Over multiple decades, Warren Buffett’s investment strategy has been hugely successful.

The Oracle of Omaha’s long-term approach and investment in high-quality companies trading at fair valuations has allowed him to outperform the stock market and receive huge dividend windfalls each year.

The good news is that there’s nothing to stop you from following in Buffett’s footsteps, even from a starting age of 50.

In fact, by starting today, you could be generating a decent source of passive income in no time.

Passive income the Warren Buffett way

As mentioned above, one of the key parts of Warren Buffett’s investment strategy is to take a long-term approach.

Buffett isn’t interested in short-term fads. Instead, he seeks to maximise his returns over many years of compounding. There’s a very good reason for this. It provides the Berkshire Hathaway (NYSE: BRK.B) leader with the time his investments need to deliver on their potential.

A good example of this is actually the Berkshire Hathaway share price. There’s no doubting the company’s quality. But if you had invested in September 2021, your investment would have been down by approximately 5% a year later. No doubt you would have been somewhat disappointed at that point.

But if you fast-forward to today, its shares have climbed approximately 50% since September 2022. Clearly it has paid to be patient.

Now imagine that you kept doing this with a diverse portfolio of high quality, dividend-paying stocks with sustainable competitive advantages, in time they would start to provide you with a growing source of passive income.

But how much?

If you are in a position to invest $1,000 per month over 15 years and generated an average annual return of 10% (and reinvested your dividends), your portfolio would grow to be worth $400,000.

At that point, you could stop reinvesting your dividends and start using them as passive income. But how much income could you generate?

With a portfolio worth $400,000 and an average dividend yield of 5%, you would be pulling in $20,000 of passive income each year.

But it won’t stop there, even without any further contributions.

If your portfolio continued to grow by 5% each year after dividend redemptions, it would increase to $650,000 in 10 years. Earning a 5% dividend yield on this portfolio would mean passive income of $32,500.

It is also worth noting that by following Warren Buffett’s strategy of making patient investments in high quality companies with competitive advantages, it may be possible to beat the market returns and produce a larger portfolio and an even more generous source of income.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Berkshire Hathaway. The Motley Fool Australia has recommended Berkshire Hathaway. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/R4G1QbO

Investing legend Warren Buffett once said, “Never count on making a good sale. Have the purchase price be so attractive that even a mediocre sale gives good results”.

If you’re an admirer of the Oracle of Omaha (and, let’s face it, who isn’t?), you’ll likely already appreciate that the price at which you buy your ASX shares is just as important as that at which you sell!

But how to sort the oversold bargains from the falling knives?

For their thoughts, we asked our Motley Fool writers which ASX shares they reckon offer the best-value buying right now. Here is what the team came up with:

6 cheap ASX for February 2024 (smallest to largest)

Why our Foolish writers think these ASX stocks offer great value buying

KMD Brands Ltd

What it does: KMD Brands is a retail business that operates three leading brands: Kathmandu, Oboz and Rip Curl.

By Tristan Harrison: The KMD Brands share price is down 33% in the past year and has dropped close to 60% since October 2021.

The company’s recent trading update revealed group sales were down 12.5%, reflecting “ongoing weakness in consumer sentiment.” Kathmandu’s rainwear and insulation categories were down, while wholesale sales for Rip Curl and Oboz also declined as retailers reduced inventory holdings in the short term.

But there were some positives. The group gross profit margin improved, and operating costs were “well-controlled and actively managed”.

I think the current KMD share price reflects short-term weakness. Commsec numbers suggest earnings per share (EPS) could rise to 6.5 cents and 8.3 cents in FY25 and FY26, respectively. This puts the stock at 10x FY25’s and 8x FY26’s estimated earnings, which looks cheap to me. The FY26 dividend yield could also be an attractive 8.75%.

Motley Fool contributor Tristan Harrison does not own shares of KMD Brands Ltd.

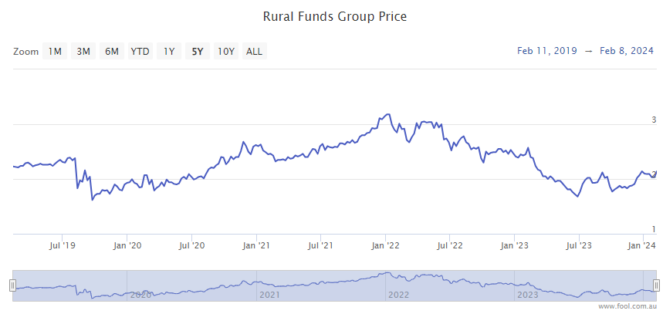

Rural Funds Group

What it does: Rural Funds Group is a real estate investment trust (REIT) that owns a large portfolio of farmland and other agricultural assets.

By Sebastian Bowen: The Rural Funds unit price has not had a fun time over recent years. Back in early 2022, units of this REIT were asking for more than $3 each. But today, those same units were going for $2.22 at Friday’s close of trade.

Rising interest rates have hurt Rural Funds. As an REIT, this trust uses loans and other financing to help build out its portfolio. With rising rates, this financing has become a lot more expensive.

Yet, I think this situation has resulted in Rural Funds stock becoming oversold. The REIT operates a strong portfolio of different agricultural assets, including vineyards, cattle and macadamia, almond, and cotton farms. Those are all commodities that have a strong and inelastic market.

Additionally, Rural Funds is a strong dividend payer, having increased or maintained its quarterly dividend payments since 2017. Today, you can expect a dividend distribution yield of more than 5.28% from this REIT.

Motley Fool contributor Sebastian Bowen does not own units of Rural Funds Group.

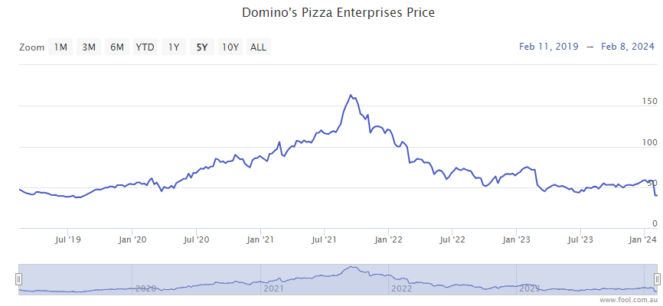

Domino’s Pizza Enterprises Ltd

What it does: Australian-owned Domino’s is the master franchise holder for Domino’s Pizza stores in Australia, New Zealand, Belgium, France, the Netherlands, Japan, Germany, Luxembourg, Taiwan, Malaysia, Singapore, and Cambodia.

By Bernd Struben: It’s been a rough start to 2024 for Domino’s shares, with the stock down 32% year to date. Most of those losses came on 25 January, when shares closed down 31%.

This followed an update that showed significant half-year sales growth in its ANZ home markets and Germany, but was overshadowed by a sales slowdown in Malaysia and Japan.

Management forecast net profit before tax for the half year between $87 million and $90 million, down year on year but up from $74 million in the prior half. It will now focus on delivering the same successful strategies driving growth in ANZ to boost its Asian operations.

The stock should also get a longer-term lift as slowing inflation and falling interest rates boost discretionary consumer spending.

Domino’s shares trade on a 2.8% partly-franked dividend yield.

Motley Fool contributor Bernd Struben does not own shares of Domino’s Pizza Enterprises Ltd.

Block Inc

What it does: Block Inc is a US fintech that provides payment terminals for small retailers, a consumer finance app, and Afterpay, to name a few of its offerings.

By Tony Yoo: It might be odd calling a stock that’s risen 70% since the end of October “oversold”. But the fact remains the Block share price is more than 14% down over the past year and 43% lower since April 2022.

The financial services company is on the way up after cleaning up its act in recent months. Management has cut costs, reduced staff share issuances, and generally placed a greater emphasis on cash flow. The revival in the Bitcoin price has helped too, with co-founder Jack Dorsey a firm believer in cryptocurrencies.

All three analysts currently surveyed on CMC Invest rate Block shares as a strong buy.

Tony Yoo does not own shares of Block Inc CDI, but does own Block Inc shares listed on the NYSE.

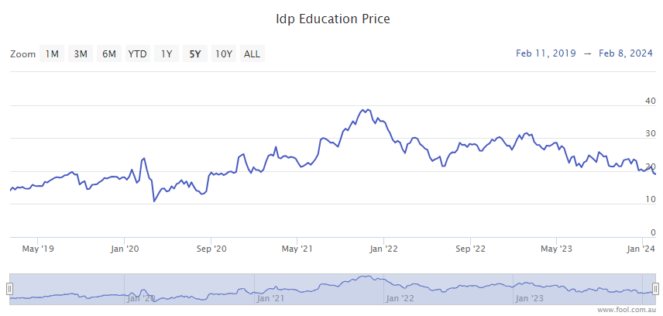

IDP Education Ltd

What it does: IDP Education is a provider of international student placement services and high-stakes English language testing services.

By James Mickleboro: IDP Education shares have lost almost 40% of their value over the last 12 months after the company was hit with bad news after bad news. This included the loss of its language testing monopoly in Canada and changes to student visas at home and abroad.

While these events have undoubtedly had a negative impact on the stock’s near-term performance, I believe the selling has been severely overdone. In light of this, I feel it has created an opportunity for ASX investors to buy a high-quality company with strong long-term growth potential.

Analysts at Goldman Sachs agree with this view and remain bullish on its outlook. The broker highlights that “IEL’s fundamental quality and structural growth drivers remain intact while the company possesses levers to continue to grow earnings (e.g. costs).”

Goldman currently has a buy rating and a $27.60 price target on IDP shares.

Motley Fool contributor James Mickleboro does not own shares of IDP Education Ltd.

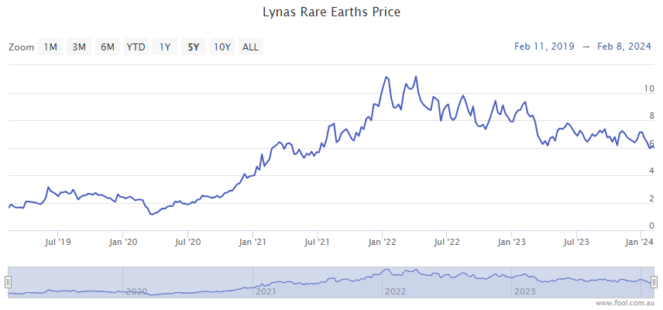

Lynas Rare Earths Ltd

What it does: Helmed by Amanda Lacaze, Lynas Rare Earths is one of the largest producers of rare earth elements, which are critical in many of our modern-day technologies. The company owns two highly regarded operations: the Mount Weld mine in Western Australia and a processing plant in Malaysia.

By Mitchell Lawler: The past year has not been kind to the Lynas share price. Coinciding with a drop in the going rate for rare earths, shares in the Australian miner have fallen 35% to reflect the shrinking revenue and profits.

I’ll go out on a limb and say this could all be a temporary weakness in an otherwise strong long-term outlook. Interest rates have constricted the consumer’s appetite for electric vehicles recently, but with rates expected to be cut at the tail end of 2024, we may soon see strength again.

I think Lynas’ current valuation is appealing based on the company’s recently increased production capacity and the Kalgoorlie facility achieving its first feed-on in December last year.

Furthermore, management’s decision to pursue organic growth over a merger with MP Materials relays a level of confidence among management in the company’s own future prospects.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Block, Domino’s Pizza Enterprises, Goldman Sachs Group, and Idp Education. The Motley Fool Australia has positions in and has recommended Block and Rural Funds Group. The Motley Fool Australia has recommended Domino’s Pizza Enterprises and Idp Education. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/tT0zR1c

Many people lament that all the technology that’s meant to help us feels like it’s actually burdened us with more things to monitor and action.

“Excuse me then if I’m a bit too busy to comment on your social media post about the sunset, answer your email survey, or pick up the phone to your stupid call centre,” said Marcus Today founder Marcus Padley.

“Sorry, but I’ve got a bit going on of my own.”

Because of this rushing around, Padley said on the Marcus Today blog, “the most precious gift you can give anyone these days, especially your family and kids, is time”.

“Simply turning up, ringing up, listening, and being there is now the biggest compliment you can ever pay anyone.

“Time. The most valuable asset on earth, and the most generous of gifts. Use it or lose it. Make it or waste it.”

So with that in mind, Padley used his vast investing experience to identify the top 10 time-wasters that investors need to ignore.

Spending your most valuable asset on any of these is time taken away from taking proper care of your ASX investments:

Useless information

The first three are all related to information that add little value to your investment decisions: Powerpoint presentations, clickbait, and media talking heads.

“PowerPoint has empowered even the most unimaginative, reclusive, bland, but credentialled introverts to present ‘well’. It is that good. Which is bad,” said Padley.

“Clickbait journalism has degraded the integrity of financial content, which is now being written for the internet, not for the reader.”

Padley himself appears on television regularly to talk about ASX investments, but he warns that it’s just for fun.

“We may look good and put on a good show, but we have no more ability to predict the future than you do. Take it for what it is, an entertainment, a show. But we are not clairvoyant.”

Human emotions

Paying attention to your own emotions is one of the biggest time-wasters for your ASX investments.

“[Emotions] do nothing for the investment process. Don’t let them get in the way,” said Padley.

“There is no ‘liking’ or ‘hating’ stocks. What you feel about a stock is irrelevant. Think like ‘Spock’. Be an algorithm. Dispassionate analysis is the goal.”

He has one tip to put this in practice.

“If you have a ‘feeling’ about a stock, you should be removed from your own investment process immediately.”

Thinking about the price you paid for your ASX investments

There is absolutely no point in worrying about the price you paid for an ASX stock.

The market doesn’t care, the stock doesn’t care, and nor should you.

“What you paid for a stock is completely irrelevant. Whether you are in profit or loss has absolutely no bearing on the future share price. So be detached,” said Padley.

“A client once said to me ‘Telstra Group Ltd (ASX: TLS) owes me five dollars’. No it doesn’t, it’s not your brother-in-law.”

Economists

Investors need to be acutely aware that all those economists from the big banks and investment houses have a financial interest in always being on the optimistic side.

Their predictions are not unbiased.

“They have a mission, to keep the clients of their large product selling wealth management companies happy and invested.”

Economist forecasts are simply to provide “a perception of control and certainty”

“They cannot afford to speak their minds, and they simply cannot tell anybody to sell, ever.”

False prophets and idols

Padley is not a fan of broker research, financial services peddling urgency, or anyone claiming to invest the same as Warren Buffett.

“Sorry, but you are not Warren Buffett, and you cannot do what he does, or someone would be doing it for us, and we would all be billionaires.

“So stop pretending you can.”

He cautions investors to always think about the motivations of a broker making a particular stock recommendation.

“90% is marketing. 90% of it is designed to promote a corporate client. 90% of it is designed to suck up to a corporate client. It is not independent advice,” said Padley.

“It is not designed to make the reader money. It is designed to make the broker money. Read it with your eyes open to the corporate purpose.”

And rushing investment decisions inevitably ends in tears.

“There is no rush when it comes to the core purpose of a stock market investor, picking stocks over long periods, not snagging a lucky rise tomorrow.

“Being urgent has but one destiny in a stock market context.”

Artificial intelligence

AI is wasting everyone’s time, according to Padley.

“Send me an email written by AI, and not only can I spot it, but it’s an insult.

Not to me, but to you. To your intelligence. We’re all going to become acutely aware of it, very quickly. It’s not impressive. It’s a bit pathetic.”

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tony Yoo has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has positions in and has recommended Telstra Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/kKaUR0u

Putting forward an ASX share that someone could rely on forever in an investment portfolio is no small potatoes. The investing world is littered with the graves of companies that once seemed unassailable, and whose fortunes many could never see fading – until they did. Kodak, Blockbuster, Borders, Ansett… the list is endless.

But today, I’m going to attempt this hard task, and discuss five ASX shares that I think are worthy candidates for a buy-and-hold-forever investment.

For as long as humans have been around, we’ve loved a flutter. And that’s the basic tenet that underpins my faith in this gaming company. Lottery Corp is the name that has exclusive rights to run lotteries and Keno services in almost all Australian states and territories. Many of these licenses only expire in many decades’ time.

I love lotteries from an investment perspective. The allure of buying a relatively cheap ticket in the hopes of winning it big is something that fundamentally attracts us all, and is also immune from normal economic maladies like inflation and recessions.

Safe in this knowledge, I’d be happy to name Lottery Corp as a buy-and-hold-forever investment.

Telstra has been a constant national companion throughout modern Australia’s history. First as the Postmaster General’s Department, then as the state-owned Telecom and now Telstra, this company has always underpinned our national communication services.

With the paramount importance of high-quality mobile connections and fast home internet in our modern economy, Telstra’s role as the go-to telecommunications services provider has arguably never looked more important.

Given this importance, I can’t envision a future where Telstra is not a major facilitator of this important facet of our economy and daily life. The company’s dominance in mobile and home internet connections gives it a highly defensive earnings base, as well as significant pricing power.

That’s why it’s my belief that Telstra will continue to be a quality investment for decades to come.

This one is a little easier to tout. No matter the advances in technology that we might see over all of our lifetimes, the fact remains that we’ll need to eat, drink and stock our households. And Woolworths is probably going to remain the first choice of more Australians than any other to provide these services.

The company’s investments in automation, click-and-collect services, and home delivery have impressed me in recent years. No matter what happens with new technologies in the grocery space, I expect Woolworths to be leading the charge. As such, I’d be happy to label this company as a top buy-and-hold stock for ASX investors today.

Changing tack a little now, let’s discuss an exchange-traded fund (ETF). The Vanguard Australian Shares ETF is an index fund that faithfully holds a sliver of the 2300 largest shares on the ASX, weighted by market capitalisation. Whatever the largest 300 companies on the ASX are at any given moment, VAS will hold their shares within its portfolio.

This index fund structure inherently future-proofs this investment.

Let’s say, for argument’s sake, that Commonwealth Bank of Australia (ASX: CBA) and BHP Group Ltd (ASX: BHP) end up being usurped as the largest bank and miner on the ASX by the year 2060 by Bank of Queensland Ltd (ASX: BOQ) and Champion Iron Ltd (ASX: CIA). Well, instead of holding CBA and BHP shares as some of its largest investments (as is currently the case), VAS will instead be holding BoQ and Champion Iron.

This ETF is an easy and hassle-free way of investing in ASX shares in a passive manner. As such, I would happily recommend it to any investor looking for a future-proof investment.

Last but not least, let’s talk about another ETF. The iShares S&P 500 ETF is another index fund. It works in a similar fashion as VAS, holding a huge range of different companies, weighted by size. But instead of the largest 300 Australian shares, this ETF tracks the largest 500 shares listed on the US markets.

That’s everything from Apple, Microsoft and Amazon to Exxon Mobil,Walmart and Coca-Cola.

The United States of America has, for more than a century, been the home to the lion’s share of the world’s greatest and most successful companies. Despite challenges from other countries like China, I don’t see this changing anytime soon. As the legendary Warren Buffett likes to say, “never bet against America”. So why not bet on America with this simple, hands-off index fund?

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Foolâs board of directors. Motley Fool contributor Sebastian Bowen has positions in Amazon, Apple, Coca-Cola, Microsoft, Telstra and Vanguard Australian Shares Index ETF. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Amazon, Apple, Lottery, Microsoft, Walmart, and iShares S&P 500 ETF. The Motley Fool Australia has recommended Amazon, Apple, Telstra and iShares S&P 500 ETF. The Motley Fool Australia has positions in Telstra Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/ZibKw3n

On Monday night, I submitted my order to buy moreApple Inc (NASDAQ: AAPL) shares, now the third-largest position in my portfolio.

I know what you might be thinking… pouring more money into a company with a US$2.9 trillion market capitalisation, valued at nearly 30 times earnings, and expected sales decline of its core product (the iPhone) — he’s lost the plot this time.

Yet, there I was, in the late hours of the night, gleefully adding to my shares in the 48-year-old US tech giant. See, I think many onlookers are missing the forest for the trees amid Apple’s newest addition to the product lineup: Apple Vision Pro.

Reminiscent of the iPhone release

Frivolous and unduly expensive… terms that some might label the futuristic-looking augmented reality headset. Does it sound familiar?

Source: Apple Vision Pro, Apple.com

At US$3,500, the Vision Pro headset (pictured above) is certainly not a cheap piece of gear. However, the original iPhone was not either when it launched in 2007.

Apple’s first crack at a cell phone carried a price tag of US$499, or US$733 when adjusted for inflation, at a time when other phones valued between US$350 to US$400 were considered the top end. Plenty of naysayers dismissed the product, overlooking the value of its exceptional software and interface.

The real ‘aha’ moment came when developers flocked to iOS. Quality touchscreen displays unlocked endless possibilities for entertainment and productivity applications, allowing customers to assign more value to the iPhone beyond ‘just a phone’.

I’d argue the same could be true of Vision Pro once developers exploit the immersive interface.

A new wave for Apple shares?

Apple App Store developers generated US$1.1 trillion in billings and sales in 2022. Owning this enormous ecosystem, Apple collects fees of between 15% and 30% on its sales. This revenue stream forms part of the company’s ‘services’ segment, which accounted for about 19% of net sales in Apple’s last quarter.

The services category is critical to why I bought more Apple shares. As more use cases are addressed by apps, Apple can clip the ticket at near-nil cost.

With more of our everyday tasks and activities passing through a glass display, Apple’s toll booth-style business has delivered solid growth. Now imagine a world where even more actions (both menial and masterful) are traversed through an Apple product.

With our SurgicalAR trace registration, surgeons can now visualize a 3D holographic rendering of a patient’s anatomy mapped directly onto them in real-time. No more alternating views. No more cognitive gymnastics. Just an immersive, precise and confident approach to #neurosurgerypic.twitter.com/gMikonOMp9

So here’s my elevator pitch on why I loaded up on Apple shares…

Developers will find more innovative ways to utilise Apple’s new platform over time. The hands-free, immersive experience lends the Vision Pro to high-value use cases. For this reason, Apple’s digital toll booth could see an order of magnitude more money flow through it in the next decade.

Meta Platforms Inc (NASDAQ: META) is the only serious competitor currently with its Meta Quest 3. As such, there’s a real chance a duopoly could form, allowing both companies to realise incredible shareholder returns.

Given Apple’s track record of marrying hardware and software, I’m confident it will repeat its success in the headset domain.

Apple shares now account for 7.9% of my portfolio after this week’s investment.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Motley Fool contributor Mitchell Lawler has positions in Apple and Meta Platforms. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Apple and Meta Platforms. The Motley Fool Australia has recommended Apple and Meta Platforms. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/eWudplI

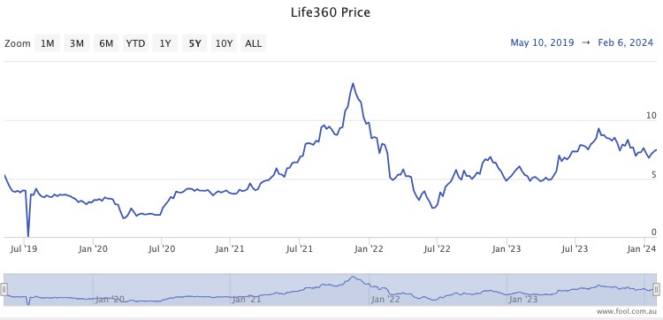

Californian software maker Life360 Inc (ASX: 360) is about to reach a milestone.

May will mark its fifth anniversary listed on the ASX.

After a topsy-turvy half-decade as a public company on the Australian exchange, I reckon Life360 shares are priced right to buy at the moment.

Let’s explore:

What does Life360 do?

Life360 Inc’s bread-and-butter business is its mobile app, also named Life360.

That app is best described as family security software.

It allows parents to track the location of their children, alerts family members if there has been a car accident, provides roadside assistance or emergency services if someone is stranded, and monitors for identity theft.

The smartphone app is most popular in its native country, the United States.

In a business update in November, co-founder and chief executive Chris Hulls revealed that global monthly active users (MAU) had just gone up 24% year-on-year to 58.4 million.

In the iPhone app store, Life360 is ranked #8 in the social networking category, sitting among other popular tools like WhatsApp, Telegram and Facebook.

Screenshot of iPhone app store (Source: Tony Yoo)

But the real ace up investors’ sleeves is that the business spent much of 2022 and 2023 turning itself from a cash-burning startup to a more mature business that focuses on the bottom line.

While the full 2023 calendar and financial year result will be announced on 1 March, the quarterly numbers already show the reforms are working wonders.

The net loss added up for the first through third quarters in 2023 was around US$25 million. For the whole of 2022, Life360 lost a whopping US$135 million.

Why are Life360 shares such a bargain right now?

The focus on cash flow, the fast-growing user population, and the app’s ability to raise prices without losing too much clientele all bode well for the future.

And historically Life360 shares seem to be reasonably cheap at the moment.

Back in 2019, the initial public offering (IPO) saw shares issued at $4.79. Subsequent excitement about the company rocketed the stock to the high $13s late in 2021.

But after the inflation-induced market selloff, Life360 shares are now hovering in the mid to high $7s.

Professional investors are certainly licking their lips at the prospect of future gains.

Broking platform CMC Invest currently shows five out of six analysts rating Life360 as a strong buy.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tony Yoo has positions in Life360. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Life360. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/w50SVok

It was a bumpy but overall positive end to the trading week for the S&P/ASX 200 Index (ASX: XJO) and ASX shares this Friday. Today’s modest gain means that the share market has notched three green days in a row.

The ASX 200 managed to pull off a modest rise for today’s session, gaining 0.073% to finish the week at 7,644.8 points.

This happy wrap-up for ASX shares comes after another strong night up on the US markets overnight.

The Dow Jones Industrial Average Index (DJX: .DJI) was a little wobbly but finished its trading with a 0.13% rise.

The Nasdaq Composite Index (NASDAQ: .IXIC) did a little better again, rising by 0.24%.

But back to the ASX now, let’s check out how the various ASX sectors finished up this Friday.

Winners and losers

Despite the market’s positive finish, there were still quite a few sectors that went backwards today.

Chief amongst those was energy stocks. The S&P/ASX 200 Energy Index (ASX: XEJ) had a shocker today, cratering by another 1.32%.

Utilities shares were another notable loser, with the S&P/ASX 200 Utilities Index (ASX: XUJ) shedding 0.85%.

Gold stocks weren’t having fun today, either. The All Ordinaries Gold Index (ASX: XGD) suffered a 0.67% sell-off.

Broader mining shares had a similar experience. The S&P/ASX 200 Materials Index (ASX: XMJ) ended up retreating by 0.28%.

Consumer staples stocks were also on the nose, evidenced by the S&P/ASX 200 Consumer Staples Index (ASX: XSJ)’s drop of 0.05%.

Our final loser was the industrials space. But the S&P/ASX 200 Industrials Index (ASX: XNJ) barely moved, inching down by just 0.01%.

Turning now to the winners, and tech stocks were the best place to be today. The S&P/ASX 200 Information Technology Index (ASX: XIJ) had a cracker, surging by 1.13%.

Healthcare shares were also on fire, illustrated by the S&P/ASX 200 Healthcare Index (ASX: XHJ) gain of 1% on the dot.

Communications stocks had a top time today too. The S&P/ASX 200 Communication Services Index (ASX: XTJ) shot up 0.8% by the end of trading.

ASX consumer discretionary shares were also in demand, as you can see from the S&P/ASX 200 Consumer Discretionary Index (ASX: XDJ)’s 0.27% bump.

Financial shares were our final winner. The S&P/ASX 200 Financials Index (ASX: XFJ) banked a lift of 0.09% this Friday.

Top 10 ASX 200 shares countdown

Today’s index gold medallist was lithium stock Liontown Resources Ltd (ASX: LTR). Liontown shares bounced by a healthy 10.4% up to $1.115 each by the end of trading. This healthy spike came despite no obvious catalyst, news or announcements from the company.

Here’s how the rest of today’s best-performing stocks stand:

Our top 10 shares countdown is a recurring end-of-day summary to let you know which companies were making big moves on the day. Check in at Fool.com.au after the weekday market closes to see which stocks make the countdown.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Sebastian Bowen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Cochlear and REA Group. The Motley Fool Australia has recommended Cochlear and REA Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/yEbS2io

Goldman Sachs believes that this language testing and student placement company’s shares are significantly undervalued following a recent selloff.

Its analysts have a buy rating and $27.60 price target on its shares. This implies potential upside of 43% for investors over the next 12 months.

While Goldman acknowledges that there has been a series of negative events that could impact IDP Education, it remains very positive and believes that structural tailwinds will underpin very strong medium term growth. It said:

IEL trades at 28x our 12mf EPS estimate vs 45x historically and against a +17% FY23-26E EPS CAGR. Reiterate Buy into a strong 1H result where we sit +10% ahead of VA Consensus EBIT based on a strong start to FY24E as seen in the available visa data. News flow may continue to be choppy, however IEL’s fundamental quality and structural growth drivers remain intact while the company possesses levers to continue to grow earnings (e.g. costs).

Goldman Sachs also sees major upside potential for this enterprise software provider’s shares.

It currently has a buy rating and a $4.50 price target on the ASX growth share. This implies a 12-month potential return of over 30% for investors.

Goldman likes Readytech due to its positive growth outlook and attractive valuation. It said:

We believe RDY remains undervalued compared to SaaS peers on an absolute and growth adjusted basis, trading on 11.5x FY24E EV/EBITDA vs a 19% FY23-26E EBITDA CAGR or a growth-adjusted multiple of 0.6x vs peers typically at ~1.5x.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group, Idp Education, and ReadyTech. The Motley Fool Australia has recommended Idp Education and ReadyTech. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/aZkMKLb

Brickworks Limited (ASX: BKW) shares are a popular option for investors.

And luckily for them, the building products company’s shares have been on a roll of late.

For example, in afternoon trade, the company’s shares are up almost 1% to $28.78.

This leaves them trading within a fraction of their record high of $29.32. In addition, it means they are now up by a sizeable 18% since this time last year.

The question now, though, is whether its shares have peaked or can keep rising from here. Let’s find out what analysts are saying.

Can Brickworks shares keep rising?

The general consensus at present is that the company’s shares are fully valued right now.

For instance, two brokers that have the equivalent of buy ratings on its shares have price targets that are either in line with its current price or lower that it.

Bell Potter has a $27.80 price target and UBS has a $29.00 price target.

Elsewhere, analysts at Macquarie, Morgans, and Ord Minnett all have the equivalent of hold ratings on Brickworks’ shares with price targets suggesting downside of 6% to 14%.

It’s not all doom and gloom

There is one broker that has broken from the pack and still sees major upside potential for investors.

A note out of Citi last month reveals that its analysts have retained their buy rating and lifted their price target to $35.00. This implies potential upside of almost 22% for investors over the next 12 months.

Citi thinks that investors should look past near-term concerns about Brickworks’ property earnings and is tipping higher capital value realisations from this side of the business in future. The broker said:

With peaking rates in sight, we believe further valuation declines may be limited and the tight demand supply dynamics in the industrial market could create further rental upside.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Citigroup is an advertising partner of The Ascent, a Motley Fool company. Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Brickworks and Macquarie Group. The Motley Fool Australia has positions in and has recommended Brickworks and Macquarie Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/MACvNKF

Dicker Data Ltd (ASX: DDR) shares are ending the week on a positive note.

In afternoon trade, the computer hardware and software distributor’s shares are up 2% to $11.50.

Why are Dicker Data shares pushing higher?

Investors have been buying the company’s shares today after it announced its latest quarterly dividend.

According to the release, the company has declared a 15 cents per share fully franked dividend for the three months ended December 31. Management notes that this “is in line with the Company’s policy of paying out 100% of net profit after tax (NPAT).”

Dicker Data’s final dividend is up significantly on last year’s final quarterly dividend of 2.5 cents per share and will mean an increase year on year.

The company has already paid out 10 cents per share fully franked dividends for each of the first three quarters of FY 2023. This means Dicker Data will have distributed a total of 45 cents per share to its shareholders come pay day, which represents an 8.4% increase on the 41.5 cents per share that was paid out in FY 2022.

Based on where Dicker Data shares currently trade, this represents an annual fully franked dividend yield of 3.9%.

When is pay day?

The record date for this final 15 cents per share dividend will be 15 February, with the payment expected to be made the following month on 1 March.

In between those two dates, shareholders can look forward to hearing from management when it releases its full year results. The company is scheduled to release its number on Tuesday 27 February.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Dicker Data. The Motley Fool Australia has positions in and has recommended Dicker Data. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/ZEq0WNf