There is no doubt Nvidia Corp (NASDAQ: NVDA) is one of the hottest stocks on the planet right now.

The computer chip maker is raking in sales from the artificial intelligence (AI) boom, beating expectations every quarter for the past year or so.

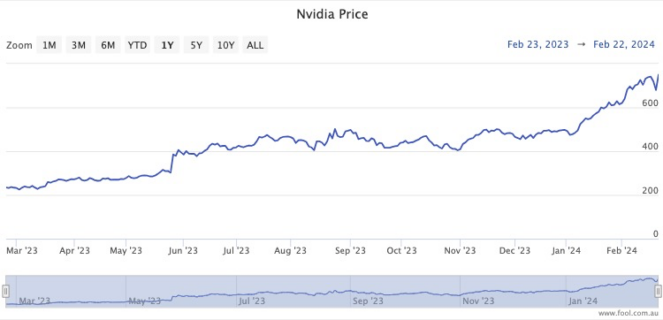

The stock has now rocketed 232% for the past year, incredibly rising 16.4% on a single day on Thursday US time.

Whether it can keep up this cracking pace is up for debate. Some sceptics are even suggesting the AI hype might already be a bubble.

So is there an ASX stock on fire like Nvidia?

Yes, there is.

And it’s going about its business with far less publicity.

What does Audinate do?

Audinate Group Ltd (ASX: AD8) is best described as an audio networking technology provider.

The company was born out of a team working at the government research organisation National Information and Communications Technology of Australia (NICTA) in the 2000s.

Co-Founder and chief executive Aidan Williams remembers the genesis when he was playing music twenty years ago.

“I was constantly connecting my synth to a mixer, to a sound card, MIDI cables, all sorts of different connections,” he said.

“To me, it seemed like a networking problem. Why make all those different connections when you could integrate it into a single network?”

The solution to this ended up as Audinate’s flagship product Dante.

Dante is a networking protocol that is now embedded into many audio products. The “language” allows equipment like instruments and mixers to talk to another, to produce lossless audio.

The Aussie company that could be an ‘unregulated monopoly’

The innovation is now dominant enough in the entertainment industry that Medallion Financial Group managing director Michael Wayne said back in 2021 Audinate “has the potential to be an unregulated monopoly”.

“You can liken it to Bluetooth, if you like. Except Bluetooth isn’t as good a technology and it’s owned by a cooperative.”

While not widely discussed in the financial media, investors in the know have already made plenty of money from Audinate shares.

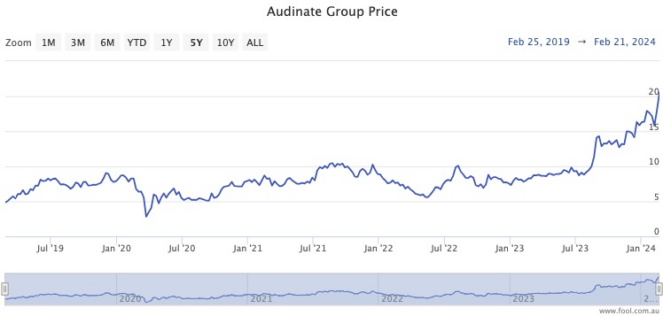

Similar to Nvidia, the stock has soared over the past 12 months, now going for 155% higher.

Over the past five years Audinate shares have returned a phenomenal 307%, for a 32.4% compound annual growth rate (CAGR).

And many experts believe the Aussie success story still has plenty of legs.

Broking platform CMC Invest currently shows none of the seven analysts covering the stock rating it as a sell. Three say buy while four are recommending a hold.

The post 1 ASX stock I think is just as hot as Nvidia (without all the hype) appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 10 November 2023

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- Here’s how the ASX 200 market sectors stacked up this week

- The Brainchip share price is up 213% this month. Is Nvidia to blame?

- Is the Nvidia share price on course to reach US$1,400?

- Why are ASX tech shares booming on Friday?

- Nvidia stock pops 10% after-hours following ‘insane result’

Motley Fool contributor Tony Yoo has positions in Audinate Group. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Audinate Group and Nvidia. The Motley Fool Australia has positions in and has recommended Audinate Group. The Motley Fool Australia has recommended Nvidia. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Kg5IalC