The S&P/ASX 200 Index (ASX: XJO) is fighting hard to stay in positive territory on Thursday. In afternoon trade, the benchmark index is up slightly to 7,609.5 points.

Four ASX shares that are acting as a drag on proceedings today are listed below. Here’s why they are falling:

Clinuvel Pharmaceuticals Limited (ASX: CUV)

The Clinuvel share price is down 8% to $15.01. This morning, this biopharmaceutical company released its half-year results and reported a 10% increase in revenue but a 4% decline in net profit after tax. This profit decline reflects a “controlled 28% expenses increase.”

Medibank Private Ltd (ASX: MPL)

The Medibank share price is down 4.5% to $3.69. Investors have been selling the private health insurer’s shares following the release of its half-year results. Medibank reported a 3.3% lift in revenue to $4,024 million and a 16.3% increase in underlying net profit after tax to $262.5 million. The latter was slightly below the consensus estimate of $265.7 million.

Sayona Mining Ltd (ASX: SYA)

The Sayona Mining share price is down 26% to 4.7 cents. This has been driven by news that its largest shareholder, Piedmont Lithium Inc (ASX: PLL), has offloaded its entire stake in the lithium miner. Piedmont Lithium agreed to sell 1,152.2 million Sayona Mining shares for a deep discount of 5.2 Australian cents per share, bringing in proceeds of $59.9 million.

Tabcorp Holdings Ltd (ASX: TAH)

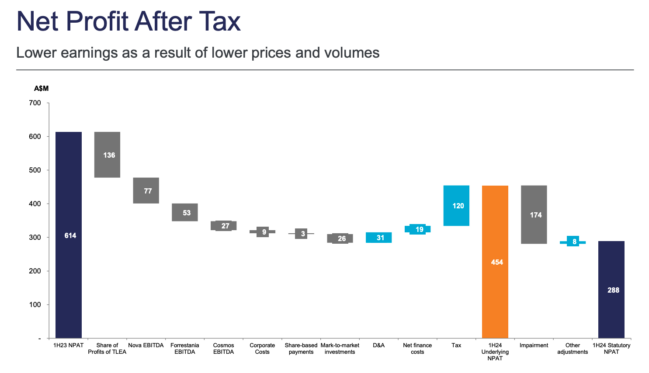

The Tabcorp share price is down 15% to 61.5 cents. This gambling company’s shares are crashing today after investors responded negatively to its half-year results. Tabcorp reported a 5% decline in revenue to $1,210 million and a loss after tax of $636.8 million. The latter was driven by a non-cash impairment charge of $731.9 million after tax to its wagering and media business.

The post Why Clinuvel, Medibank, Sayona Mining, and Tabcorp shares are sinking today appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 10 November 2023

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- Tabcorp share price tumbles 13% on half-yearly earnings loss

- Medibank share price slumps 5% despite surging earnings

- Sayona Mining share price crashes 19% after Piedmont Lithium says sayonara

- Here are the top 10 ASX 200 shares today

- Medibank share price hits 52-week high on US tech partnership

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/DxiGZwF