Motley Fool Australia Chief Investment Officer Scott Phillips joined Tracy Vo for Nine’s Late News on Thursday night to unpack the latest business news, including a lower profit for Qantas Airways Limited (ASX: QAN), calls for the Treasurer to retain his power of veto over the Reserve Bank of Australia (RBA), and a billion dollar payday for Andrew ‘Twiggy’ Forrest.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Scott Phillips has positions in Fortescue. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/pzVkm9r

Group net profit after tax before amortisation (NPATA) down 36% to $15 million

Net loss after tax of $4.6 million (from $4 million profit)

What happened during the half?

For the six months ended 31 December, Pexa reported a 16% increase in revenue to $163.3 million.

This reflects an 11% lift in Pexa exchange revenue to $149.6 million, an 80% jump in Digital Growth business revenue to $7.2 million, and a 261% increase in International business revenue to $6.5 million.

Operating EBITDA was up 12% to $58.8 million for the half. This was driven by a 17% jump in Pexa exchange EBITDA to $82.9 million, which was partially offset by operating losses from its other businesses.

Pexa’s NPATA came in at $15 million for the half, down from $23.5 million a year earlier. Management advised that this reduction was primarily due to costs associated with the acquisition of Smoove, restructuring costs, and higher amortisation arising from investments.

Management commentary

Pexa’s CEO, Glenn King, was pleased with the half. He said:

Across the Group, these results represent the discipline we have brought to executing our strategy. This includes improving the efficiency of our business through our Productivity Enhancement Program and beginning to embed our capital management framework. We have made strong progress to ensure we are well placed to execute on our strategic objectives in the second half, but we still have more to do to realise our ambitions in Australia and overseas.

Pleasingly, PEXA Exchange continues to perform strongly and has maintained its leading market position, reflecting the resiliency of the platform. It delivered a good first-half result, benefiting from CPI-linked price increases, increased market volumes and penetration and a shift in activity towards higher-value transfers.

How does this compare to expectations?

Goldman Sachs described the result as “strong” and notes that its margins are tracking ahead of its FY 2024 guidance. The broker adds:

PXA reported 1H24 Sales/EBITDA/Adj. NPATA +16%/+12%/-8% vs. pcp to A$163mn/A$59mn/A$26mn, which were +2%/+8%/+15% vs. GSe and +5% vs. Visible Alpha Consensus Data EBITDA (A$56mn). FY24 guidance reiterated including group operating EBITDA margins (ex. Smoove) >35%. Net debt/EBITDA increased to 2.5x (1H23 2.3x) with PXA flagging no current expectation of material acquisitions to come.

Outlook

Pexa has reaffirmed its previous guidance for FY 2024. It expects:

Group operating EBITDA margin of 35% or better

Exchange operating EBITDA margin of 50-55%

Net cash outflows of $70 million to $80 million for the International and Digital Growth businesses

Breakeven operating EBITDA for Digital Growth for the month of June 2024.

The Pexa share price is down approximately 2% over the last 12 months.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group and PEXA Group. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/WmcSIiw

Of all the index funds on the ASX, those that track the Nasdaq 100 Index have delivered some of the greatest returns in recent years.

Propelled by their huge stakes in the stellar ‘magnificent seven’ tech stocks, exchange-traded funds (ETFs) like the BetaShares Nasdaq 100 ETF (ASX: NDQ) have delivered some breathtaking returns for investors, that make our own ASX seem very tame by comparison.

Just take NDQ units.

Over the 12 months to 31 January 2024, this ETF has returned an astonishing 51.31% (including dividend distributions). The fund has also averaged a Warren Buffett-esque 22.63% per annum over the past five years.

Until recently, the BetaShares Nasdaq 100 ETF was the only Nasdaq-specific fund on the ASX. But last year, it was complimented with the addition of the Global X US 100 ETF (ASX: N100).

Given the kinds of numbers above, it’s not too surprising to see that the ASX has just welcomed not one, but two more ETFs that give investors additional Nasdaq exposure.

Betashares just yesterday launched the BetaShares Nasdaq Next Gen 100 ETF (ASX: JNDQ), as well as the BetaShares Nasdaq 100 Equal Weight ETF (ASX: QNDQ).

Both of these ETFs give investors exposure to Nasdaq stocks. But both offer different paths to doing so. We’ll start with the Nasdaq 100 Equal Weight ETF, as it’s a little simpler to explain.

Two new Nasdaq ETFs hit the ASX

So like most index funds, the BetaShares Nasdaq 100 ETF (NDQ) holds the 100 shares in its portfolio in weighted proportions. This means that the largest shares (by market capitalisation) take up far more room in the fund’s portfolio than the smaller ones.

To illustrate, right now Microsoft â the largest public company in the world at present â commands an NDQ weighting of around 8.8%. In contrast, one of the smaller holdings in this ETF is the pharmacy chain Walgreens Boots Alliance. It holds just a 0.1% weighting in the same portfolio.

However, the QNDQ ETF seeks to change this paradigm. As its name implies, this fund gives every stock in the Nasdaq 100 an equal weight, meaning that Microsoft has the same level of weighting and influence on this fund as Walgreens. That would be around 1%.

The Nasdaq Next Gen 100 ETF is a little different though. Instead of holding the largest 100 shares on the Nasdaq (as NDQ and QNDQ both do), it tracks the largest 100 shares outside the Nasdaq 100 (the Nasdaq 101-201 if you will).

So rather than having access to names like Microsoft, Apple, Amazon and Tesla, you’re getting smaller companies like eBay, DraftKings, Zoom Video and Baidu.

On day two of these funds’ ASX lives, both are doing well and are above the price the units listed at yesterday. But it will be interesting to see how both of these new Nasdaq ETFs go over longer periods of time, especially compared to the uber-popular BetaShares Nasdaq 100 ETF.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Foolâs board of directors. Motley Fool contributor Sebastian Bowen has positions in Amazon, Apple, Microsoft, and Tesla. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Amazon, Apple, Baidu, BetaShares Nasdaq 100 ETF, Microsoft, Tesla, and Zoom Video Communications. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended eBay and has recommended the following options: long January 2026 $395 calls on Microsoft, short April 2024 $45 calls on eBay, and short January 2026 $405 calls on Microsoft. The Motley Fool Australia has positions in and has recommended BetaShares Nasdaq 100 ETF. The Motley Fool Australia has recommended Amazon, Apple, and Zoom Video Communications. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/T5kPjcb

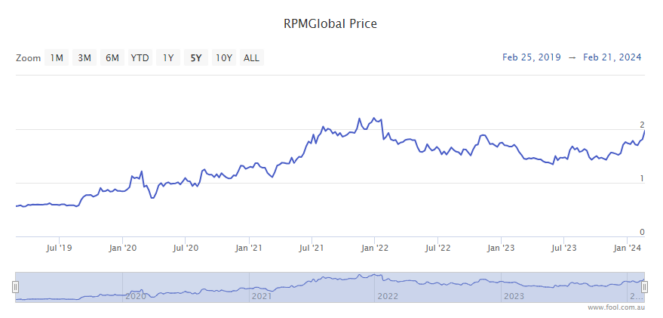

The RPMGlobal Holdings Ltd (ASX: RUL) share price is up 8.91% at $2.14 amid a broader tech stock rally on Friday.

RPMGlobal provides technology solutions, advisory consulting, and training to the mining industry.

The company is outperforming its ASX All Ords peers, with the S&P/ASX All Ordinaries Index (ASX: XAO) up just 0.49% by comparison.

But technology is the hottest market sector of the day, with the S&P/ASX 200 Information Technology Index (ASX: XTX) currently up 1.49%.

This follows a 2.94% surge for the NASDAQ overnight.

Popular US tech stocks made impressive gains, led by NvidiaCorp, which shot up 16.4% to a new record high of US$785.75 after the semiconductor company released its 4Q FY23 numbers.

Meta Platforms gained 3.87%, Amazon rose 3.55%, and Apple lifted 1.12%.

Net assets of $58.2 million, up $0.8 million as of 31 December 2023

Cash of $23.3 million and no debt.

What else happened in 1H FY24?

RPMGlobal said net revenue from the software division increased 24.9% to $37.1 million, with software subscription revenue up 26% to $21.3 million. The company said some of this growth was due to customers converting their software licenses from perpetual to subscription.

Software consulting revenue rose 22.6% to $6.5 million. Maintenance and support revenue fell 9.7% to $6.5 million. Perpetual licence sales were steady at $1.1 million.

The company noted that it has outlaid $10 million in an on-market share buyback over the past year.

What did RPMGlobal management say?

The company said its software products and advisory services were gaining market share from competitors, evidenced by Southeast Asia sales and the reputation built by the advisory business.

Management commented:

AMT continues to be selected and implemented by the world’s major mining companies, and XECUTE is quickly becoming the ‘go-to” operational product for tier two miner’s and has started to make serious inroads into the tier one global miners.

We believe XECUTE will begin to rival AMT in terms of market acceptance and revenue generation in the next few years.

What’s next for RPMGlobal?

Management said it was optimistic about the years ahead, given RPMGlobal’s strong balance sheet, healthy cash flow, and competitive advisory and software offerings.

RPMGlobal share price snapshot

The RPMGlobal share price has risen 34% over the past year, while the ASX All Ords has lifted 5.4%.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Foolâs board of directors. Motley Fool contributor Bronwyn Allen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Amazon, Apple, Meta Platforms, Nvidia, and RPMGlobal. The Motley Fool Australia has recommended Amazon, Apple, Meta Platforms, Nvidia, and RPMGlobal. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/xMQ8wLb

Flight Centre Travel Group Ltd (ASX: FLT) shares will be on focus next week when the travel agent giant releases its half-year results.

Ahead of the release on Wednesday, let’s see what the market is expecting.

Flight Centre half-year results preview

According to a note out of Goldman Sachs, its analysts are expecting the company to report explosive growth for the first half.

Its analysts have pencilled in sales growth of 28.5% to $1,288.1 million and earnings before interest and tax (EBIT) growth of 344.9% over the prior corresponding period. This is modestly higher than the market consensus estimate.

As for dividends, the broker is expecting a 23 cents per share dividend for the full year.

Flight Centre’s dividends are usually weighted to the second half, so this could mean an interim dividend in the region of 8 cents per share.

Elsewhere, analysts at Morgans recently commented on their expectations for the first half of FY 2024. They said:

Earnings are seasonally skewed to the 2H (even more so post the Scott Dunn acquisition). 2Q NPBT was guided to be below the 1Q of A$54m. In line with seasonal trends, 1H cashflow is usually weak.

Should you buy Flight Centre shares?

At present, Goldman Sachs is sitting on the fence with this one. It has a neutral rating and $20.70 price target on the company’s shares. This implies potential downside of 5% from current levels.

Morgans, on the other hand, is feeling more upbeat. It has an add rating and $26.00 price target on Flight Centre’s shares.

If the broker is on the money with this recommendation, it would mean upside of 19% for investors over the next 12 months.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has recommended Flight Centre Travel Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Isdm3i5

Three S&P/ASX 200 Index (ASX: XJO) shares just earned substantial upgrades from leading brokers.

The bullish broker outlooks for these stocks follow the release of the companies’ earnings results.

The brokers forecast these big-name ASX stocks could see share price gains of as much as 25% over the year ahead. And that’s not including the dividends all three companies pay.

Read on for the three stocks with some big potential gains ahead.

Why these three ASX 200 shares could surge in 2024

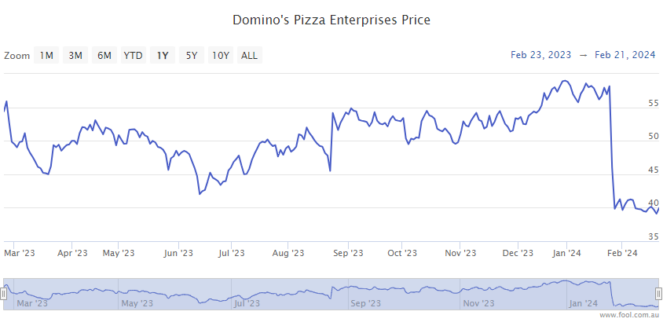

The first ASX 200 share earning a broker upgrade is Domino’s Pizza Enterprises Ltd (ASX: DMP).

The fast-food pizza retailer reported its half-year results on Wednesday. The Domino’s share price closed up 2.7% on the day and gained another 7.7% yesterday. Shares are up 0.4% in early afternoon trade today at $43.85 apiece.

On the positive side of the ledger, network sales increased 8.8% year on year to $2.14 billion. And Domino’s reported same store sales growth of 1.25%. This came alongside an 11.8% boost in online sales, which reached $1.71 billion over the six months.

On the negative side of the ledger for the ASX 200 share, earnings before interest and tax (EBIT) was down 5.3% to $107.9 million. And net profit after tax (NPAT) was down 13% to $62.3 million. Earnings and profits were both impacted by the company’s struggling Asian operations.

Still, 2024 is off to a strong start.

In the first seven weeks of the new half, same stores sales growth increased 8.39% in ANZ and 0.34% in Asia. Growth dipped 0.64% in Europe.

Even after the past three days of share price gains, Jarden Securities sees significant further upside ahead.

The broker raised Domino’s to an ‘overweight’ rating with a $49 price target. That’s almost 12% above current levels. And that’s not including dividends. Domino’s declared an unfranked interim dividend of 55.5 cents per share.

Which brings us to the second ASX 200 share receiving a significant broker upgrade, fashion jewellery retailer Lovisa Holdings Ltd (ASX: LOV).

Lovisa reported its half-year results on Thursday. Investors reacted by sending the stock up 10.4%. And the Lovisa share price is up another 4.8% in afternoon trade on Friday at $28.62.

Investor enthusiasm was stoked by the company’s opening 74 new outlets over the six months. Lovisa had 854 stores at the end of December. In a major development, the company opened its first stores in China and Vietnam.

On the financial front, revenue increased 18.2% year on year to $373 million, with NPAT up 12.0% to $53.5 million.

Citi noted that “Lovisa has delivered another strong result and is successfully evolving into a global retailer”.

The broker raised Lovisa to a ‘buy’ rating with a $31.65 price target. That represents a potential upside of more than 10% from current levels. Lovisa also pays dividends. The company declared an interim dividend 50 cents per share, 30% franked.

Rounding off the list

Rounding off the list of ASX 200 shares receiving hefty broker upgrades is gambling and gaming company Tabcorp Holdings Ltd (ASX: TAH).

Tabcorp reported its half-year results on Thursday.

The company reported a statutory net loss after tax of $636.8 million for the six months. And revenue was down 5% year on year to $1.21 billion.

Concerned over the sliding revenues, investors hit the sell button yesterday, sending the Tabcorp share price down 10.3%. But the buyers are back on Friday, with Tabcorp shares up 4.2% at the time of writing, trading for 68 cents apiece.

It’s unlikely today’s buying is fuelled by the 1 cent per share, fully franked interim dividend.

But the fact that this represents a payout ratio of 111%, which management said reflected “confidence in the business and a strong financial position”, could be stirring optimism.

As could the ASX 200 share’s ongoing investments in AI and new technology platforms, which management said was enabling the company to become a more digital-oriented business.

Macquarie certainly has a bullish outlook for the stock. The broker raised Tabcorp to an ‘outperform’ rating with an 85-cent price target.

That represents a 25% potential upside from current levels.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Domino’s Pizza Enterprises and Lovisa. The Motley Fool Australia has recommended Domino’s Pizza Enterprises and Lovisa. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/FHbJgO6

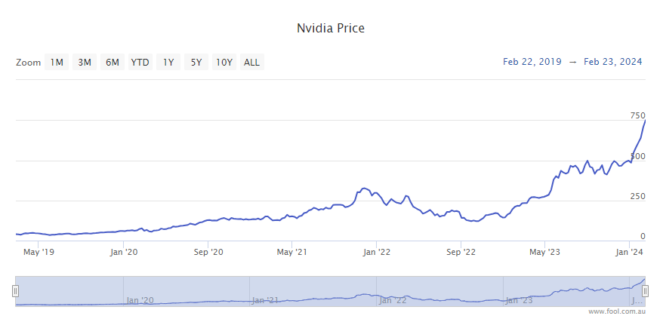

The Nvidia Corp (NASDAQ: NVDA) share price closed last night at US$785.38, up 16.4% after the semiconductor company delivered a cracking quarterly update that included a 769% net income increase.

Say, what? Yep, that isn’t a typo.

Following the results, several brokers have laid out their predictions for the Nvidia share price from here.

And one analyst is tipping the stock will get to US$1,400… within just 12 months.

Nvidia share price on fire

Hans Mosesmann, senior research analyst at Rosenblatt Securities, appears to have the highest 12-month target price on Nvidia at the moment.

He thinks the stock can almost double within the next 12 months to US$1,400 per share.

That’s a pretty remarkable prediction for a company that already has a market cap of US$1.94 trillion.

Then again, the Nvidia share price has more than tripled over the past year. So, in a historical context, you could say Mosesmann’s tip of a near-doubling over the next year sounds like a slowdown!

For the record, this time last year the Nvidia share price was about US$232.

Full-year revenue up 126% to a record of US$60.9 billion

Gross margin up 15.8% to 72.7%

Net income up 581% to US$29.76 billion

Earnings per share up 586% to US$11.93

Nvidia’s founder and CEO, Jensen Huang, commented: “Accelerated computing and generative AI have hit the tipping point. Demand is surging worldwide across companies, industries and nations.”

The company expects 1Q FY24 revenue to go higher still, to $24 billion (+/- 2%), with an improved gross margin in the range of 76.3% to 77%.

And all of this good news has market analysts in a bit of a lather.

Most brokers raise 12-month share price targets

Most brokers raised their 12-month price targets on Nvidia overnight and maintained their buy ratings.

Here is a selection of the most bullish predictions:

Rosenblatt Securities raised its price target to US$1,400, up from US$1,100 (maintain buy)

Keybanc raised its Nvidia share price target to US$1,100, up from US$740 (maintain overweight)

Benchmark raised its price target to US$1,000, up from US$625 (maintain buy)

Bernstein raised its price target to US$1,000, up from US$700 (maintain outperform)

Bank of America raised its price target to US$925, up from US$800 (maintain buy)

Truist raised its price target to US$911, up from US$691 (maintain buy)

TD Cowen its Nvidia share price target to US$900, up from US$700 (maintain outperform)

Wolfe raised its price target to US$900, up from US$630 (maintain outperform)

A couple of brokers were a little more conservative on Nvidia’s share price trajectory from here:

UBS lowered its price target to $800, down from $850 (maintain buy)

Deutsche Bank raised its price target to $720, up from $560 (maintain hold rating)

Morgan Stanley raised its price target to $795, up from $750 (maintain overweight)

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Bank of America is an advertising partner of The Ascent, a Motley Fool company. Motley Fool contributor Bronwyn Allen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Apple, Bank of America, Microsoft, Nvidia, and Truist Financial. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool Australia has recommended Apple and Nvidia. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/wxb8k7W

According to a note out of Bell Potter, its analysts have retained their buy rating on this corporate travel specialist’s shares with a reduced price target of $18.30. While the company’s half-year result fell short of expectations, the broker believes that macro issues are to blame rather than anything company specific. And although this has led to earnings estimate revisions, Bell Potter sees plenty of value in its shares at current levels and retains its buy rating. The Corporate Travel Management share price is trading at $16.29 today.

A note out of Morgans reveals that its analysts have retained their add rating on this lithium miner’s shares with a lowered price target of $4.50. Although Pilbara Minerals’ half-year profits missed expectations, the broker remains positive on the investment opportunity here. Especially given how it believes the company is well-positioned to benefit greatly when lithium prices rebound. The Pilbara Minerals share price is fetching $3.66 this afternoon.

Analysts at Goldman Sachs have retained their buy rating on this airline operator’s shares with a trimmed price target of $8.05. The broker believes that Qantas’ half-year results provides a further proof point on its reset earnings capacity. It highlights that the company’s earnings per share is 52% higher than pre-COVID times. But despite this, its market capitalisation is 17% below pre-COVID levels. The Qantas shares price is trading at $5.26 on Friday.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Corporate Travel Management and Goldman Sachs Group. The Motley Fool Australia has recommended Corporate Travel Management. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/o54Lsjz

Statutory NPAT grew from $5.2 million to $6.2 million

Interim dividend per share up 50% to 3 cents per share

The company saw its funded customer number increase 13% to more than 130,000, while superannuation members increased by 16%.

Net inflows amounted to $259 million, an increase of 39% compared to the prior period. This was supported by superannuation net inflows of $269 million.

The company said its continued positive net inflows during challenging market conditions demonstrates the “resilience” of its business.

The investment performance added $0.2 billion to its FUM over the period.

What else happened in the FY24 first half?

Australian Ethical launched three investment products. The Infrastructure Debt Fund was launched, as well as two multi-asset products, being ‘moderate’ and ‘conservative’ funds.

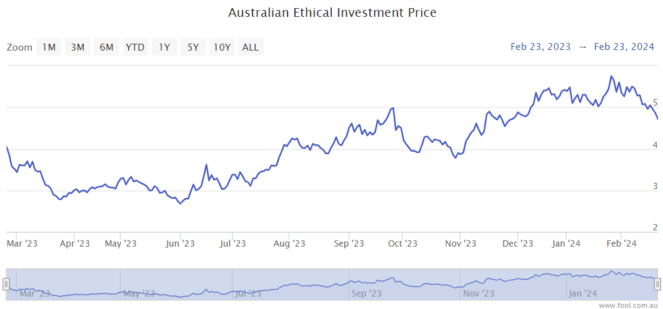

The fund manager pointed out that the business operating leverage is improving. The underlying cost-to-income ratio for the period was 75%, an improvement from the FY23 first half of 81%. Increasing profitability can help give investors more confidence about paying more for the Australian Ethical share price.

What did Australian Ethical management say?

The Australian Ethical CEO John McMurdo said:

Our growth strategy is gathering momentum and we are seeing an uplift in our key financial metrics as well as strong momentum on key strategic initiatives. We are proud of the way we operate our purpose-driven business and were delighted that many aspects of our business – customer experience, growth, governance, investment philosophy as well as investment excellence – were all recognised by awards and accolades during the period.

What’s next for Australian Ethical?

The business is targeting $100 million of annualised revenue by the end of FY24. It generated $47.5 million in revenue in the first half of FY24.

It said its larger scale will allow the business to invest for growth while also delivering profit for shareholders. It’s planning to invest in technology and data analytics, as well as the customer experience.

The company revealed it’s considering a pipeline of ‘inorganic’ opportunities.

Australian Ethical share price snapshot

In the last six months, Australian Ethical shares have risen by 27%, compared to a 7% rise for the S&P/ASX 200 Index (ASX: XJO).

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Australian Ethical Investment. The Motley Fool Australia has recommended Australian Ethical Investment. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/HUnoBet

In afternoon trade, the S&P/ASX 200 Index (ASX: XJO) has followed the lead of Wall Street and is pushing higher. At the time of writing, the benchmark index is up 0.6% to 7,657.2 points.

Four ASX shares that have failed to follow the market higher today are listed below. Here’s why they are dropping:

The Accent share price is down 7% to $2.05. This follows the release of the footwear retailer’s half-year results this morning. Accent reported a 1.7% decline in sales to $810.9 million and a 27.6% reduction in net profit after tax to $42.2 million. This led to the company’s board cutting its interim dividend by 29% to 8.5 cents per share.

The Austal share price is down 14% to $1.92. Investors have been selling the shipbuilder’s shares after it released its half-year results. Austal reported a 7.5% decline in revenue to $717.7 million. And while the company posted a net profit after tax of $12 million (compared to a loss of $7.3 million in FY 2023), this is well short of FY 2022’s half-year profit of $45.1 million.

The Newmont share price is down 7% to $47.26. This morning, this gold miner released its FY 2023 results and reported a huge loss. Newmont posted a 7% decline in adjusted EBITDA to US$4,217 million and a net loss of US$2.5 billion. The latter includes US$1.9 billion in impairment charges, US$1.5 billion in reclamation charges, and US$464 million in Newcrest transaction and integration costs.

The Sandfire share price is down 6% to $7.16. This follows the release of the copper miner’s half-year results this morning. Sandfire reported a 3% decline in revenue to US$417.9 million and a loss after tax of US$53.1 million. Management blamed the loss on the MATSA mining complex in Spain, which was acquired for US$1.9 billion in FY 2022. MATSA accounted for depreciation and amortisation of US$149.1 million.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Austal. The Motley Fool Australia has recommended Accent Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/ERj41WS