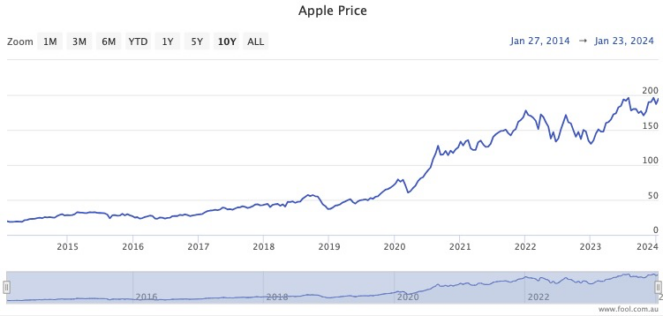

Despite already being a massive company in 2014, Apple Inc (NASDAQ: AAPL) shares have rocketed since then.

The computing giant has impressively come up with new innovations consistently to keep the demand for its products perpetually growing.

Ten years ago, the Apple share price was hovering around the US$18 mark.

If you had the foresight to buy US$20,000 of stock at that price, just 10 years later, it would now be worth US$216,866.

That’s better than a 10-bagger in the space of just a decade. A decade in which Apple spent a significant time as the largest company in the world.

Just amazing.

So is there an ASX growth stock that could emulate Apple?

Let’s check out Camplify Holdings Ltd (ASX: CHL).

Australia’s version of AirBnB?

Camplify is an online platform for owners of recreational vehicles to lend them out to strangers, generating cash when otherwise they would sit unused.

In simple terms it has been described as Airbnb Inc (NASDAQ: ABNB) for RVs.

The company listed on the ASX in June 2021 after an initial public offering (IPO) that saw shares sold at $1.42 each.

Camplify shares are now going for around $2.17.

Why does it have potential to be a multibagger in the coming years?

The business is growing rapidly.

Check out these numbers from the 2023 financial year compared to the year before:

- Revenue up 126%

- Net loss down 66%

- Cash flow per share improved from negative 13.1 cents to positive 4.8 cents

And professional investors are bullish on Camplify.

According to CMC Invest, both Canaccord Genuity and Morgans rate the ASX growth stock as a strong buy.

Can it become a 10-bagger over the next decade though?

Of course, no one can definitively answer that.

But what I can tell you is that over the past 10 years, Apple has never grown its revenue 126% in the space of just one year.

Camplify, at a much earlier stage of its life, has the potential to do anything.

The post Could buying this ASX growth stock at $2.17 be like investing in Apple in 2014? appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 10 November 2023

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- I’m buying cheap ASX shares to build my wealth in 2024 and beyond

- Here’s how the ASX 200 market sectors stacked up this week

- Which Nasdaq company just overtook Apple as the world’s largest by market cap?

Motley Fool contributor Tony Yoo has positions in Camplify. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Apple. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended Camplify. The Motley Fool Australia has recommended Apple and Camplify. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/gO58q37