Owners of this ASX mining share, rejoice! The company has uncovered a major high-grade silver discovery. The Lode Resources Ltd(ASX: LDR) share price more than doubled shortly after opening this morning on the back of the news.

At the time of writing, the Lode Resources share price is swapping hands for 27 cents, 80% higher than its previous close.

However, at its intraday high, stock in the ASX mining share â worth approximately $12 million at Mondayâs close â was swapping hands for 34 cents apiece, representing a 124% gain.

Letâs take a closer look at the find thatâs sent the ASX small cap rocketing higher on Tuesday.

ASX mining share more than doubles on major find

ASX mining share Lode Resources is leaping upwards today following a major discovery at the companyâs Webbs Consol Project.

Exploration at the projectâs Tangoa West prospect has intercepted high-grade silver-lead-zinc-copper mineralisation over a thick drill intercept at shallow depths.

The find includes an aggregate 5.9 metres at 1,074 grams per tonne of silver equivalents within the broader intercept of 26.7 metres at 399 grams per tonne of silver equivalents.

That highlights potential mineralisation outside the subsurface below the project’s old workings. It also outlines potential mineralisation in surface targets with no previous mining.

Additionally, newly identified vertical mineralisation and alteration zonation could be good news for the current drilling program as previous programs seem to have only tested upper portions of mineralised lodes.

All that has excited the ASX mining share’s managing director, Ted Leschke.

“The high-grade silver-base metal discovery at Tangoa West ⦠extends the high-grade Webbs Consol mineral system to three kilometres,” Leschke said.

“In addition, the newly recognised vertical mineralisation and alteration zonation identified in drilling to date has strong implications for mineralisation at depth at Webbs more broadly”.

Tangoa West is one of several drill targets being tested at the project.

Lode Resources share price snapshot

Perhaps unsurprisingly, the ASX mining share has been performing well recently.

It has gained 22% in 2022 so far. It’s also currently nearly 93% higher than it was this time last year.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Brooke Cooper has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/fi0FTYX

The Weebit Nano Ltd(ASX: WBT) share price is charging higher today, gaining 19% in early trade to $2.33.

It’s now settled at $2.22, up 13.27% on yesterday’s closing price.

Shares in the company â which develops next-generation memory technologies for the global semiconductor industry â closed yesterday at $1.96 each.

So, why are investors bidding up the ASX tech shareâs price today?

A maiden public demonstration

The Weebit Nano share price is off to the races after the company reported today it will hold the first public demonstration of its ReRAM IP module.

That demonstration is intended to show the technologyâs real-world capability as a ânon-volatile memory (NVM) integrated into an actual subsystemâ. It will take place at the three-day Leti Innovation Days event, currently underway in France.

According to the release, the interactive presentation will demonstrate its Weebit ReRAM functioning as an NVM memory block. The module will be fed live images and should retain that data while powered off, then display the data separately.

The Weebit Nano share price could also be getting a boost from the company reporting it expects its ReRAM module to publicly demonstrate its faster write speed compared to typical flash memory technology.

Commenting on the demonstration, CEO of Weebit Nano Coby Hanoch said:

This is the first time we are publicly demonstrating our ReRAM embedded in silicon, less than a year after taping out the module. The demo of our ReRAM technology represents yet another key technical milestone as we progress toward full productisation. The demo will be a great asset for use in our sales activities with potential customers.

Weebit Nano share price snapshot

Faced with fast-rising interest rates that have hit almost every growth share, the Weebit Nano share price has struggled in 2022, down 20% after factoring in todayâs gains. By comparison, the All Ordinaries Index (ASX: XAO) is down 16% year-to-date.

Longer term, Weebit Nano shares are outperforming, up 44% over the past 12 months compared to an 11% loss posted by the All Ords.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/BFlGZOq

The Bega Cheese Ltd (ASX: BGA) share price is trading down again on Tuesday and is now 3.5% in the red at the time of writing.

Shares have taken a nosedive this week, in continuation of a downtrend started from 10 June. Since then, the Bega share price has sunk from $4.65 to $3.86 in early trade on Tuesday.

In wider market moves, the S&P/ASX 200 Index (ASX: XJO) has started in the green today and now trades 1% higher at 6,502.

What’s up with the Bega share price?

There’s been no market-sensitive news out of Bega’s camp lately.

However, the share did cop a downgrade from the analyst team at UBS last week. The broker reckons higher milk prices and other cost pressures are likely to pull Bega’s earnings lower in FY23.

“Input cost pressures mainly relate to increased milk supply costs, but also material increases in packaging, freight, labor and electricity,” the broker said.

It revised its FY23 earnings before interest, tax, depreciation and amortisation (EBITDA) to $214 million, down from a previous $245 million.

The UBS team now values Bega at $4.75 per share.

Following the downgrade, those at Bell Potter also cut recommendations to a hold at a $4.20 price target.

Meanwhile, Macquarie followed suit and cut its price target by 12% to $4.75 per share as well.

Despite the shift in sentiment, support remains behind Bega, with several brokers still constructive on its outlook.

Out of all analysts covering the share, almost 64% rate Bega a hold right now, versus 27% saying it’s a buy, according to Bloomberg data.

The consensus price target is $4.86 per share, per this list.

This year to date, shares are down more than 30%, as seen on the chart below.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

There’s no denying that it’s been an uphill climb for Wall Street and investors since the year began. Remember that fabled walk to and from school in three feet of snow, uphill, both ways, which your parents told you about as a kid? This is the stock market equivalent of it.

Since the three major U.S. indexes hit their all-time closing highs between mid-November and early January, the iconic Dow Jones Industrial Average(DJINDICES: ^DJI), broad-based S&P 500(SNPINDEX: ^GSPC), and technology-focused Nasdaq Composite(NASDAQINDEX: ^IXIC), have respectively tumbled by 19%, 24%, and 34%, as of June 16. More importantly, it firmly places the Nasdaq and S&P 500 in a bear market. The S&P 500 is often viewed as the best barometer of U.S. stock market health.

This indicator has correctly predicted five S&P 500 bear markets

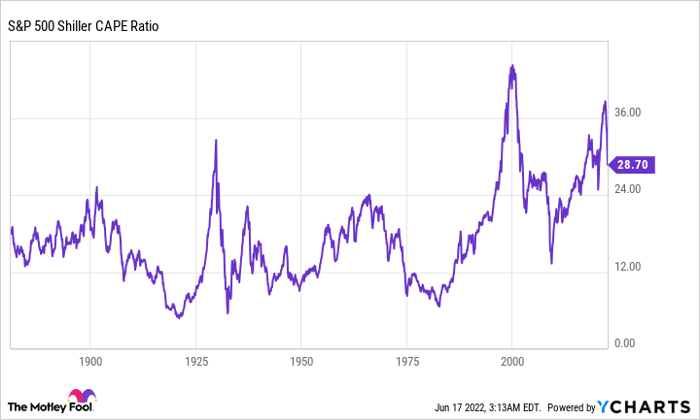

Although some investors might be surprised by the S&P 500 losing nearly a quarter of its value in just over five months, one telltale signal with an impeccable track record correctly predicted this tumble. That indicator is the Shiller price-to-earnings (P/E) ratio, which is also referred to as the cyclically adjusted price-to-earnings ratio, or CAPE ratio.

Whereas traditional P/E ratios compare the price of a security to its trailing12-month earnings or its forecast earnings for the current or coming year, the Shiller P/E ratio is based on average inflation-adjusted earnings from the previous 10 years.

The telltale bear market warning has occurred anytime the Shiller P/E has crossed above and sustained 30. Aside from the fact that the average Shiller P/E since 1870 is just 16.95, pushing above 30 has a notoriously bad track record:

1929: Following the Black Tuesday crash, the broader market went on to lose most of its value during the Great Depression. The Dow Jones ultimately shed 89% of its value.

1997-2001: The S&P Shiller P/E ratio would hit an all-time high of 44.19 immediately prior to the dot-com bubble bursting. Following the market’s peak, the S&P 500 lost about half its value.

Q3 2018: During the second half of 2018, the Shiller P/E ratio found its way, briefly, above 30. During the fourth quarter of 2018, the S&P 500 lost 19.8% of its value, or 20% on a rounded basis. A decline of 20% is the accepted threshold for a bear market.

Q4 2019-Q1 2020: In the six months leading up to the 33-calendar-day coronavirus crash, the S&P Shiller P/E ratio was, again, north of 30. The COVID-19 crash erased 34% from the S&P 500.

Q3 2020-Q2 2022: Finally, the S&P Shiller P/E topped 40 prior to the S&P 500 rolling over in early January 2022. Thus far, the index is down 24%.

To recap, that’s five instances since 1870 where the Shiller P/E ratio has topped 30, and five subsequent bear market retracements totaling 20% to 89%. It’s simply never been wrong.

However, there are a number of caveats that should be understood before proclaiming this the greatest bear market telltale signal of all time.

For example, valuation “norms” have changed significantly over the past century. Prior to the mid-1980s, computers weren’t exactly commonplace on Wall Street. It took quite a bit of time to disseminate information from businesses to Main Street, which allowed rumors to perpetuate. In other words, the environment wasn’t conducive to supporting lofty valuations.

Since the mid-1980s, the information barrier between businesses, Wall Street, and Main Street, has gradually disappeared. Today, John and Jane Q. Investor can access income statements, balance sheets, and management commentary at the click of a button. This ease of access to information drives more investor risk-taking and has, therefore, inflated the Shiller P/E ratio over the past 25 years.

Something else to consider is that, even though the Shiller P/E ratio has a perfect track record of predicting an eventual bear market once valuations become extended, there’s no telling how far above 30 it’ll climb, or how long the Shiller S&P 500 will stay above 30. If you’d bet against the benchmark S&P 500 when it first crossed 30 during the third quarter of 2020, you’d still be underwater today, even with a 24% decline in the index.

Also, take note that valuation isn’t always the reason a bear market takes shape. The COVID-19 pandemic that cratered the S&P 500 over the course of five weeks in 2020 had little to do with the perception of extended valuations.

Bear markets are a surefire buying opportunity for the patient

Although it may not seem like it at the moment, bear markets are, historically, the perfect time to invest.

When looking at the long-term performance of the S&P 500, one thing that’s abundantly clear is that bull markets last considerably longer than corrections (that is, declines of at least 10% from a recent high). Since the beginning of 1950, the aggregate number of days spent in a bull market outweighs days spent in correction by roughly 2.6-to-1. This means every sizable correction is an opportunity for patient investors to strike.

If you’re wondering where to invest, there are plenty of great ideas.

For instance, dividend stocks have a proven track record of outperformance. According to a 2013 report from J.P. Morgan Asset Management, a division of JPMorgan Chase, income stocks averaged a hearty 9.5% annual return between 1972 and 2012. By comparison, publicly-traded stocks that didn’t pay a dividend gained an average of only 1.6% annually over the same time frame. Because dividend stocks are almost always profitable and time-tested, they make a good case to increase in value over time.

Interestingly, growth stocks can be smart investments when the U.S. economy weakens and the S&P 500 enters a bear market. A Bank of America/Merrill Lynch study published in 2016 found that over a 90-year period (1926-2015), value stocks outpaced growth stocks in the return column (17% to 12.8%, based on average annual return). But during periods of weakness, growth stocks performed considerably better than value stocks. Â

Investors can also buy an S&P 500 tracking index. According to data from Crestmont Research, if you, hypothetically, were to have bought an S&P 500 tracking index and held for 20 years at any point since 1900, you would have generated a positive total return, including dividends. There isn’t a single point on the S&P 500’s rolling 20-year timeline where this statement doesn’t hold true.

Patience can pay off handsomely on Wall Street.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Sean Williams has positions in Bank of America. Bank of America is an advertising partner of The Ascent, a Motley Fool company. JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

from The Motley Fool Australia https://ift.tt/CNMQIOS

In early trading, shares in the integrated grains company are getting a boost. At the time of writing, the share price is 3.3% higher at $9.39. For context, the S&P/ASX 200 Index (ASX: XJO) is also up a lively 1.11% this morning.

Benefitting from a positive reaction to the contents of its latest presentation, Graincorp is leading the consumer staples sector out of the gates on Tuesday.

What’s growing the Graincorp share price today?

The grain logistics and storage company is getting extra attention on the ASX today. Typically, an investor presentation covers information already known by the market. However, today’s presentation has been marked as price-sensitive, indicating there are likely some important details hidden within it.

Before we dive deeper, here are a few main points that could be influencing the Graincorp share price:

Reaffirmed prior FY22 full-year guidance of $590 million to $670 million in underlying EBITDA

Dividend payout ratio target of 50% to 70% with “optionality to pay special dividends in years” ahead

Well-positioned amid global supply chain disruptions

Potential for third consecutive bumper crop across Australian east coast

Possibly the biggest takeaway from Graincorp’s presentation to shareholders is its insulation from some of the strongest pressures faced by other companies at the moment. For example, it touted its end-to-end supply chain along the east coast. This includes seven bulk grain port terminals and approximately 160 storage sites.

At a time when grain prices are at multi-year highs, the ability to deliver the product to ports and get it shipped is enabling the company to capitalise on the situation.

What else?

Importantly, the retained EBITDA guidance indicates Graincorp remains largely unaffected by the conflict in Ukraine. This is despite Europe and Ukraine exports making up 85 million tonnes of global exports.

Notably, the company highlighted its global footprint which has given the company some optionality. For example, Graincorp earmarked Canada as a “key part” of its multi-origin strategy.

More than anything, the presentation has likely provided reassurance to the Graincorp share price today. The company currently holds a market capitalisation of $2.14 billion.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Mitchell Lawler has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/zZG5Duy

The Altium Limited(ASX: ALU) share price is pushing higher on Tuesday.

In morning trade, the electronic design software companyâs shares are up 1.5% to $25.84.

Why is the Altium share price pushing higher?

As well as getting a boost from a rebounding share market, the Altium share price was given a lift from a broker note out of Bell Potter.

According to the note, the broker has reiterated its buy rating but cut its price target by 18% to $34.00.

Despite this cut, based on the current Altium share price, this suggests potential upside of over 31% for investors over the next 12 months.

What did the broker say?

With just nine days remaining in the current financial year, Bell Potter believes that âno news is good newsâ in respect to the companyâs guidance.

It commented:

Altium has undertaken various marketing initiatives this quarter which, while slightly different to years gone by, suggests the company is again targeting subscriber over revenue growth in H2. This is worth highlighting as Altium has provided both revenue and EBITDA margin guidance for FY22 â US$213-217m and lower end of 34-36% â so there is the potential that these initiatives put at least the revenue guidance at some risk.

We do not, however, believe this is the case as: 1. 1HFY22 revenue growth was strong; 2. Altium narrowed the revenue guidance range towards the upper end in late February knowing it would implement these marketing initiatives in Q4; 3. The strong momentum in Octopart in 1HFY22 is likely to continue into 2HFY22 and offset any weakness in China (due to lockdowns) and Russia (due to the war in Ukraine); and 4. No update has been provided to market.

In light of this, its analysts âbelieve the company is on track to achieve its FY22 guidance.â

Why did Bell Potter cut its price target?

Bell Potter advised that it has cut its target on the Altium share price to $34.00 to reflect âa material decrease in the relative valuations.â

Outside this, nothing else changes. It continues to forecast strong revenue and EBITDA growth through to FY 2024.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Altium. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/LsaArYH

The S&P/ASX 200 Index (ASX: XJO) has started the week poorly, continuing its sudden downturn in June.

Following Monday’s session, the benchmark had fallen more than 7% over the past five trading days, marking its worst week since the March 2020 COVID-19 selloff.

Despite the weakness, several brokers are bullish on the Telstra Corporation Ltd(ASX: TLS) share price. Shares in the telco have been volatile this year to date yet they are also trading back around pre-pandemic highs.

These brokers are bullish

According to the team at JP Morgan, Telstra is a buy right now. It values the telco at $4.80 and, in a recent note, says planned increases to FY23 mobile prices are a key driver for the share.

The broker lifted its revenue forecasts on Telstra and notes many customers are “down shifting to lower priced plans which now all include 5G”. JP Mogan said:

We believe the [revenue] increases were necessary to achieve the FY2025 targets Telstra outlined at the companyâs 2021 Investor Day.

After factoring in the impact of the pricing increases into our model we now forecast Telstra will achieve targeted mid-single digit Mobile services revenue growth to FY2025 with a 5.2% [annualised] growth rate.

Morgans is also positive on the share, highlighting sector tailwinds and Telstra’s potential to unlock further shareholder value.

The Morgans team is forecasting a 16 cents per share dividend payment in FY22 and FY23.

Both brokers make up the 57% coverage that rates Telstra a buy right now, according to Bloomberg data. The remainder are split to hold, with Barclay Pearce saying the company was a sell back in February.

From that list, the consensus price target is $4.48 per share, translating to around 17.5% return potential at the time of writing.

In the last 12 months, the Telstra share price has held a 9% gain after sliding around 8% into the red this year to date.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

The Galileo Mining Ltd(ASX: GAL) share price is charging higher in early trade, up 5.2%.

The ASX mining share closed yesterday trading at $1.54 apiece and is currently trading at $1.62 after shooting to $1.65 shortly after open.

Investor interest appears to be piqued by the latest results from the companyâs ongoing drill campaign.

What drill results were announced?

The Galileo Mining share is moving higher after the company reported positive results from its reverse circulation (RC) drilling program. The exploratory drilling is taking place at the Callisto discovery at Galileoâs Norseman project, located in Western Australia.

The miner said that all four of its first RC drill holes intersected wide zones of disseminated nickel and copper sulphide mineralisation.

The exploratory drilling is taking place in the same area where Galileo intercepted a sulphide layer associated with palladium, platinum, gold, rhodium, nickel, and copper. These results were announced 26 May, sending the Galileo Mining share price soaring higher on the day.

Commenting on the positive results, Galileoâs managing director Brad Underwood said:

The results confirm the consistency of the geology over the target area and the drill samples have been sent to the laboratory for analysis. Drilling is ongoing with another 16 holes planned over the next three to four weeks.

Additional Program of Work applications are awaiting approval with the Department of Mines which will allow further drilling along strike to the north. Presently we have shown mineralisation occurs over 250 metres across strike and, with five kilometres of prospective strike to the north, we have a lot more drilling to come.

The company expects the assay results from these first four holes in late July.

With high rainfall slowing the drilling program, Galileo is bringing a second rig to the site. Thatâs expected to arrive tomorrow. The miner plans to drill approximately 16 more holes in the current program.

Galileo Mining share price snapshot

The Galileo Mining share price has been a standout performer on the ASX this year, up 628% since the opening bell on 4 January. For some context, the All Ordinaries Index (ASX: XAO) is down 16% year-to-date.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/5kRPxvT

The NextDC Ltd(ASX: NXT) share price has come under pressure in 2022.

Since the start of the year, the data centre operatorâs shares are down 21%.

This has been driven by weakness in the tech sector and concerns over its exposure to rising energy prices.

Is the NextDC share price weakness a buying opportunity?

According to a note out of Morgans, its analysts believe the NextDC share price is trading at a very attractive level.

This morning its analysts have retained their add rating but trimmed their price target on its shares to $13.01.

Based on the current NextDC share price of $10.09, this implies potential upside of 29% for investors over the next 12 months.

What did the broker say?

Morgans has been looking into what impact rising energy prices would have on NextDCâs operations. The good news is that it doesnât expect any material impacts. It explained:

NXT typically contracts energy rates annually. We estimate that ~80% of FY23 power costs get passed straight through to its wholesale customers. The remaining ~20% is enterprise and subject to annual price reviews which are typically the greater of CPI or 2.5%. Enterprise contracts also allow NXT to pass on material structural changes in energy prices (which it has done once in the last decade).

The broker also sees rising energy prices as an “opportunity” for NextDC. This is due to the company being independently certified as the only Australian data centre provider with a NABERS 5-star rating for energy efficiency. It was also certified with PUE of 1.4 in FY 2021, which is well below the Australian industry average of 1.7.

Morgans feels that this efficiency could be attractive to prospective customers. It commented:

This means NXT is >50% more energy efficient than peers and much more energy efficient than on-premise. Customers looking to save money due to rising energy prices may well fast-track their migration to NXT.

Overall, its analysts âsee upside risk to FY23 consensus revenue and are comfortable with EBITDA.â

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor James Mickleboro has positions in NEXTDC Limited. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/APgB6wQ

What a rollercoaster ride it has been for the Zip Co Ltd(ASX: ZIP) share price.

From reaching an all-time high of $14.53 in February 2021, the buy-now pay-later (BNPL) shares are now trading at 53 cents. That represents a massive 96% decline in just 16 short months.

And even when you look at year-to-date, its shares are down 90%. This means the share price would need to increase by 900% to break even.

While you may think Zip shares are too cheap at current valuations, hereâs why I wonât be buying at all.

Investors fall out of love with the BNPL industry

The once gleaming BNPL industry was popular among investors as consumer trends shifted during the pandemic.

Government stimulus packages among record low interest rates drew an insatiable appetite for shoppers.

However, as quickly the BNPL market soared, it has now almost turned to dust.

To put that into perspective, Zip was once valued more than $6 billion at its height. More than retail giant, JB Hi-Fi Limited(ASX: JBH).

Today, the BNPL company has a market capitalisation of around $371.49 million. A staggering fall of 94%.

Why I wonât be a buyer of the Zip share price

With so many market entrants to the BNPL sector, it has become increasingly crowded.

Titled âApple Pay Laterâ, the service offering doesnât charge any interest or late payment fees to customers.

In addition, a number of major Australian banks such as Commonwealth Bank of Australia(ASX: CBA) have promoted their own offering.

Furthermore, Zip is experiencing credit losses outside its target range. With the latest figures at around 2.6% of total transaction volume, this may increase due to the current macroenvironment.

Interest rates hikes due to soaring inflation levels are leading some economists to predict a recession in 2023.

Essentially, what this means is that consumers are less likely to spend on discretionary items when interest rates are high. The cost of debt such as credit cards, personal loans and mortgage will require extra payments, affecting consumer spending habits.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

Motley Fool contributor Aaron Teboneras has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended ZIPCOLTD FPO. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/uH8mWIE