%.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/glKkLBN

With a market capitalisation of $54 billion, Fortescue Metals Group Limited (ASX: FMG) is one of the biggest businesses on the ASX. But are investors able to buy Fortescue Future Industries (FFI) shares?

Fortescue is best known for being a large ASX mining share with a focus on iron ore, along with its heavyweight peers Rio Tinto Limited (ASX: RIO) and BHP Group Ltd (ASX: BHP).

But there is elevated interest in Fortescue’s business segment known as Fortescue Future Industries.

FFI describes itself as a âglobal green energy company committed to producing green hydrogen, containing zero carbon, from 100% renewable sources”. Green hydrogen, when used, primarily produces water.

FFI is focused on âleading the green industrial revolution, developing technology solutions for hard-to-decarbonise industries, while building a global portfolio of renewable energy, green hydrogen and green ammonia projects”.

One of its key goals is to help decarbonise Fortescueâs operations by 2030.

Can we buy shares of Fortescue Future Industries?

FFI is not a separately listed business on the Australian Stock Exchange. So investors canât directly buy shares of FFI.

But investors can buy shares of the ASX-listed Fortescue which owns all of Fortescue Future Industries.

Some experts believe that FFI is already worth tens of billions of dollars. According to reporting by the Australian Financial Review, Fortescue chair Andrew Forrest has been approached by investment banks. They’ve suggested Fortescue Future Industries is already worth US$20 billion if it was to go through the process of an initial public offering (IPO).

So, if investors were to apply that to Fortescue’s overall market capitalisation, it would represent a significant chunk of the company’s value. It also depends on how much investors would value Fortescueâs iron business.

What are FFIâs long-term goals?

Certainly, Forrest has big goals for Fortescue Future Industries. He said the following in Fortescueâs FY22 result:

We must become the Saudi Arabia, not of oil, but of green hydrogen, we can become the Asia of green iron too, if we are prepared to commit to it. Think the North West Shelf â not of climate-threatening methane, but of carbon-free green ammonia, for every ship in the world. Please donât think it canât be done, it can.

The company is investing to create a global portfolio of green energy projects to supply 15 million tonnes per year of renewable green hydrogen by 2030.

FFI has already signed deals with companies in the northern hemisphere for supplying green hydrogen.

In October 2021, it signed a memorandum of understanding (MoU) with UK-based construction company JCB and Ryze Hydrogen for the purchase of 10% of FFIâs global green hydrogen production.

It has also signed an MoU with German electricity company E.ON to deliver up to five million tonnes per annum of green hydrogen by 2030. This one deal represents approximately a third of Fortescue Future Industriesâ future production to 2030.

Fortescue has also made a few acquisitions and partnerships to boost the decarbonisation and earnings prospects of FFI. For example, it acquired Williams Advanced Engineering, a leading provider of high-performance battery and electrification technology.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Tristan Harrison has positions in Fortescue Metals Group Limited. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/lmMh0gw