ANZ Group Holdings Ltd (ASX: ANZ) shares are traditionally a very popular option for passive income investors.

And it isn’t hard to see why.

Each year, the banking giant shares a sizeable portion of its profits with its shareholders.

This usually means that its shares offer a dividend yield that is well ahead of average on any given year.

But will this remain the case in the future? Let’s find out what sort of passive income a $10,000 investment could generate from ANZ shares.

Passive income from ANZ shares

Firstly, let’s see how many shares you can buy with a $10,000 investment.

With the ANZ share price ending the week at $27.26, investors will end up owning 367 units if they put this amount into the bank’s shares.

Moving onto income, according to a note out of Goldman Sachs, its analysts are expecting the ANZ dividend to come in at a fully franked $1.62 per share in FY 2024.

This means that you would end up with income of $594.54 for the year.

And if you keep holding on the bank’s shares into 2025, you can expect another juicy pay check to come your way.

Goldman is expecting another fully franked $1.62 per share dividend in FY 2025. This will mean another $594.54 passive income boost for the year.

And then for a third year in a row, the broker expects ANZ to pay out $1.62 per share in dividends in FY 2026.

All in all, if Goldman is accurate with its forecasts, this will mean income of almost $1,800 for investors across the next three years from a $10,000 investment.

The broker currently has a buy rating and $27.85 price target on ANZ’s shares.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/uJ21kKW

Next week the Reserve Bank of Australia (RBA) will be meeting for the first time in 2024 to decide on interest rates.

This meeting comes at a very interesting time given how last week the Australian Bureau of Statistics revealed that inflation continued to ease during the December quarter.

In light of this, the market is now expecting the RBA’s next move for rates will be lower and not higher. This is very welcome news for borrowers.

But what could happen at next week’s meeting? Let’s take a look at what the economics team at Westpac Banking Corp (ASX: WBC) is expecting from the central bank.

Westpac on the RBA and interest rates

According to the bank’s latest weekly economic report, its team expect the RBA to keep its powder dry on Tuesday. Chief Economist, Luci Ellis, said:

The data flow since November has pointed in this direction, and today’s CPI release seals the deal: the RBA will keep the cash rate on hold next week, and it is unlikely to raise rates further this cycle.

And while Ellis has suggested that the central bank’s rhetoric at Tuesday’s meeting may not change as much as borrowers would like, she believes that it may not be long until the RBA will be confident enough to state that inflation is under control. She said:

[The RBA] is unlikely to rule out further rate increases entirely in their post-meeting communication. But the case to raise rate from here is steadily losing traction. We expect that over coming months, further declines in inflation and soft outcomes in the real economy will give the Board enough confidence that inflation will return to target on the desired timetable. They will therefore have scope to reduce some of the current restrictiveness of policy.

When will rates fall?

Westpac isn’t expecting interest rates to fall in the very near future, but does believe that the first cut will come in 2024.

Ellis advised that the Westpac economic team “expect the first rate cut no earlier than September.” This would take the cash rate to 4.1%.

The good news is that Westpac then expects further cuts to 3.85% by December, 3.6% by March 2025, 3.35% by June 2025, and then finally 3.1% by September 2025.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has positions in Westpac Banking Corporation. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/ajJR4mv

Building a diversified portfolio of ASX shares and exchange-traded funds (ETFs) is one of many different ways to invest in the Australian economy.

Given the choice, my preference right now would be to invest in Washington H. Soul Pattinson and Co. Ltd (ASX: SOL) shares. This appeals to me more than buying into an ETF such as the Vanguard Australian Shares Index ETF (ASX: VAS).

Now, the VAS ETF is not a bad investment. It has plenty of positives, including diversification, dividend yield and franking credits, and a low management fee. Investing in the Vanguard Australian Shares Index ETF can work well as a strategy for people wanting to take a more passive hand-off investment approach.

But I’d prefer to buy Soul Patts shares for a few different reasons.

Concentrated investments

I like that, as an investment house, Soul Patts has flexibility in its choice and allocation of investments, depending on the size of the opportunity.

Its biggest strategic positions include TPG Telecom Ltd (ASX: TPG), New Hope Corporation Ltd (ASX: NHC), Brickworks Limited (ASX: BKW), Pengana Capital Group Ltd (ASX: PCG), Apex Healthcare, Tuas Ltd (ASX: TUA) and Aeris Resources Ltd (ASX: AIS).

The VAS ETF is heavily invested in a small number of miners, banks and others, while its allocation to smaller businesses is very limited.

I like that Soul Patts has the freedom to allocate its capital wherever it likes. In its FY23 presentation, it described its investment style as “active and thoughtful” with an “unconstrained mandate”, and it did not invest to replicate any index.

I think concentrated investments in the right areas can lead to portfolio outperformance for Soul Patts shares.

Defensive setup

Soul Patts invests heavily in a number of industries that can provide defensive and resilient cash flows.

Banking and retailers, which make up a sizeable portion of the S&P/ASX 300 Index (ASX: XKO), are not defensive in my mind if a recession comes along. Miners are not exactly resilient in all conditions, but they can provide returns that are largely uncorrelated to the rest of the market.

Soul Patts invests in fairly defensive/uncorrelated areas like telecommunications, resources, swimming schools, property, healthcare, agriculture and more.

Strong dividend income

The VAS ETF typically offers a good dividend yield, but the distributions are not consistent. That’s mostly because an ETF passes through the investment income it receives, and dividends from the underlying holdings can change year to year â just think about how the BHP Group Ltd (ASX: BHP) dividend has bounced around.

Soul Pattinson has grown its dividend every year since 2000. While its starting dividend yield isn’t as high as the VAS ETF, the dividend is consistently growing. Having said that, growth is not guaranteed.

Soul Patts shares have outperformed

Past performance is not a guarantee of future returns, but Soul Patts’ portfolio has done well at beating the market over time.

At July 2023, the end date of its FY23 result, it said its total shareholder return (TSR) was 11.3% per annum over five years, 12.4% per annum over 10 years and 12.5% over 20 years, beating the All Ordinaries Accumulation Index (ASX: XAOA) return by 3.6%, 3.9% and 3.5% per annum, respectively.

I think Soul Patts’ investment choices now and in the future can enable it to deliver outperformance over the next decade. For example, in recent times, it has ramped up its investments in credit, unlocking equity-like returns.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tristan Harrison has positions in Brickworks and Washington H. Soul Pattinson and Company Limited. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Brickworks and Washington H. Soul Pattinson and Company Limited. The Motley Fool Australia has positions in and has recommended Brickworks and Washington H. Soul Pattinson and Company Limited. The Motley Fool Australia has recommended Tpg Telecom. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/ZAKzqrn

When it comes to buying ASX dividend shares, some beginner investors are seduced by the lure of high payouts. But there’s much more to picking the right passive income stocks for your portfolio than just dividend yield.

Is the company retaining enough profit to reinvest for future growth? Are its dividends sustainable? Does the stock have a decent track record of growing its shareholder payouts? Is the yield rising sharply on the back of recent share price falls, and if so, why are investors selling? And so it goes on…

To help sort the income-stock treasure from the traps, we asked our Foolish writers which ASX dividend shares they think should be on your buy list right now. Here is what the team came up with:

7 best ASX dividend shares for February 2024 (smallest to largest)

Why our Foolish writers love these ASX passive income stocks

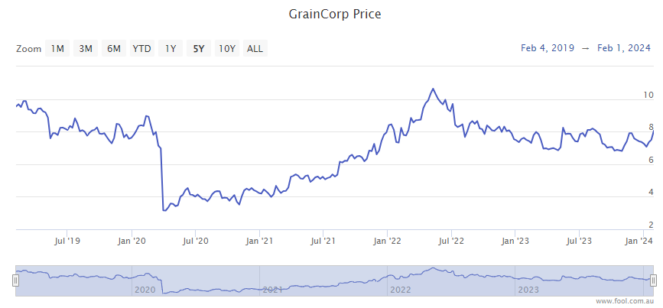

Graincorp Ltd

What it does: GrainCorp is a 100-year-old agribusiness and processing company that connects growers and producers with local and international customers. It manages a wide range of grains, pulses, oilseeds, biofuel components, animal feeds, and oils and shortenings used in food production.

By Bronwyn Allen: I used CommSec’s stock screener to identify the S&P/ASX 200 Index (ASX: XJO) stock with the best five-year growth rate for dividends. Up came Graincorp shares with an impressive 82.3% growth rate over five years and 22.1% over 10 years.

Among the nine analysts covering the stock on CommSec, five rate Graincorp a strong buy, three a hold, and one a strong sell.

While the long-term dividend growth rate is great, ag stocks can be volatile. The consensus expectation for Graincorp dividends in 2024 is 30.8 cents per share, well down on the 54 cents paid last year.

However, on today’s share price of $7.92, 30.8 cents still equates to a reasonable dividend yield of 3.9%, plus 100% franking.

Motley Fool contributor Bronwyn Allen does not own shares of Graincorp Ltd.

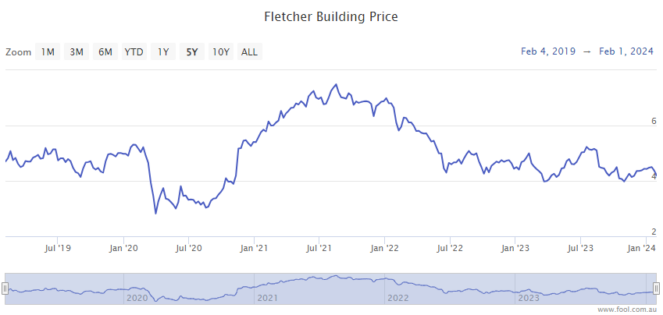

Fletcher Building Ltd

What it does: Fletcher Building is a New Zealand company that makes and distributes construction materials.Â

By Tony Yoo: This Kiwi outfit has been a consistent dividend payer over the past four years. The yield is already excellent at 7.4%, but if you include supplemental distributions, that is bumped up to 8.5%.

The cyclical nature of the construction industry is such that now might be a cheap time to buy a stock like Fletcher Building before the real estate market heats up from interest rate cuts. The current share price is around 19% off last August.

Pleasingly, revenue, operating margin and net profit before abnormals have all trended up over the past four financial years. According to CMC Invest, nine out of 11 analysts currently believe Fletcher Building shares are a buy.

Motley Fool contributor Tony Yoo does not own shares of Fletcher Building Ltd.

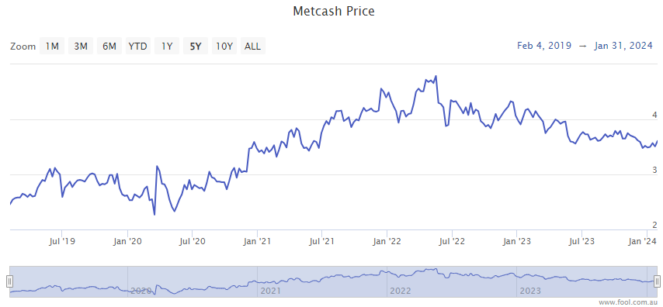

Metcash Limited

What it does: Metcash distributes food and drink to independent supermarkets and liquor stores around the country, including IGA supermarkets, IGA Liquor, Cellarbrations, The Bottle-O, Porters Liquor, Thirsty Camel, Big Bargain Bottleshop, and Duncans. It also has a hardware division that owns Mitre 10, Home Timber & Hardware, and Total Tools.

By Tristan Harrison: A number of ASX dividend shares have rallied in the last few weeks and months, reducing their dividend yields, but Metcash hasn’t seen that, making it look much better value relative to others.

Using Commsec forecasting, Metcash is projected to pay a very healthy grossed-up dividend yield of around 8%.

Furthermore, I think Metcash is one ASX stock that could strongly benefit from potential interest rate cuts, which could lead to stronger demand for its hardware division. Before economic conditions weakened, the hardware division was the most profitable, so a rebound in demand would be very helpful.

Population growth is also a useful tailwind for Metcash, with more people equating to more households and potential customers. The company recently announced it’s in the running to acquire Superior Food Group, which could further boost earnings.

In my opinion, the Metcash share price is good value. It’s priced at 13x FY24’s estimated earnings.

Motley Fool contributor Tristan Harrison owns shares of Metcash Limited.

Super Retail Group Ltd

What it does: Super Retail Group is a retailing conglomerate behind the popular Rebel, Super Cheap Auto, Macpac, and BCF chains.

By Sebastian Bowen: I’ve long been impressed with the performance of Super Retail Group. Sure, this company does operate in the usually-cyclical consumer discretionary sector. However, its stores — particularly Super Cheap and BCF — are famously recession-resistant.

Its recent numbers also suggest resistance to both high inflation and high interest rates, too. This alone makes it a good candidate for a dividend investor, in my view.

But what’s really caught my eye this February is Super Retail’s chunky dividend. At recent pricing, this company offers investors a yield close to 5%, which typically comes with full franking credits attached for an added bonus.

As such, I think you could do far worse than this company for a passive income investment today.

Motley Fool contributor Sebastian Bowen does not own shares of Super Retail Group Ltd.

NIB Holdings Limited

What it does: NIB is a private medical insurance provider to residents of Australia and New Zealand. After privatising in 2007, the company has grown to serve more than 1.5 million people. NIB also has a substantial presence in travel insurance and National Disability Insurance Scheme (NDIS) plan management.

By Mitchell Lawler: Jostling with heavyweights, such as Medibank Private Ltd (ASX: MPL) and Bupa, the smaller NIB has managed to grow at an above-industry rate for the last 20 years.

Dividends are dependent on profits. The business continues to report strong policyholder growth and attractive net margins. In particular, the international inbound health insurance segment posted a 15.7% policyholder increase in FY23, delivering a sensational net margin of 13.1%.

Furthermore, the core Australian resident offering continues to expand, increasing its policyholder count by 4.7% in FY23. As immigration into Australia surges, NIB could be well-positioned to reap the rewards.

Investors can secure NIB shares on a 3.6% dividend yield right now. It may not be quite as generous as other alternatives. However, I believe this company’s dividends have plenty of room to grow.

Motley Fool contributor Mitchell Lawler does not own shares of NIB Holdings Limited.

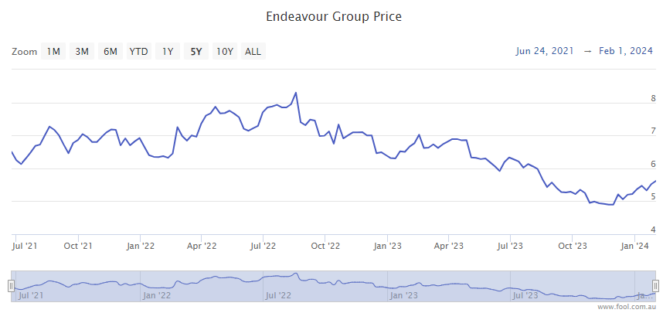

Endeavour Group Ltd

What it does: Endeavour is the drinks giant behind the BWS and Dan Murphy’s brands, as well as a large network of hotels/pubs.

By James Mickleboro: I think Endeavour would be a great ASX dividend share to buy due to its leadership position in a market that has defensive qualities.

In addition, the company still has plenty of growth opportunities. It added 39 retail stores to its network in FY 2023, bringing its network to 266 Dan Murphy stores and 1,435 BWS stores. While these may sound like large numbers, management isn’t stopping there, with plenty more store openings planned.

Goldman Sachs expects this to underpin the payments of fully-franked dividends per share of 21 cents in FY 2024, 23 cents in FY 2025, and 25 cents in FY 2026. This will mean yields of 3.8%, 4.2%, and 4.5%, respectively.

The broker also sees value in Endeavour shares at current levels. It has a buy rating and $6.40 price target on them. This represents more than 11% upside from Friday’s closing price of $5.74.

Motley Fool contributor James Mickleboro owns shares of Endeavour Group Ltd.

BHP Group Ltd

What it does: BHP is the largest company listed on the ASX. It has top-tier mining operations in Australia, North America, and South America. The diversified resources company earns most of its revenue from iron ore, with copper coming in at number two and coal also providing significant income.

By Bernd Struben: BHP is well known for its reliable, fully franked dividends. And BHP’s share price and dividends are closely aligned with the price of iron ore, which topped US$220 per tonne in mid-2021.

The retrace in the price of the industrial metal in the latter half of 2022 and much of 2023 to below US$100 per tonne also saw BHP’s dividends come down from the all-time highs of late 2021 and 2022.

Though at yesterday’s closing price of $47.61, BHP still trades at a healthy 5.5% trailing yield.

When it comes to the outlook for the iron ore price, I’m in agreement with Citi’s analysts. They see it rebounding to US$150 per tonne (up from the recent US$136 per tonne) in the first quarter of 2024. This would bode well for BHP’s share price and dividends.

Motley Fool contributor Bernd Struben does not own shares of BHP Group Ltd.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Citigroup is an advertising partner of The Ascent, a Motley Fool company. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has positions in and has recommended NIB Holdings and Super Retail Group. The Motley Fool Australia has recommended Metcash. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/zJfERox

It’s always the dilemma when you come across a hot stock that’s rocketed in recent times.

Has the share price already had all its wins? Or is the business outlook still strong enough to produce further gains for investors?

Those who are looking at Fortescue Ltd (ASX: FMG) are in exactly this predicament at the moment.

The share price for the iron ore and green energy miner has soared 41% just in the last three months. If you go back to a trough last May, the return is an amazing 54.5%.

“The company revealed that it shipped 48.7 million tonnes over the period. That brought its shipments for the six months to 31 December to 94.6 million tonnes, the second-highest half-year in Fortescue’s history.

“What’s more, the company was able to achieve average revenue of US$116 per tonne.”

From this point on, the iron ore outlook is even better.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Citigroup is an advertising partner of The Ascent, a Motley Fool company. Motley Fool contributor Tony Yoo has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/jGrxAqL

Sometimes complicated problems have very simple solutions.

Stock investment guru and buy-and-hold advocate Brian Feroldi recently cited the 2006 example of an American anesthesiologist who created a new tool to save lives.

“It was tested in 100 Michigan hospitals over 15 months,” Feroldi said in his newsletter.

“During that time, it saved 1,500 lives and reduced spending by $200 million.”

Amazingly, the tool only cost 2 cents per use.

“In the history of medicine, there may never again be a more powerful, accessible tool to help the masses.

“And what was that magic tool? It was a checklist.”

The list had five items to check off: washing hands, clearing the incision site, draping the patient, using surgical hat, gloves and gown, and applying sterile dressing.

And each piece of paper that these reminders were printed on cost just $0.02.

“Using the checklist cut infections from a 4% occurrence to zero.

“We’re enamoured with complicated, high-tech solutions. But more often than not, eliminating unforced errors is where the real gains can be had.”

The investment tool that could save your bacon

So what does this have to do with investing in ASX shares?

Feroldi insists that “returns can often be improved dramatically” by avoiding simple mistakes.

So he suggests going through this checklist just before hitting the “buy” button in your broking system:

Is the company’s gross margin stable or expanding?

Is the company self-funding, or is it reliant on outside capital?

“These three questions alone could eliminate 80% of the potential investments you spend your time researching,” said Feroldi.

“It’s up to you to spend the rest of that time getting familiar with the choices left.”

Of course, everyone has different priorities, tastes, and investing styles.

Feroldi pointed out his newsletter colleague Brian Stoffel has nine items on his checklist, while he has many more.

But ultimately, they all serve the same purpose: to narrow down stock ideas and reduce investing mistakes.

“Over the long-term, eliminating these ‘unforced errors’ — and focusing your time on the investments that are truly worthy — can make all the difference.

“If you don’t have an investing checklist, make 2024 the year you build one. Your future self [will] thank you.”

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tony Yoo has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/vx8E0OG

The S&P/ASX 200 Index(ASX: XJO) gained 1.71% over the week to finish at 7,699.4 points on Friday.

All market sectors finished the week in the green.

Let’s check out the week’s news.

Real estate shares led the ASX sectors this week

So, we know why this is happening, don’t we?

It’s all about interest rates, and mounting speculation that the Reserve Bank (RBA) will keep rates on hold. And not just at its first meeting of 2024 next week. In fact, maybe the rate hiking cycle is over.

CBA head economist Gareth Aird was definitive in his prediction for the RBA decision next week:

We expect the RBA will leave the cash rate unchanged next week and see no chance of any other outcome. We expect the RBA to lower their end-2024 inflation forecast to a little above 3%. And we anticipate they will forecast inflation returning to the mid-point of the target band by mid-2026.

CBA reckons the RBA will start cutting interest rates in September. Aird said his economics team expects total cuts of 75 basis points this year, and another 75 in 1H 2025.

Over in the United States this week, the Federal Reserve kept interest rates on hold for a fourth consecutive month at 5.25% to 5.5%.

Among the large-cap real estate stocks, Goodman Group (ASX: GMG) shares rose by 7.34% to finish at $26.98 per share this week. Scentre Group (ASX: SCG) shares rose to $3.10, up 5.98% over the week.

Stockland Corporation Ltd (ASX: SGP) shares gained 4.25% to finish at $4.54 on Friday. The Vicinity Centres (ASX: VCX) share price lifted 4.35% to $2.04, and Mirvac Group (ASX: MGR) shares rose 3.1% to $2.16.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bronwyn Allen has positions in Goodman Group. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goodman Group. The Motley Fool Australia has recommended Goodman Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/0FCepgo

It was a big week for many S&P/ASX 200 Index (ASX: XJO) shares.

A week that saw the benchmark index close at a record high of 7,680.70 points on Wednesday before resetting that with a record close of 7699.40 points on Friday. These both topped the previous all-time closing high of 7,628.9 points, notched on 13 August 2021.

With records toppling, here’s why these three ASX 200 shares grabbed the Motley Fool’s headlines this week.

Three ASX 200 shares grabbing the Motley Fool’s headlines

The first ASX 200 share that leapt into the Motley Fool’s headline news this week was Commonwealth Bank of Australia (ASX: CBA).

On Tuesday, CBA, Australia’s biggest bank stock, set its own all-time intraday high. In early morning trade shares in the big four bank were changing hands for $116.94 apiece. That put CBA shares up 22% since 31 October.

With no fresh price-sensitive news out from CBA, Motley Fool analyst Sebastian Bowen attributed the record high to the same factors that were sending the ASX 200 towards all-time highs on the day. Namely “falling inflation, strong economic growth with low unemployment, and the expectations of interest rate cuts this year”.

Also leaping into the Motley Fool’s headlines this week was mining giantBHP Group Ltd (ASX: BHP).

The ASX 200 share led the news on Monday after it was reported that BHP, Vale and their Samarco joint venture could be facing 47.6 billion reais (AU$14.8 billion) in legal damages. Those compensatory damages, tied into the 2015 Samarco Fundao dam collapse in Brazil, were levelled by a Brazilian federal court judge.

BHP responded that it was “fully committed to supporting the extensive ongoing remediation and compensation efforts in Brazil through the Fundacao Renova”.

However, as the miner had not yet been served with the court decision, management said they would review the implications and the potential for an appeal.

The BHP share price closed the day down 1.4%.

Which brings us to the third ASX 200 share that leapt into the Motley Fool’s headlines this week.

Paladin, and indeed numerous ASX uranium stocks, made headline news on Friday as uranium prices soared to near 16-year highs.

The uranium price has more than doubled over the past 12 months, with 22 nations recently having pledged to triple their nuclear power capacity to provide reliable baseload power without atmosphere-warming carbon emissions.

New uranium supply was already lagging behind the demand growth. And on Friday, Paladin received another big boost after Kazatomprom, the world’s top uranium producer, reiterated concerns that supply issues with sulphuric acid, crucial for its uranium mining methods, would impact its production levels in 2024.

The Paladin share price closed up 6.6% at $1.38 on Friday.

That sees the ASX 200 share up 39.5% so far in 2024.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/U6lxVzn

The ASX reports that $1.1 billion of IPO capital was raised among 45 IPO listings in 2023. The five-year average for ASX IPOs is $5.4 billion among 120 listings per year.

But the total quoted market capitalisation from all new market entrants in 2023 was higher than in 2022.

The total for IPOs, demergers, and new dual and direct listings was $33.7 billion, up 8% from the previous year.

In an article published on asx.com.au today, Alice Nguyen from ASX Listings said this was a global trend because growth companies faced strong economic headwinds last year.

But she said ASX IPO conditions may be better this year.

The biggest ASX IPO of 2023

Redox Pty Ltd(ASX: RDX) was the largest ASX IPO last year, raising $402 million and achieving a market cap of $1.3 billion at the time of listing in July.

Redox is a family-owned chemical and ingredient distributor. The owners sold a 30% stake with the aim of raising capital for offshore expansion.

The biggest new listings by value

The most significant listing by value was the dual-listing of US mining behemoth Newmont Corporation CDI (ASX: NEM). This follows Newmont’s acquisition of ASX gold mining stock Newcrest.

Another mega-merger was the $11 billion marriage and dual listing of Livent Corp and Allkem to form new ASX lithium share, Arcadium Lithium (ASX: LTM).

A big one on the way this year is the proposed merger of Sigma Healthcare Ltd (ASX: SIG) and the unlisted Chemist Warehouse.

The deal will create an $8.8 billion ASX healthcare major, once it is completed in 2H 2024 (assuming regulatory approvals).

Top 10 ASX listings in 2023… and their share prices today

This list represents the top 10 new listings by market cap, including ASX IPOs and major mergers.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bronwyn Allen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/C5WqZwB

DUG Technology Ltd (ASX: DUG) shares are catching the eye on Friday afternoon.

At the time of writing, the ASX All Ords tech share is up 9% to a new 52-week high of $2.34.

Why is this ASX All Ords share jumping?

Investors have been buying the analytical software development company’s shares after it released an announcement after lunch.

In case you’re not familiar with DUG Technology, it delivers innovative software products and cost-effective, cloud-based high-performance computing (HPC) as a service backed by tailored support for technology onboarding.

Its expertise in algorithm development and code optimisation allows its clients to leverage big data and solve complex problems. These clients come from a diverse range of industries including radio-astronomy, biomedicine, and meteorology, as well as the resource, government, and education sectors.

What was the announcement?

This afternoon the ASX All Ords share announced that it has deployed 600 new Intel Xeon CPU Max Series machines.

In addition, it is investing in 1,500 AMD EPYCTM Genoa machines costing US$18.2 million to support the growth of its Services business line. It notes that it has executed a letter of intent received from First National Capital to lease the compute.

The ASX All Ords share’s managing director, Dr Matthew Lamont, was very pleased with the news. He said:

It is very exciting to see our HPC capabilities grow in response to the increasing demand for our services. The Intel machines are already benefiting our active MP-FWI projects. The AMD machines are needed to accelerate delivery of both current and imminent projects, and to support the unprecedented demand we continue to see moving forward. These are exciting times indeed.

DUG Technology shares are now up 170% over the last 12 months.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has recommended Dug Technology. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/tqQYnCk