The S&P/ASX 200 Index(ASX: XJO) has continued its poor form of the week so far this Thursday. At the time of writing, the ASX 200 has lost another 0.64% and is now trading at just under 7,450 points.

So let’s look at something different and take a glance at which shares are sitting atop the ASX 200’s share volume charts, according to investing.com.

The 3 most traded ASX 200 shares by volume this Thursday

ASX 200 telco Telstra is our first cab off the rank today. Telstra has had a notable 12.11 million shares swap hands as it currently stands on the markets. This telecommunications company seems to be defying the mood of the broader market and is currently up 0.9% at $3.97 a share. The company is also continuing to regularly buy back its own shares. This is probably why Telstra is appearing on this list today.

Paladin Energy is next up today. This ASX 200 uranium share has watched as 24.39 million of its shares have found a new home thus far. Yesterday, Paladin announced the completion of a $200 million share purchase plan, which saw the company’s share price drop at the time. However, today, investors seem to have had a change of heart. Paladin shares are now up by 4.2% at 81 cents apiece. This is probably the source of this elevated trading volume.

AVZ Minerals is our third and final share to check out today. This ASX 200 lithium hopeful has had a whopping 31.88 million shares bought and sold on the markets thus far. Again, there has been no major news or announcements out of this company today. So we can probably attribute this volume down to the share price fall AVZ has endured over today’s trading. The AVZ Minerals share price is currently down by 2.62% at $1.12.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the five best ASX stocks for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now.

Motley Fool contributor Sebastian Bowen owns Telstra Corporation Limited. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia owns and has recommended Telstra Corporation Limited. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/OC84Eks

Two separate markets, one similar industry. That’s an easy way to categorise this pair of interesting tech names that are currently triangulating around the scene.

Each of Archer Materials Ltd(ASX: AXE) and Brainchip Holdings Ltd (ASX: BRN) has been beaten down in the last month whilst the broader tech sector has jumped into the green.

Tech names, in general, have snapped back over the last month, with the S&P/ASX All Technology Index (ASX: XTX) – a proxy for the ASX tech sector – shooting up 5% in that time.

Why don’t we do a quick comparative analysis on both of these shares to get a better understanding of what’s driving each name, and then we’ll see what the market is saying.

Brainchip versus Archer – descriptive analysis

Whilst both companies operate in the same industry, each has fairly different addressable markets. First, let’s look at a brief description of each security.

Brainchip operates as a holding company. Through its subsidiaries, it provides neural computing technology solutions. It also provides artificial neural networks, software and digital hardware solutions in both the US and Australia.

It currently trades at 93.25 cents, well off its 52-week high of $2.34, but above its yearly low of 36 and a half cents. It has a market capitalisation of around $1.6 billion, and printed revenue of $1.6 million in 2021, up from $120,000 a year prior.

Archer Materials on the other hand operates as a technology company. It develops and then commercialises advanced semiconductor devices. The application of its chips ranges from quantum computing to medical diagnostics to mineral exploration. It has a global footprint.

Archer is trading down today at 88.5 cents and that’s a hefty slice off its 52-week high of $3.08 and actually closer to its 52-week low of 66.5 cents, set back in May 2021.

Archer’s market capitalisation of just $217 million places it in the small cap category as well. The company hasn’t secured revenue yet but recorded a net loss after tax of $2.8 million last year.

Fundamental flavour

There’s plenty that can be said about each company’s operating lines and the strengths and weaknesses of various product offerings. That’s not for this analysis. Here we’ll look at some of the numbers for a more informed and objective take. All measures are per Bloomberg data.

Ratios are a great way to bring two companies into the same line to make this comparison. We can use data obtained from the ratios to examine whether each name is performing well or not.

For instance, both companies aren’t profitable right now, in the sense they’ve both recorded after-tax losses in the last reporting period. That has an impact on certain measures of profitability.

Even still, Brainchip’s return on common equity (ROE) came in at -114% in H2 FY21, whereas Archer saw a -30% ROE.

Elsewhere, Brainchip’s gross margin of 82% stands out, as Archer hasn’t printed or recognised revenue from its operations just yet.

Instead, Archer recorded other comprehensive income of $1.72 million in 2021, mainly due to the sale of assets of $1.7 million to Chem X Materials Pty Ltd.

Both companies were also cash flow negative in their last half-yearly set of accounts, spending more on operations than earning in customer receipts.

Archer has a debt ratio of just 0.08% whereas its competitor here has a ratio of 8.6%. But that doesn’t mean to say it has an unhealthy balance sheet – both of these figures show each company is lowly geared with little debt. That could be a good sign in a world of rising interest rates.

In fact, Brainchip has ample liquidity, as short-term obligations are covered around 7x from and 6x from cash on the balance sheet.

Also, both companies appear to have a sufficient cash runway to last over the next 2 years, as determined by a funny little metric that analysts use, called the Altman’s Z-score.

The score takes various metrics from the financial statements and is used to predict a company’s likelihood of going bankrupt in the next 2 years, with surprising accuracy. A score of 2.99 or more indicates this safety. Brainchip and Archer are at 94.5 and 338 respectively.

Share price performance

Archer shares have compressed down in the last 12 months and have shaved 21% in that time. From their peak, shares have lost exactly two-thirds of their value at the time of writing, and are down another 8% this past month.

Brainchip shares on the other hand have had a similar outcome albeit a little bit further down the track (see below). Except, the company has held onto gains and is now up 70% in the past year and 37% in the past month of trade.

Whilst shares have retreated heavily in 2022 after going vertical in January, they are still quite top heavy and are floating well above 3 and 5 year highs.

Both stocks have also moved largely independently of each other over the last 12 months. Even more curious is, that Brainchip has moved pretty much on its own, despite what’s happened in the tech sector over this time. Let’s explain.

A commonly used term in finance is a statistic known as the stock’s ‘beta’; simply a measure of how closely it moves in unison relative to moves in the market (or an index).

A beta of 1 means the stock is perfectly correlated. It and the index move directly in unison, whilst minus 1 moves directly inversely to the index. A score of zero has no correlation whatsoever.

In this case, we’ll use the S&P/ASX All Technology Index, and what we’re trying to examine is what direction each stock moves when the index spikes up or down, and by how much. Typically, tech stocks move almost in unison with the wider tech sector and are called ‘high-beta’ stocks for that reason.

But not Brainchip. For the last 2 years its beta is -0.156, meaning that, on average, each move in the tech index has had little to no impact on the Brainchip share price.

In comparison, Archer has moved more closely. Its beta score is 0.87 – closer to 1 – meaning it has a much higher correlation to movements in the index.

Important to note, is that correlation doesn’t equal causation – these measures don’t show what’s causing the share price to change, rather how closely it moves compared to another benchmark.

These calculations, drawn from historical data, have implications on factors like diversification in portfolios, and also security selection – particularly at the professional level (think fund inclusion etc).

Valuation

Analysts haven’t glossed over both of these companies in enough detail to provide a comprehensive discounted cash flow valuation based on future cash flow projections.

Instead, we can look at valuation multiples for an apples-to-apples here. Archer is trading at 6.9x its book value of equity (P/B) but hasn’t printed sales, so P/B is what we need to focus on.

Brainchip on the other hand is trading at a P/B of 62.5x – but it has printed revenue, unlike its foe here, and warrants the premium. Although, it is trading at more than 750x sales – hardly a bargain.

Checking growth of these measures compared to each company’s enterprise value (EV) growth is a method that analysts use to assess the value of early-stage players with little earnings data to go by.

Brainchip’s EV has climbed 128% since 2020 and over 1,500% since 2018, compared to P/B growth of 106% and 612% in the same periods.

Meanwhile, Archer’s EV has grown 51% since 2020 and 950% since 2018, with P/B expanding just 25% and 538% in those times respectively.

Compare this to the benchmark S&P/ASX 200 Index (ASX: XJO), whose market cap has grown by 19% and 47%, whilst its P/B has grown by 9.5% and 21%.

Therefore it could be that Brainchip has created more value for its shareholders, outpacing Archer and smashing the benchmark in growing the book value of its equity. This has come alongside growth in its share price. What this means in terms of valuation – the market will decide.

Has it created more value for shareholders? I’ll let you be the judge.

Foolish takeaway

Both shares are running at different paces this year, but it’s interesting to know that they aren’t necessarily dancing to the tune of the tech sector.

Analyst opinion on each is very light and there are a lot of assumptions baked into each company’s forward revenue projections.

Nevertheless, whilst both shares have garnered serious attention over the last 12 months, there’s no telling in what direction the market will move next, let alone these two individual names.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the five best ASX stocks for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now.

Motley Fool contributor Zach Bristow has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/OenCZtr

The S&P/ASX All Ordinaries Index (ASX: XAO) is in the red today, down 0.64% to 7,738 points at the time of writing.

The ASX All Ords may be wobbling after the release of official notes from the US Federal Reserve’s latest meeting. The notes indicated that bigger interest rate hikes than usual — possibly 0.5% at a time — might be required to curb inflation once the Ukraine-Russia conflict eases, according to reporting by abc.net.au.

Among the drags on the All Ords index today are these three ASX small-cap shares, which have all touched new 52-week low prices.

The first ASX All Ords faller we’re looking at today is fashion footwear retailer Accent. It’s trading down 5.35% to $1.56 at the time of writing — its lowest level in a year. This is a long way down from the 52-week high of $3.08 reached in April 2021.

Next is online luxury goods retailer Cettire, which is currently down 7.42% at $1.06 — a new 52-week low. This ASX All Ords share is now down 78% on its 52-week high of $4.81 reached in mid-November. That was around the time the company announced a direct brand partnership with Staff International and reported strong trading momentum.

Lastly, we look at Audinate, which crashed to a new 52-week low of $6.13 in earlier trading. That’s a 4% decline on yesterday’s closing price of $6.39. It has since rebounded to its current price of $6.22 at the time of writing.

The last lot of price-sensitive news from Audinate came on 14 February when it released its 1H22 results. The audio-visual networking provider delivered strong revenue growth and said it was navigating supply chain issues well. Broker James Gerrish of Shaw and Partners responded the following day by slapping a $12 price target on this ASX All Ords small-cap. He’s still keen on the stock today, as my Fool colleague Tony reported.

ASX All Ords recap

The All Ordinaries index is down 2.4% year to date but up 7.8% over the past 12 months.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the five best ASX stocks for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now.

Motley Fool contributor Bronwyn Allen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. owns and has recommended AUDINATEGL FPO and Cettire Limited. The Motley Fool Australia owns and has recommended AUDINATEGL FPO. The Motley Fool Australia has recommended Accent Group and Cettire Limited. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/HtvmqXO

The Xero Limited (ASX: XRO) share price has dropped 5% over the last two days.

Considering the market capitalisation of Xero is $15.7 billion (according to the ASX), this decline represents hundreds of millions of dollars.

Xero shares are seeing red, just like plenty of other ASX shares on the stock market. At the time of writing, the S&P/ASX 200 Index(ASX: XJO) is down by 0.6%.

Today, the WiseTech Global Ltd (ASX: WTC) share price is down 5.4%, the Novonix Ltd(ASX: NVX) share price is down 5.2%, the Block Inc (ASX: SQ2) share price is down 4.1%, the Webjet Limited (ASX: WEB) share price is down 3.9% and the Pro Medicus Limited (ASX: PME) share price is down 3.1%.

There haven’t been any announcements out of the company recently that could have affected the Xero share price. However, it is due to hand in its FY22 full-year result on 12 May 2022.

What is causing the ASX share market to be volatile?

Inflation and interest rates are getting much more investor attention these days.

A number of Australian economists now believe that June could be the month when interest rates start increasing in Australia, according to the Australian Financial Review.

Why do interest rates matter for the Xero share price? Or any asset price?

Billionaire Ray Dalio, founder of Bridgewater Associates, once said about interest rates and asset valuations:

It all comes down to interest rates. As an investor, all you’re doing is putting up a lump sum payment for a future cash flow.

Before you consider Xero , you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Xero wasn’t one of them.

The online investing service he’s run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. owns and has recommended Block, Inc., Pro Medicus Ltd., WiseTech Global, and Xero. The Motley Fool Australia owns and has recommended Block, Inc., Pro Medicus Ltd., WiseTech Global, and Xero. The Motley Fool Australia has recommended Webjet Ltd. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/LnZ75vY

Should you invest $1,000 in AVZ Minerals right now?

Before you consider AVZ Minerals, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and AVZ Minerals wasn’t one of them.

The online investing service he’s run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor Aaron Teboneras has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/KgXq7Rk

The ASX could be about to welcome a mining technology company amid a major commodities boom.

Chrysos Corporation might be gearing up to list on the market by May. The details of its IPO are expected to be finalised today, according to The Australian.

The company could be floating with a valuation of around $600 million following an initial public offering (IPO) worth approximately $200 million.

Let’s take a closer look at the CSIRO-born-and-backed company and its apparently imminent ASX float.

Could this ASX hopeful win out in the commodities boom?

Chrysos Corporation is seemingly gearing up to join its ASX mining clients on the exchange, potentially making the most of the current commodities boom.

According to the CSIRO’s Resourceful magazine, the company is “part spin-out, part employee start-up, part investor joint venture”. The scientific research agency still holds a significant portion of the company.

Chrysos Corporation’s mining technology – PhotonAssay – has been developed by the CSIRO over the last 15 years and commercialised by the company for the last five years.

It’s said to be a faster, safer, more accurate, and more environmentally friendly way to analyse gold samples. It could replace the industry standard, fire assay, which employs extreme heat and chemicals.

Chrysos Corporation makes its coin by leasing its equipment, and licensing its technology, to mining companies.

But what kind of cash could the commodities-focused ASX IPO hopeful be bringing in?

Those metrics are reportedly expected to increase to $26.6 million and $3.2 million respectively next financial year. And, in following years, they could double.

The CSIRO isn’t the only entity with a hold of Chrysos Corporation. Perenti Global Ltd(ASX: PRN) also owns shares in the ASX hopeful.

The Australianhas also recently reported Regal Funds Management, Wilson Asset Management, and Tribeca Investment Partners each own stakes in Chrysos Corporation.

No doubt, all eyes will be on the mining tech company ahead of its potential IPO and ASX float.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the five best ASX stocks for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now.

Motley Fool contributor Brooke Cooper has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/9Cy7whn

In afternoon trade, the S&P/ASX 200 Index (ASX: XJO) has followed the lead of Wall Street and is tumbling lower. At the time of writing, the benchmark index is down 0.7% to 7,438.1 points.

Four ASX shares that are falling more than most today are listed below. Here’s why they are dropping:

The Andromeda Metals share price has continued to sink and is down a further 15% to 9.8 cents. Investors have been selling this kaolin explorer’s shares this week following the release of a bitterly disappointing definitive feasibility study (DFS) for the Great White Kaolin Project in South Australia. Management revealed an internal rate of return (IRR) of 36% and a 5.9 years payback, which compares unfavourably to previous estimates of 175% and 15 months, respectively.

The ARB share price is down 5% to $39.39. Part of this decline is attributable to the 4×4 parts manufacturer’s shares trading ex-dividend this morning for its interim dividend. Eligible shareholders can now look forward to receiving this fully franked 39 cents per share dividend later this month on 22 April.

The BCI Minerals share price is down 7% to 44.2 cents. This follows the release of an update on its Mardie project this morning. Comments around costs appear to have spooked investors. Management commented: “Cost pressures are evident across the mining and construction sectors in Western Australia. We are closely monitoring and managing our contracts and are reviewing the inflationary impact on the total Mardie capital cost.”

The WiseTech share price is down 6% to $49.59. This appears to have been driven by weakness in the tech sector today following another very poor night of trade on the Nasdaq index on Wall Street. It isn’t just WiseTech that is tumbling today. At the time of writing, the S&P ASX All Technology index is down 3.1%.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the five best ASX stocks for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now.

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. owns and has recommended WiseTech Global. The Motley Fool Australia owns and has recommended WiseTech Global. The Motley Fool Australia has recommended ARB Corporation Limited. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/UgBDxPG

It might be a red day for the S&P/ASX 200 Index (ASX: XJO) on Thursday, but that hasn’t stopped a handful of shares from reaching 52-week highs today.

In afternoon trade, the Aussie benchmark index is 0.5% worse for wear, treading around 7,450 points. Yet, a select few ASX 200 constituents are being embraced amongst the sour session.

Following on from hitting a new all-time high yesterday, the Dan Murphy’s and BWS owner is setting new records again today. Shares in Endeavour Group have lifted more than 1% during trade to reach $7.66.

However, there’s not a whole lot of new information out from the company today. Insinuating the company’s shares might still be revelling in an improved outlook from Goldman Sachs. The broker set its price target for Endeavour Group at $8 per share.

The next ASX 200 share leaving the market green with envy is coal producer New Hope Corporation. Shares are making the trek upwards today despite there not being any announcements from the $3.1 billion energy giant. At the time of writing, the New Hope share price is up 2.2% to $3.79 — with an intraday high of $3.80.

For reference, this stampede into positive territory has continued after non-exec director and non-exec chair Thomas Millner and Robert Millner acquired more shares. According to the filings, the two board members added more than $1.68 million worth of New Hope shares across 4 April and 5 April.

Finally, Worley is another new 52-week high candidate today. Although, the engineering services company has slipped into the negative as the day has gone on. Regardless, Worley shares climbed to $13.89 shortly after the market opened. Now that price is closer to $13.50 as we head into the afternoon.

This ASX 200 share is another name hitting the new high milestone without much substance today. Despite Worley shares charging 10% higher in the last month, the company hasn’t released a price-sensitive announcement since 23 February, which was its half-year results.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the five best ASX stocks for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now.

Motley Fool contributor Mitchell Lawler has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/OgjWi1u

Perhaps more than any other sector, ASX energy shares had a wild ride over the quarter just gone. During the three months to 31 March, global energy prices went on a rollercoaster, largely as a consequence of the disruptions caused by the war in Ukraine and subsequent sanctions levied on the Russian economy.

As a result, the world has seen record-high oil, gas, and coal prices which, of course, have flowed through to the bowser, the supermarket, and almost every corner of the economy. But how did the companies that drill, pump, and mine oil, gas, and coal out of the ground fare during these tumultuous times?

Well, let’s first check out the ASX’s largest energy share, Woodside Petroleum Limited(ASX: WPL),

Woodside started 2022 at $21.93 a share. On 31 March, this energy giant finished up at $32.10. That’s a rather stunning rise of 46.37% for the March quarter. This arguably proves how valuable soaring energy prices can be for an ASX energy share.

ASX energy shares shoot the moon over March quarter

But did other energy shares experience similar moves? Beach Energy Ltd(ASX: BPT) is another company in this space worth checking out. Beach shares were priced at $1.26 each on New Year’s Eve. Fast forward to 31 March, and we saw the company shoot up to $1.56. That’s a far less enthusiastic, but still solid, rise of 23.81%.

Santos Ltd(ASX: ATO) is another ASX energy heavyweight. It was going for $6.31 a share at the start of the quarter ending 31 March. But by the end, we saw this company reach $7.74 — a gain of 22.66%.

Turning to an ASX coal miner, let’s examine how Whitehaven Coal Ltd(ASX: WHC) shares performed over the same period. Whitehaven ended 2021 at a share price of $2.61. But three months later, the company had reached $4.15 a share. That’s a whopping gain of 59% in three months.

So, all in all, it has been a very lucrative quarter for ASX energy shares. Whitehaven was the clear winner, followed by Woodside, with both companies clocking gains of more than 45%. But all of these companies managed to appreciate by more than 20% over the first quarter of 2022. No doubt ASX energy investors will be hoping for a repeat performance during the current quarter ending 30 June. But we shall have to wait and see.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the five best ASX stocks for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now.

Motley Fool contributor Sebastian Bowen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/cNon2W3

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

It’s easy to look at a stock like Amazon (NASDAQ: AMZN) and think that at $1.7 trillion, it can’t possibly go much higher in value than where it is today. But as long as a company has ways to continue growing, there’s no reason its valuation won’t also increase. And there’s no danger for this cash-rich business to run out of opportunities anytime soon.

In just three charts, investors can see why, despite its massive size, Amazon can still be an excellent long-term investment.

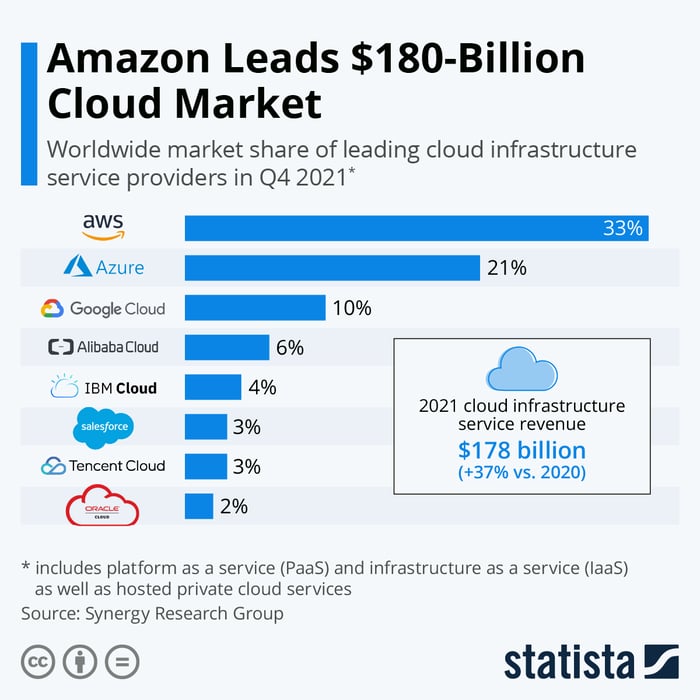

A leader in the cloud market

Although Amazon is primarily known for being a top online retailer, its cloud business, Amazon Web Services (AWS), has also made a name for itself in the industry. Many top companies use AWS, including software company Intuit, top bank HSBC, and COVID-19 vaccine maker Moderna. And as a leader in the cloud market, it’ll undoubtedly continue to be a top choice for many businesses that expand their presence online.

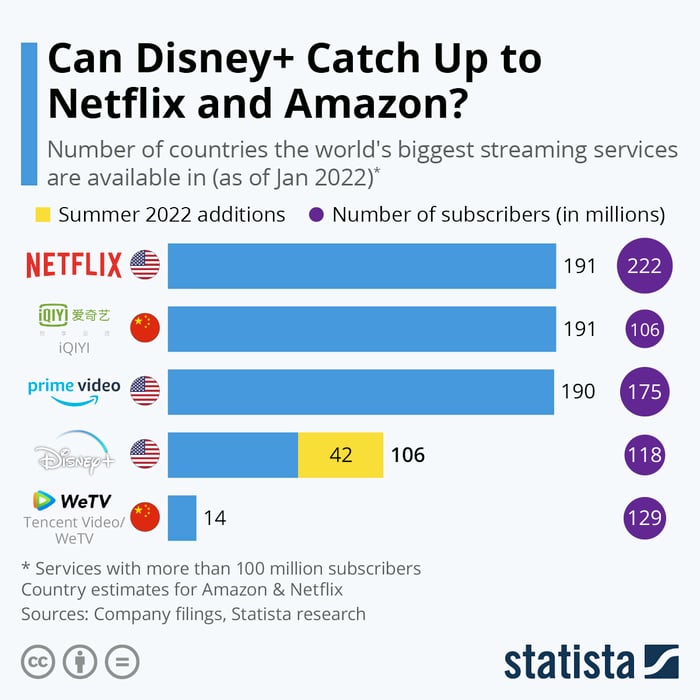

Its streaming service is among the top in the industry

Amazon Prime Video has over 175 million subscribers and is among the top streaming services in the world. An important caveat here is that Amazon Prime Video is included within an Amazon Prime subscription, and so these numbers likely would be lower if the company were only offering it as a stand-alone service the way Netflix and WaltDisney do their services. But it’s another example of how Amazon has room to grow in another area — streaming.

Last year, the company secured a deal with the NFL where it would spend a reported $1 billion per year for exclusive rights for Thursday Night Football games. It’s a 10-year deal that starts next year and will help diversify its streaming services; Netflix, for comparison, does not have any live sports available for subscribers to watch. Amazon can spend a lot more money to expand into its streaming business to make it more robust and possibly lure subscribers away from other services.

Amazon has been investing in various industries

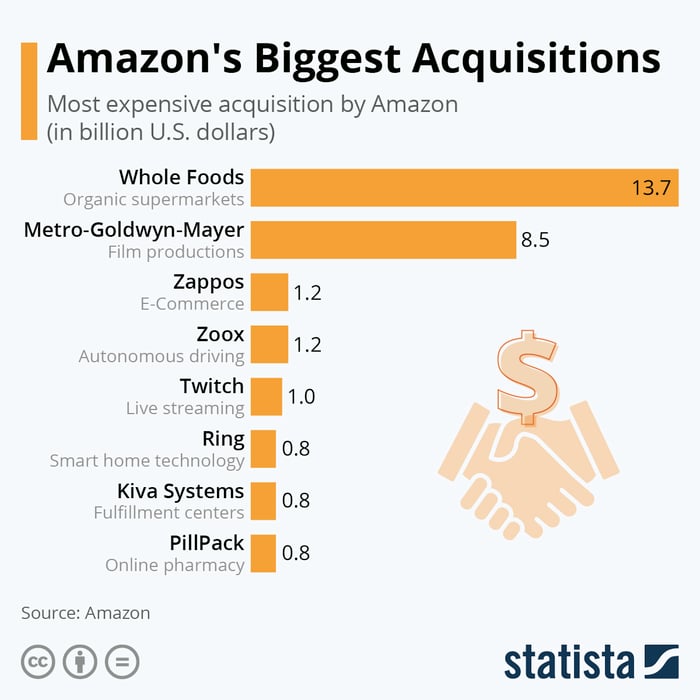

In 2021, Amazon generated $46 billion in cash from its day-to-day operating activities. The year before that, its cash from operations was north of $66 billion. The company is bringing in truckloads of cash every year and that puts it in an excellent position to spend on acquisitions to expand its business even further. Here are the biggest deals the company has made in recent years:

From autonomous driving to supermarkets to an online pharmacy, Amazon has been expanding its reach into various sectors. It can grow deeper into any one of these sectors or it can pursue yet another new one altogether. Either way, given the cash that Amazon generates each year, it won’t struggle to find a new growth avenue to pursue.

Should you invest in Amazon today?

Amazon just continues to get bigger over the years. In 2021, revenue of $469.8 billion was more than 67% higher than the $280.5 billion that the company reported in 2019, before the pandemic emerged. Online shopping is more popular than ever before and even if that slows down in a return to normal, the company can simply shift to other areas of its business, such as pumping more money into Whole Foods or developing its telehealth capabilities.

For buy-and-hold investors, Amazon is one of the safer growth stocks to hang on to over the long term. The business is a beast when it comes to cash flow, and with so many opportunities for growth, this is an unstoppable company to invest in. Up just 6% in the past year, while the S&P 500 has climbed 14%, the stock has underperformed the markets of late — but that isn’t a trend investors should expect to continue. It may only be a matter of time before this growth stock starts rallying again, and now may be as good a time as any to load up on it.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

Before you consider Amazon , you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Amazon wasn’t one of them.

The online investing service he’s run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

David Jagielski has no position in any of the stocks mentioned. John Mackey, CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. owns and has recommended Amazon, Netflix, and Walt Disney. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended HSBC Holdings, Intuit, and Moderna Inc. and has recommended the following options: long January 2024 $145 calls on Walt Disney and short January 2024 $155 calls on Walt Disney. The Motley Fool Australia has recommended Amazon, Netflix, and Walt Disney. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

from The Motley Fool Australia https://ift.tt/nKwYROt