On Wednesday, the Australian Bureau of Statistics released the latest inflation data and revealed a lower than expected reading.

According to the release, consumer prices rose a modest 0.6% during the December quarter and 4.1% over the last 12 months.

In light of this, the market is now starting to believe that interest rates could start to fall in the near future.

This could be good news for Telstra Group Ltd (ASX: TLS) shares, which have struggled as interest rates climbed.

That’s because the telco giant is treated like bond proxy by many investors. So, when actual bonds offer yields that are equally as attractive as Telstra’s dividend yield, they will just buy the risk-free bonds instead.

But what might happen if interest rates fall? Will that make Telstra and other ASX telco shares more attractive?

Goldman Sachs thinks that will be the case. While it isn’t overly optimistic on interest rates falling materially any time soon, it does believe that Telstra could benefit when they do.

What is the broker saying about interest rates and Telstra shares?

The broker isn’t expecting interest rates to be cut aggressively but sees scope for a gradual adjustment. It said:

With our local and global economics teams forecasting rate cuts through 2024, alongside 2yr US rates having compressed significantly in recent months, clearly market expectations for interest rates will be both a significant driver of shareholder returns (and potentially earnings) for our TMT coverage through 2024. However we would stress that our global economists believe the market is discounting too much easing at this point, given they remain upbeat on the growth outlook – potentially suggesting a series of gradual adjustment cuts is more likely than an aggressive easing campaign.

This is likely to be good news for Telstra shareholders. It adds:

As recently noted by our strategists, when interest rates started to fall last year, they believed ‘Bond Proxies’ weren’t as expensive as they appeared on face value thanks to more conservative balance sheets and pay-out policies. Hence following their recent underperformance (vs. cyclicals) they see an even stronger case to add to defensive exposures – supporting our positive view on Telstra (Buy).

Goldman currently has a buy rating and $4.65 price target on Telstra’s shares. It is also forecasting fully franked dividends per share of 18 cents in FY 2024, 19 cents in FY 2025, and 20 cents in FY 2026.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has positions in and has recommended Telstra Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/pdlOUjz

The S&P/ASX 200 Index (ASX: XJO) started the year with a bang. The benchmark index rose a decent 1.2% in January to finish at a record high close of 7,680.7 points.

While this was a great return, it pales in comparison to some of the gains that were made last month.

For example, the five ASX 200 shares listed below absolutely smashed the market in January:

The Boss Energy share price was the best performer on the ASX 200 index last month with a stunning 38% gain. Investors were scrambling to buy the uranium developer’s shares after the price of the chemical element surged to new highs. This was driven by an update from the world’s largest uranium developer, which warned that it could fall short of guidance in the coming years. For the same reasons, Paladin Energy Ltd (ASX: PDN) shares raced 31% higher in January.

The Megaport share price was on fire last month and also stormed 38% higher. The majority of this gain came at the end of the month when the elasticity connectivity and network services interconnection provider released its quarterly update. Megaport reported total revenue of $48.6 million and EBITDA of $30 million. The latter was well ahead of expectations. Goldman Sachs commented: “MP1 reported 1H24 revenue of A$95mn (+35% yoy, +1% vs. GSe prior) and EBITDA of $30mn (+20% vs. GSe prior).”

The Alumina share price wasn’t too far behind with a gain of 29% in January. Investors were buying the alumina producer’s shares after it revealed that its partner, Alcoa (NYSE: AA), plans to fully curtail production at the loss-making Kwinana Alumina Refinery in Western Australia from the second quarter of 2024. This went down well with analysts. For example, Goldman Sachs responded by upgrading Alumina’s shares to a buy rating with a $1.43 price target. Alumina shares ended the month at $1.16.

The Elders share price was on form in January and rose a sizeable 19%. This appears to have been driven by favourable operating conditions. These conditions caught the eye of analysts at Bell Potter, which responded by retaining its buy rating with an improved price target of $9.50 (from $8.35). It said: “Since reporting FY23 results in Nov’23 soil moisture profiles in key summer cropping regions have improved and livestock prices have firmed, with volumes generally continuing to demonstrate high single-to-double digit YOY gains in both cattle and sheep/lamb markets.”

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Megaport. The Motley Fool Australia has recommended Elders and Megaport. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/NaWhtx5

ASX investors have enjoyed a pretty decent start to the new year. In fact, the S&P/ASX 200 Index (ASX: XJO) capped off the first month of 2024 with a record high.

And with the December-quarter inflation figures coming in cooler than expected, market chatter abounds on whether interest rate cuts might be on the horizon sooner rather than later.

This means that right now could be the ideal time for ASX shareholders to top up their portfolios and for beginner investors to take the leap and buy their first stocks.

To that end, we asked our Foolish writers which top ASX shares they reckon should be on your buy list this month. Here is what the team came up with:

7 best ASX shares for February 2024 (smallest to largest)

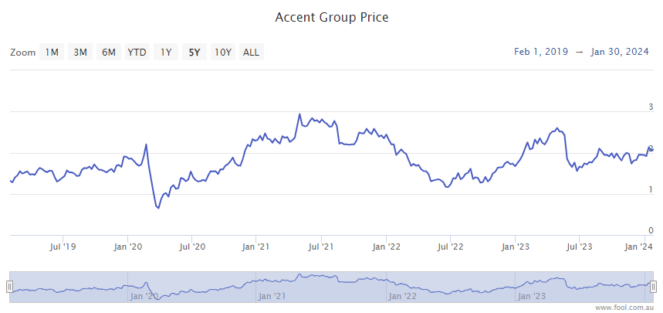

What it does:Â Accent distributes and sells shoe brands in Australia, such as CAT, Dr Martens, Henleys, Hoka, Kappa, Merrell, Skechers, Ugg and Vans. It also operates its own businesses, including The Athlete’s Foot, Trybe, Stylerunner, Nudy Lucy, and Glue Store.

By Tristan Harrison: Accent has done a good job of growing into the retail business it is today, with major global shoe brands electing to partner with it.

The Accent share price is still down around 20% from April 2023, giving investors an opportunity to invest in the company at a much lower valuation. Sales and profit may be challenged in 2024, but I think the long term looks promising, particularly if/when households start spending normally.

Accent is continually growing its store network and, interestingly, generates around a fifth of total sales from digital retail. I’m confident the company can keep adding brands to its portfolio and further grow its own businesses.

According to Commsec, the Accent share price is valued at less than 13x FY26’s estimated earnings with a possible grossed-up dividend yield of 10%.

Motley Fool contributor Tristan Harrison owns shares of Accent Group Ltd.

Elders Ltd

What it does: Formed 185 years ago, Elders has endured through a tumultuous slice of history. Today, the agribusiness has a hand in a wide array of segments, including agency services, real estate, agricultural chemicals, and animal health.

By Mitchell Lawler: The Elders’ share price deteriorated as much as 45% last year, at its low, as livestock prices normalised.

The steep upswing in cattle and sheep prices incentivised a rapid increase in supply. As usual, these reactions often overshoot, creating an oversupply â an issue exacerbated by demand pressure wielded by the cost of living. This manifested as a weak set of numbers from Elders in its FY2023 results.

However, wet weather has supported improving livestock prices despite the El Niño declaration. Given the confluence of stabilising prices and wetter conditions, there’s a reasonable chance â in my opinion â that Elders could return to growth this year.

Motley Fool contributor Mitchell Lawler owns shares of Elders Ltd.

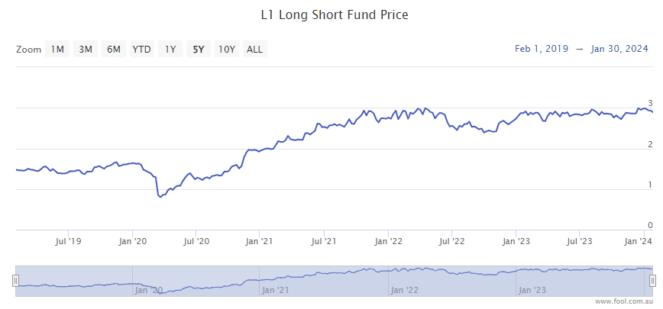

L1 Long Short Fund Ltd

What it does: The L1 Long Short Fund is a listed investment company (LIC) that manages a portfolio of ASX and international shares on behalf of its investors. As the name suggests, its management can use both ‘long’ investing and short selling to generate returns.

I’m always on the lookout for managed funds and LICs that can demonstrate a history of being able to beat the market over long periods of time. Long Short Fund falls into this category, and as such, it has piqued my interest. How could it not, with a five-year average return of 20% per annum (as of 31 December)?

With an established track record of performance, this LIC is at the top of my watchlist this month.

Long Short Fund has proven to have had an uncanny knack for picking winners. Some of its most successful investments in recent times have been the likes of Mineral Resources Limited (ASX: MIN) and BlueScope Steel Ltd (ASX: BSL).

This fund has the ability to short-sell shares as well, which could give investors some protection in the event of a downturn.

Motley Fool contributor Sebastian Bowen does not own shares of the L1 Long Short Fund Ltd.

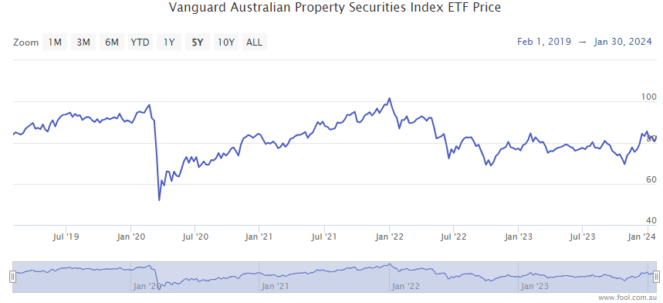

By Tony Yoo:Steep interest rate rises have been rough on the real estate sector over the past couple of years. That’s reflected in the Vanguard Australian Property Securities Index ETF share price, which is now down about 17% from the start of 2022.

However, with interest rates now reaching or nearing their peak, the property sector could be in for a revival. If the Reserve Bank of Australia actually cuts mortgage repayments, the party will be in full swing.

February could provide an excellent low entry point for long-term investment in Australian real estate through this ETF.

Motley Fool contributor Tony Yoo owns shares of the Vanguard Australian Property Securities Index ETF.

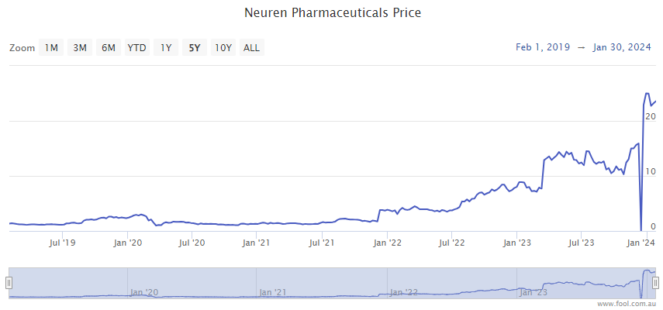

Neuren Pharmaceuticals Ltd

What it does: Neuren Pharmaceuticals is a biopharmaceutical developer specialising in drugs to treat neurodevelopmental disorders that emerge in childhood. In 2023, its first drug, Daybue, received FDA approval and went to market in the United States. It’s the world’s first treatment for Rett syndrome.

After such a strong performance, it’s interesting to note how many analysts are rating Neuren Pharmaceuticals shares a buy.

Clearly, they are unperturbed by the transformative change in the company’s market cap last year and see more share price growth ahead.

Of the five analysts covering Neuren shares on CommSec, four rate the stock a strong buy and one a moderate buy.

Could Neuren Pharmaceuticals stock be a winner yet again this year?

Motley Fool contributor Bronwyn Allen does not own shares of Neuren Pharmaceuticals Ltd.

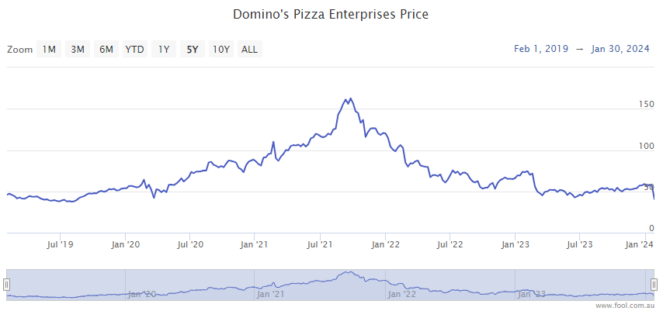

Domino’s Pizza Enterprises Ltd

What it does: Domino’s Pizza Enterprises is the exclusive master franchisor for the Domino’s brand network in countries including Australia, New Zealand, Belgium, France, The Netherlands, and Japan.Â

By James Mickleboro: I think it is fair to say that the last 12 months have been a complete disaster for Domino’s.

Management’s pricing missteps in response to inflationary pressures, and a poor performance from most of its operations during the first half, meant its shares lost almost half their value since this time last year.

While this is disappointing, I believe it has created a compelling buying opportunity for patient investors with a very favourable risk/reward.

Citi appears to believe this is the case. Its analysts currently have a buy rating and a $61.10 price target on Domino’s shares. This represents almost 52% upside from the company’s current share price of $40.21.

Motley Fool contributor James Mickleboro owns shares of Domino’s Pizza Enterprises Ltd.

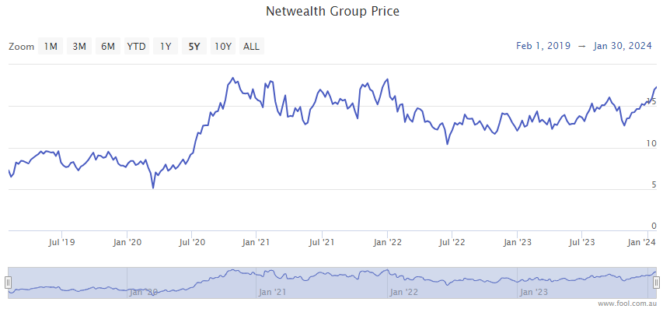

Netwealth Group Ltd

What it does: Netwealth is a diversified fintech company. Its platform provides portfolio administration, investment management tools, and investment and managed account services to financial advisers, private clients, and companies.

By Bernd Struben:The Netwealth share price is up 31% over the past 12 months, and I believe there’s more outperformance ahead.

The company recently reported that its member accounts grew by 3,254 in the December quarter to reach 132,826 accounts at the close of 2023.

As at 31 December, Netwealth had $78.0 billion of funds under administration (FUA). That was achieved following record 12-month FUA inflows of $19.7 billion.

Atop the potential capital gains, Netwealth shares trade on a 1.4% fully-franked trailing dividend yield.

And CommSec estimates that both the company’s earnings per share (EPS) and dividend payouts will increase over each of the next three calendar years.

Motley Fool contributor Bernd Struben does not own shares of Netwealth Group Ltd.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Domino’s Pizza Enterprises and Netwealth Group. The Motley Fool Australia has positions in and has recommended Netwealth Group. The Motley Fool Australia has recommended Accent Group, Domino’s Pizza Enterprises, and Elders. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/q1fB4t8

Invest wisely in ASX shares and summon up the patience to allow compounding to do its job, and you could find yourself smiling at the passive income coming into your bank account each month.

Take a look at this scenario as an example:

Compounding and ASX shares are your friends

Construct a diversified portfolio of ASX shares with that $10,000 and you’re on your way.

Just take a quick squiz at some of the quality stocks available on the S&P/ASX 200 Index (ASX: XJO).

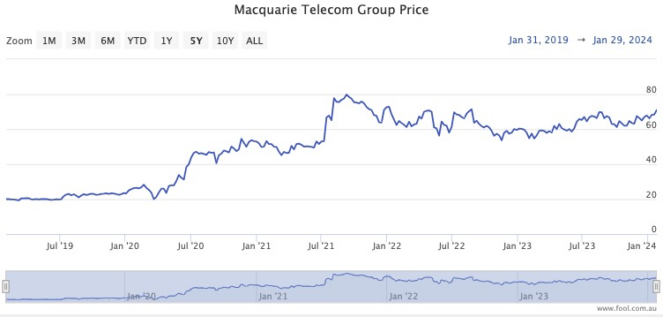

Data centre operator and telco Macquarie Technology Group Ltd (ASX: MAQ) has returned 265% over the past five years, for a CAGR in excess of 29%.

Over in dividend land, investment bank Macquarie Group Ltd (ASX: MQG) has risen 62% over the same period with a current dividend yield of 3.75%. Combining those equates to a 13.9% CAGR.

For a bit of both, how about retailer Lovisa Holdings Ltd (ASX: LOV), which has put on 243% of capital growth in five years while paying out a 3% yield? That takes the CAGR up over the 30% mark.

How to grab that sweet passive income

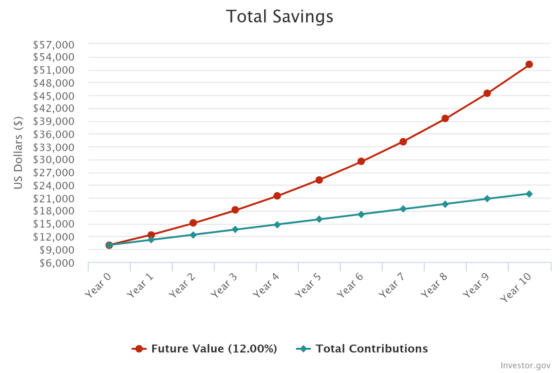

So send that $10,000 on its way then promise yourself to save $100 each month to add to this nest egg.

After 10 years, that portfolio could have reached $52,116.

From that point on, if you cash out the 12% annual return, that’s $6,253 each year.

That’s a passive income of $520 per month.

Mission accomplished.

Of course, there are levers you can pull if you want more passive income.

You can leave the investment growing for longer than 10 years. If you resist cashing out for five more years, that portfolio will be near enough to $100,000.

That will provide you passive income just short of $1,000 each month.

Another way is to increase your contributions each month.

If you can manage to add $200 instead of $100 every time the calendar turns, after 10 years the portfolio will be more than $73,000.

From then you can bring in monthly passive income of around $730.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tony Yoo has positions in Lovisa and Macquarie Group. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Lovisa and Macquarie Group. The Motley Fool Australia has positions in and has recommended Macquarie Group. The Motley Fool Australia has recommended Lovisa. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/gmdc0bV

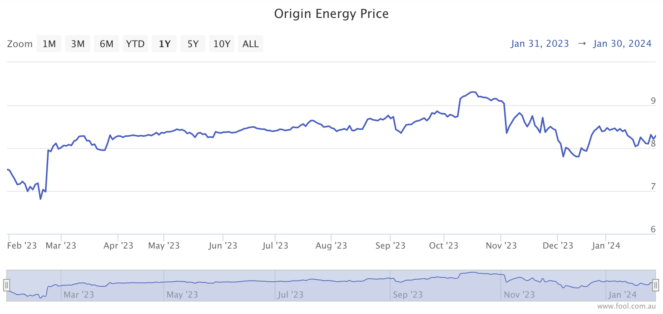

The Origin Energy Ltd (ASX: ORG) share price charged full steam ahead on Wednesday following the company’s December quarterly report.

As Australia Securities Exchange (ASX) trading closed for the day, shares in the $14 billion utility giant were up 2.7% from their previous closing price, settling at $8.52 apiece. The decent gain put Origin’s performance above that of other utility companies included in the S&P/ASX 200 Index (ASX: XJO).

Let’s take a closer look at what sparked the rally today.

Origin share price lifts on a mixed quarter

The headline numbers for all investors to know from today’s release include:

APLNG production up 1% to 167.4 petajoules (PJ) versus the prior corresponding period

APLNG gas sales down 1% to 160.4 PJ versus the prior corresponding period

Commodity revenue down 25% to $2.38 billion

Electricity sales up 6% to 9.0 terawatt hours (TWh)

Natural gas sales down 5% to 46.2 PJ

Based on the numbers, the December quarter appeared favourable for electricity and weaker for gas.

According to the report, lower gas production was experienced quarter-on-quarter due to an unplanned power outage on an LNG vessel. The interruption at Origin’s Curtis Island facility left the company incapable of loading three LNG carriers.

Adding to the pain, the average realised LNG price plunged 25% to US$11.88 per million British thermal units (MMBtu). However, the price was a 2% improvement from the September quarter figure.

The weakness in gas resulted in a reduction of Origin’s cash share from Australia Pacific LNG for the six months ended 31 December 2023. Falling 17% from its previous financial year-to-date amount, Origin received $648 million from the gas business.

Conversely, electricity sales increased 6% — as shown above — due to warmer weather and more customers.

What did management say?

Origin Energy CEO Frank Calabria shined a light on the company’s continued push into renewables during the quarter, stating:

We achieved further progress on our strategy to grow renewables and storage in our portfolio with the approval of a $400 million investment to construct a large-scale battery at Mortlake Power Station.

We also made a further investment in Octopus Energy to lift our interest as the company continues to grow rapidly and expand the global licensing of its Kraken platform.

On 18 December 2023, Origin upped its stake in Octopus Energy from 3% to 23%. The increased holding in the UK technology and energy company required $530 million.

Origin Energy share price snapshot

Even though the $20 billion takeover by Brookfield and EIG fell through late last year, Origin shares have held onto most of their accumulated gains.

As depicted below, the Origin share price is 15% higher than where it was seated 12 months earlier.

Still, shareholders may feel slighted by the fact Origin’s market capitalisation is a distance from the collapsed bid of $20 billion. The company is currently valued at $14.68 billion, which puts Origin 36% away from Brookfield’s offer.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Mitchell Lawler has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/uHafn6x

The S&P/ASX 200 Index (ASX: XJO) has certainly had a Wednesday to remember. Today saw the ASX 200 finally, after more than two years, hit a fresh new record high.

The index gained 1.06% by market close and finished the trading day at 7,680.7 points after touching its new record of 7,682.3 points just before close.

This hallowed day for ASX shares comes after another strong night up on Wall Street last night for US shares.

The Dow Jones Industrial Average Index (DJX: .DJI) hit another record high and banked a gain of 0.35%.

However, the Nasdaq Composite Index (NASDAQ: .IXIC) went the other way, shedding 0.76% of its value.

But let’s get back to the local markets now and see how today’s gains trickled down to the various ASX sectors.

Winners and losers

It was almost champagne all around on the markets today.

But there was one exception: ASX gold stocks. The All Ordinaries Gold Index (ASX: XGD) was left out in the cold during today’s session, losing 0.2% of its value.

But that was the only red sector on the markets.

Leading the gainers was the real estate investment trust (REIT) space. The S&P/ASX 200 A-REIT Index (ASX: XPJ) had a blowout this Wednesday, surging by 1.98%.

Hot on REITs’ heels were utilities shares. The S&P/ASX 200 Utilities Index (ASX: XUJ) rocketed by a pleasing 1.7%.

Also making waves were energy stocks. The S&P/ASX 200 Energy Index (ASX: XEJ) had a cracker too, shooting up by 1.56%.

Financial shares were only just behind, evidenced by the S&P/ASX 200 Financials Index (ASX: XFJ)’s swell of 1.47%.

Healthcare stocks were living up to their reputation too, with the S&P/ASX 200 Healthcare Index (ASX: XHJ) vaulting 1.22% higher.

Consumer staples shares didn’t miss out either, with the S&P/ASX 200 Consumer Staples Index (ASX: XSJ) gaining 1.02%.

Coming in at a dead heat with consumer staples shares were industrial stocks, with the S&P/ASX 200 Industrials Index (ASX: XNJ) also recording a rise of 1.02%.

Consumer discretionary stocks followed that, with a 0.6% lift for the S&P/ASX 200 Consumer Discretionary Index (ASX: XDJ).

Miners had a decent day as well, illustrated by the S&P/ASX 200 Materials Index (ASX: XMJ)’s upgrade of 0.46%.

Tech shares came next, with the S&P/ASX 200 Information Technology Index (ASX: XIJ) growing by 0.38%.

Communications stocks were our final bright spot. The S&P/ASX 200 Communication Services Index (ASX: XTJ) rose by 0.25% by the closing bell.

Top 10 ASX 200 shares countdown

Today’s top stock came down to nickel producer Nickel Industries Ltd (ASX: NIC).

Our top 10 shares countdown is a recurring end-of-day summary to let you know which companies were making big moves on the day. Check in at Fool.com.au after the weekday market closes to see which stocks make the countdown.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Sebastian Bowen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has recommended HomeCo Daily Needs REIT and Treasury Wine Estates. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/642IzMk

This followed what was then a new multi-year low for the Lake Resources share price. As my colleague went into at the time, Lake has been suffering immensely from the recent collapse in lithium prices, which has rendered its major Kachi project potentially unprofitable.

The company could well have issues raising any additional capital to cover its cash problems. As such, my colleague concluded that “zero seems like it could be a real possibility down the line” for Lake Resources shares.

At the time of writing, the Lake Resources share price is sitting at 9.5 cents each. Today, the company has shed another 5.15% of its value and is now down 8% from where it was last week to 9.2 cents a share.

Its 12-month share price losses now stand at a depressing 88.8%.

Investors shun Lake Resources shares after quarterly update

Investors don’t seem to have reacted too well to Lake Resources’ latest quarterly update, which was released today during trading hours. It seems that investors have taken this report as even more bad news.

So for the quarter ending 31 December 2023, Lake reported that it lost $17.97 million through operating its activities. That left its cash balance at $31.3 million at the end of the quarter, down from $60.28 million at the end of the previous quarter.

The company also has $36.19 million of unused cash left in a finance facility, for a total available funding of $67.5 million. Lake Resources estimates that this is enough cash to fund another 2.48 quarters of operation.

However, Lake also highlighted that it was able to reduce expenditures by approximately 20% over the quarter in question. It is also expecting to be able to cut costs by a further 40% over the current quarter (ending 31 March 2024).

Even so, it’s clear from investors’ reaction today that they are not too keen on what Lake Resources had to say. It will be interesting to see where the company stands at the end of March.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Sebastian Bowen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/mCPgrTx

Qantas Airways Limited (ASX: QAN) shares have been through a fair bit of pain. In the past six months, the ASX travel share has dropped 15%. Over that time, the S&P/ASX 200 Index (ASX: XJO) has risen 3%, so Qantas has underperformed by close to 20%. Can we look to history as to how Qantas could surprise this ASX reporting season?

A lot of stocks have risen in the last few months, but Qantas shares have faced a number of negative headlines relating to tickets being sold that seemingly shouldn’t have been sold, a ruling that Qantas illegally fired workers and more.

But, despite all of the issues, it’s possible that Qantas’ result release could be more positive than investors are expecting.

Priced for weakness

It’s understandable that the Qantas share price has dropped in light of these issues. There are also other factors that could impact the ASX travel share, including its need to spend heavily on replacing a large number of its planes.

But, ultimately, Qantas shares look as though they’re priced really cheaply considering how much profit Qantas might generate in FY24.

I think it’s a good idea to keep in mind a quote from Benjamin Graham â thought of as the person who taught legendary investor Warren Buffett – about markets and share prices:

In the short run, the market is a voting machine but in the long run it is a weighing machine.

In other words, the popularity of a stock can send the price lower in the short term, but it’s the financial performance that will drive things in the longer term.

If Qantas generated the same statutory numbers in FY24, the Qantas share price would be valued at less than 6 times profit. I think that’s a very low price/earnings (P/E) ratio.

The airline’s chair revealed, very briefly, at the company’s annual general meeting (AGM) in early November that “travel demand continues to be strong”. While this doesn’t give us much of an insight, it implies good financial performance is continuing. The oil price is, for now at least, still in the US$70s per barrel, down from the US$80s in October and November.

Qantas said at the AGM it had increased its fare prices to offset some of this higher oil cost.

The profit estimate on Commsec and from broker UBS both suggest Qantas could generate roughly the same EPS in FY24 as FY23, and that profit could keep rising in the years ahead.

The market seemed to underestimate how much travel demand there would be in the second half of 2022, and history showed that was a mistake.

There’s a fair chance that the FY24 first half result, and FY24 overall, could surprise positively in terms of how strong profit generation continues to be.

I wouldn’t bet ‘the house’ on Qantas shares, but it may be one of the most unloved ASX 200 shares at the moment, which could end up meaning it’s a contrarian opportunity for the longer term.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/bPzYTQM

The Australian stock market is already off to a flying start in 2024 so far. Sure, we’re now at the tail end of January, and the S&P/ASX 200 Index (ASX: XJO) has ‘only’ appreciated by around 0.2%.

But when you consider that we’ve just seen a new record high for ASX 200 shares minted, it’s not too bad. Especially so if we take into account that the ASX 200 Index has risen more than 12% since the start of November.

But even though we’re one month down in 2023 so far, there are 11 to go. So let’s go through three big questions that you might have about the ASX 200 in 2024

Will the Australian stock market hit more record highs this year?

First up, let’s talk about the new all-time record high that the ASX 200 hit just today. Today’s high of 7,658.7 points is a welcome development for all ASX 200 investors, who have had to wait more than two years to see a fresh record following the index’s last record in August 2021.

But now that this goal has finally been achieved, many investors will start wondering just how many new highs we might see this year. Can the ASX 200 hit 7,700 points? Maybe 7,900, or even 8,000 points?

Only time will tell. But if interest rates do start dropping in 2024 (as investors now clearly expect them to) without triggering an economic downturn, it could well push the ASX 200 to fresh heights.

Will interest rates start falling?

On that note, let’s talk about interest rates. As we touched on this morning, the legendary investor Warren Buffett once described interest rates as ‘financial gravity’, pulling everything else down to earth.

There’s little doubt that the pullbacks we saw from August 2021’s all-time high for the Australian stock market were caused by the massive runup of interest rates over the succeeding 18 months or so.

But could the reverse happen in 2024? Well, if the RBA does decide that inflation is now firmly back under control (which, after today’s numbers, seems more likely than ever), we could indeed see rates begin to drop again.

Investors have probably already baked in at least one cut this year for the Australian stock market, judging by today’s euphoric highs. But if inflation continues to drop faster than expected, we could well see multiple cuts.

Of course, the opposite is also true. If inflation picks up again, we could be looking at a 2024 with no cuts, or perhaps even a hike.

What will the dividends be like from ASX 200 shares?

Let’s talk about ASX shares themselves now. One of the most anticipated areas that investors focus on in the share market is what kinds of dividends are coming their way.

Given the unique structure of the Australian stock market (and our franking system), dividends form a major component of long-term returns.

Looking at an exchange-traded fund (ETF) like the SPDR S&P/ASX 200 ETF (ASX: STW), we can see that over the past 22 years or so, investors have enjoyed more returns through dividends than through capital growth.

So it goes without saying that investors will be paying attention to what kinds of dividends are coming out of the ASX 200 in 2024.

In particular, I’ll be watching the big four banks like Commonwealth Bank of Australia (ASX: CBA) and National Australian Bank Ltd (ASX: NAB). As well as miners like BHP Group Ltd (ASX: BHP) and Fortescue Ltd (ASX: FMG).

Also worth keeping track of are Telstra Group Ltd (ASX: TLS), Woolworths Group Ltd (ASX: WOW), Woodside Energy Group Ltd (ASX: WDS), Wesfarmers Ltd (ASX: WES) and Coles Group Ltd (ASX: COL).

If the majority of these blue chip ASX 200 shares give investors a dividend pay rise, it could help push up the entire Australian stock market.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Sebastian Bowen has positions in National Australia Bank, Wesfarmers and Telstra Group. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Wesfarmers. The Motley Fool Australia has positions in and has recommended Coles Group, Telstra Group, and Wesfarmers. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/oM5zDn8

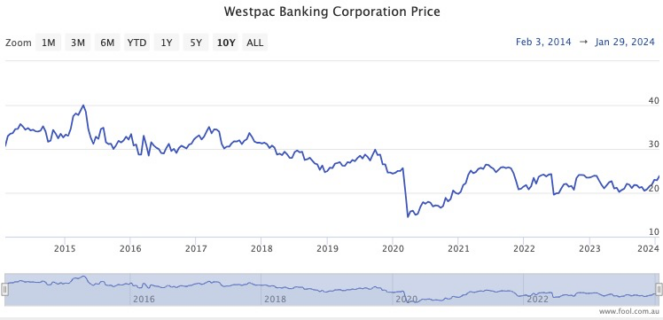

The Federal Court has ordered Westpac Banking Corp (ASX: WBC) to pay a total of $9.8 million for its actions relating to a $12 billion interest rate swap deal in 2016.

The Australian Securities and Investments Commission, which brought on the legal action after an investigation into the transaction, had told the court that the deal exposed Westpac’s client to serious risk.

The court ultimately agreed, calling Westpac’s actions as “unconscionable conduct” in its judgement.

Westpac will pay a penalty of $1.8 million, as well as $8 million for ASIC’s legal and investigation costs.

“Westpac’s behaviour was unconscionable and exposed its client to significant risk,” said ASIC deputy chair Sarah Court.

“Westpac’s conduct was also in stark contrast with several other banks.”

The fine was the largest legally possible for the time of the offence.

The same conduct now could attract a penalty that’s the larger of $782.5 million or three times the benefit derived.

Westpac made millions after pre-hedging without client consent

The detrimental conduct came when Westpac pre-hedged in advance of an interest rate swap transaction with a consortium acquiring electricity provider Ausgrid from the NSW government.

Despite concerns expressed by its client about how the pre-hedging could make the swap deal ultimately cost them more money, Westpac did it anyway without consent.

In doing so, the bank’s derivatives trading desk made a trading profit of about $20.7 million on the day the swap was executed. The sales team directly received $3.7 million of commission.

To this day, the $12 billion interest rate swap remains the largest transaction of its kind in Australian history.

“This is a significant outcome which assists to clarify expectations regarding pre-hedging, particularly around disclosure and consent,” said Court.

“Appropriate conduct for pre-hedging is an issue of global significance.”

The Federal Court found that Westpac had inadequate mechanisms to manage the conflict between its own interests and the consortium’s. The bank had not done enough to make sure the transaction was provided to the client “efficiently, honestly and fairly”.

A Westpac spokesperson told The Motley Fool that the bank had “already taken action to strengthen processes and policies in relation to pre-hedging activity”.

“Provision for the settlement was made in Westpac’s 2023 financial year results.”

The court reserved a decision as to whether Westpac will be ordered to complete a compliance program and an independent review into its pre-hedging practices.

The Westpac share price is down around 20% from January 2016.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tony Yoo has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Lh3o9Vl