This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

Both the pandemic as well as commission-free trading platforms like Robinhood have attracted a flurry of new investors into the stock market over the past couple of years. Retail investors have been playing a much larger role than ever before and have helped such meme stocks as AMC Entertainment and GameStop rally hundreds of percentage points at various times this year while the S&P 500 has enjoyed a strong but much more modest gain of 28%.

Yet not everyone has become rich from investing in these risky stocks and trends. Many investors have lost big money betting on stocks. If you’re a novice investor who has recently begun trading or are looking to get started investing in stocks next year, there are a few mistakes you’ll want to avoid making. Here are three of the biggest ones that rookie investors make.

1. Focusing too much on stock price

Oftentimes when I talk to relatively new investors, one of the things that comes up is a stock’s price. But whether a stock is trading at $20, $200, or $2,000 is completely irrelevant. The more important question is the stock price in relation to the company’s earnings — known as its price-to-earnings (P/E) ratio. Investors might also look at the stock price in relation to the company’s sales — known as its price-to-sales multiple.

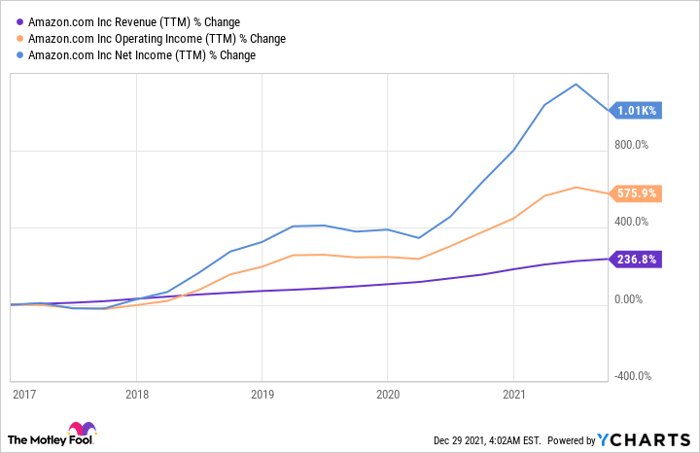

Consider tech giant Amazon (NASDAQ: AMZN), which trades at more than $3,400. That’s a big number, but that alone doesn’t mean it’s an expensive stock. Amazon reported diluted earnings per share of about $51 over the trailing 12 months, so the stock is trading at around 67 times those earnings (and less than four times its revenue). That isn’t cheap since the average stock in the Technology Select Sector SPDR Fund trades at only 34 times its profit. If Amazon’s stock were to fall to a P/E of 34, its shares would still be worth more than $1,700 — which again may look expensive — but its valuation would now be in line with a typical tech stock.

Thus, looking solely at a stock’s price without taking into context the company’s underlying earnings or revenue should not be used to evaluate whether its shares are expensive.

2. Focusing on the number of shares

One thing a stock price can impact is how many shares you may end up owning. If you’ve got $10,000, you’ll be able to buy roughly three shares of Amazon. But if you invested the same amount in tiny veterinarian health company Zomedica (NYSEMKT: ZOM), which trades at around $0.35, you could own more than 28,570 shares of the company.

In the end, it doesn’t matter how many shares you own. It’s the overall value of your investment that counts. A 10% increase in a $10,000 investment still represents a $1,000 profit, regardless of how many shares you own. So you want to be sure to own enough shares to meet your investment goal.

With Zomedica, you might be tempted to think that investing $100 in the stock is fine since you’ll own about 285 shares of the company. But a $100 investment is still a $100 investment, regardless of your stock count. If you’re spending the time to research stocks and find a good investment, make sure the investment is appropriately sized.

Of course, it’s also important to consider the size of any individual investment in relation to your overall stock portfolio, making sure not to be overly concentrated in any one stock.

3. Ignoring fundamentals

If you don’t spend much time researching and just feel as though you can risk taking a bet on the latest meme stock, that would be a big mistake as you could lose all your money. The fundamentals count.

Again, let’s look at Zomedica, for example. This stock was popular with retail investors in the early part of the year, hitting a peak of $2.91 on Feb. 8. It has since fallen a mammoth 88%. Even if you bought it at just $1.00 a few months later, it would still be down more than 60% today — a huge loss.

However, had you looked at the company’s fundamentals before investing in its shares, you would have been aware of some significant risks. It was only in March that the company announced the first commercial sale of Truforma, its flagship product that helps veterinarians run diagnostics on animals. Through the first nine months of this year, the company has generated just $52,000 in revenue while incurring losses of more than $15 million.

So with an unproven product and a stock that is soaring for no clear reason, the writing was on the wall that this was an extremely risky investment. Lesson: Do your homework before you invest.

Investors need to be more careful heading into 2022

Although the S&P 500 has been having another strong year in 2021, with a new COVID-19 variant out there and interest rate increases on the horizon, next year could be a perilous one for the economy and stock market. So it’s paramount that investors avoid big mistakes and make the best decisions they can with their money as 2022 approaches.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

The post 3 rookie mistakes to avoid making in the stock market appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for more than eight years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the five best ASX stocks for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now.

*Returns as of August 16th 2021

More reading

- 2 compelling ASX shares that could be buys in 2022

- Here’s why the Resonance Health (ASX:RHT) share price is rocketing 36% today

- What’s going on with the Australian Clinical Labs (ASX:ACL) share price lately?

- 3 fantastic ASX 200 shares to buy in 2022

- Insiders have been buying Nuix (ASX:NXL) and this ASX share

David Jagielski has no position in any of the stocks mentioned. John Mackey, CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. owns and recommends Amazon. The Motley Fool Australia has recommended Amazon. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

from The Motley Fool Australia https://ift.tt/3qxLjq7