This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

Self-driving technology has been advancing quickly over the last decade, and there are now a handful of companies operating fully autonomous commercial vehicles in the market. And it may surprise you to find out that Tesla (NASDAQ: TSLA) is not yet one of those launching fully autonomous vehicles, despite the attention it has received about its driver-assist technology.

Alphabet‘s (NASDAQ: GOOG) (NASDAQ: GOOGL) Waymo and General Motors‘ (NYSE: GM) Cruise are now operating fully autonomous ride-hailing services in the San Francisco area, and Waymo is also operating in the Phoenix area, both without a safety driver. If all goes according to plan, within the next few years, fully autonomous ridesharing will likely be available in some cities in the U.S., and the companies leading the way include some surprising names.

Where self-driving stands today

There are eight companies with permits to operate driverless tests in California, where most of the country’s self-driving testing is taking place. Four have deep ties to China, and we’ll set them aside for now given the uncertainty facing Chinese technology companies both in China and in the U.S. Those companies are Auto X, Baidu, Pony AI, and Weride.

The other four companies have received approval to bring self-driving technology to market and in some cases are already offering rides to the public.

- Cruise: This is GM’s self-driving unit, which currently has a permit to give autonomous rides to the public. The company has also already built about 100 Cruise Origin vehicles and is testing those vehicles right now. It doesn’t have a commercial launch date, but given the state of its testing, we can likely expect something sooner than most, at least on a limited basis.

- Waymo: This is Alphabet’s self-driving unit, operating in both Phoenix and San Francisco. The company is currently operating Jaguar vehicles and has ambitions in commercial trucking as well.

- Nuro: This is the only company with a permit for commercial operation in California. Nuro isn’t a ride-hailing company, but rather a delivery company. It’s partnered with Domino’s, Chipotle, CVS, and others to bring goods to people’s doors. It’s an autonomous driving service and it’s here!

- Zoox: Owned by Amazon (NASDAQ: AMZN), the company announced a ridesharing vehicle late in 2020 but has been very quiet ever since. We don’t know if its ambitions are for commercial ridesharing operations or something within Amazon’s operations.

All four of these companies should be taken very seriously because of the technology they’ve developed. But they’re taking their technologies to market in very different ways.

Building a company to last

Developing self-driving technology is one thing. Building a business will be another. Companies are going to have to build the physical vehicle infrastructure, attract a network of users, and continue to build and advance technology. This will take an incredible amount of cash.

Nuro’s path to the market is clear. It’s delivering goods to people’s doors, and, with a custom vehicle design and pods that keep items safe and secure while in transport, this could be a future vision of delivery if it can scale fast enough to beat the competition.

Waymo, being owned by Alphabet, has enormous resources and capital behind, so access to capital isn’t a problem compared to other independent ventures. The company has a product called Via that aims to bring autonomous driving to commercial vehicles. It’s also testing an autonomous ride-hailing service, which it could launch more broadly. But it’s not clear if there’s a custom vehicle in development, as Cruise and Zoox have developed, to make ridesharing a reality.

Cruise has been much more upfront with its plans, the Cruise Origin, which is under development. The company also has a war chest of $10 billion to deploy vehicles, $5 billion of which came from GM Financial. Cruise is majority-owned by GM, and that gives the company the ability to tap into GM’s manufacturing expertise and its financing muscle to grow. It’s already doing that, and that may give it a leg up in building an autonomous driving business.

Why isn’t Tesla on the list? In its home state of California, the company reported only 12.2 miles of autonomous testing on California’s public roads during 2019 and zero miles in 2020. The company is clearly trying to sell autonomous driving features to customers, but they aren’t fully autonomous and are not meant to replace the driver. In fact, it’s not even testing a fully autonomous driving system — at least, it’s not doing any tests on public roads in California that it’s reporting to regulators.

Where should your autonomous dollars be going?

As a public stock investor, if I were to bet on any two companies in autonomous driving it would be Waymo and Cruise. Zoox seems to have great technology but it’s unknown what Amazon will do with it and Nuro is still privately held, so isn’t eligible for investment by retail investors.

Waymo and Cruise are clearly industry leaders in self-driving vehicles, and they’re already transporting people around cities in the U.S. The difference between them is the upside they could generate for their respective owners.

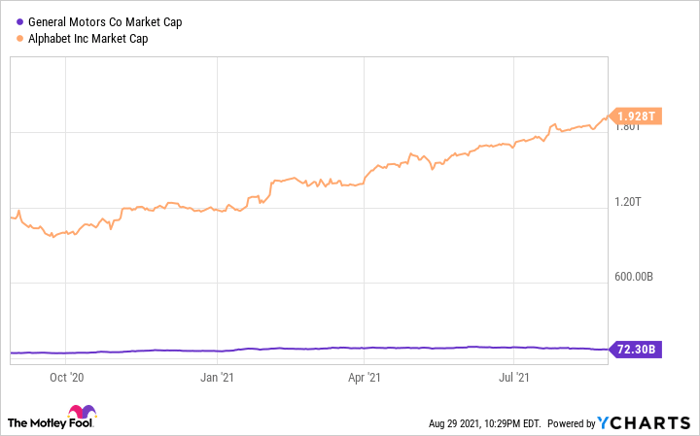

Alphabet is a nearly $2 trillion company, and Waymo’s impact on a company that size will be limited just because of the company’s current size. GM, on the other hand, is a $72 billion company, and if Cruise becomes a valuable business it would be transformational. Cruise is already valued at about $30 billion, so the upside for GM from that level is simply much higher than it is for Alphabet.

GM Market Cap data by YCharts

Despite being somewhat under the radar, GM has arguably built the most impressive autonomous driving business in Cruise. The company has a custom vehicle in testing, a manufacturing partner, billions in financing, and it could launch to the public in the next year or two based on plans to launch in Dubai late in 2023 and in San Francisco sometime ahead of Dubai. If self-driving cars are indeed going to be a revolution in transportation stocks, GM may have the most to gain.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

The post Self-driving cars are here and the leaders may surprise you appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for more than eight years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the five best ASX stocks for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now.

*Returns as of August 16th 2021

More reading

- ASX investors were buying Alibaba, Pfizer shares last week

- Why Apple stock jumped to a new all-time high on Monday

- Why CBA (ASX:CBA) is backing the RBA in push for payment reforms

- Amazon investors are getting its e-commerce business for free

Travis Hoium owns shares of Chipotle Mexican Grill and General Motors and has the following options: long March 2023 $250 puts on Tesla. John Mackey, CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. owns shares of and has recommended Alphabet (A shares), Alphabet (C shares), Amazon, and Baidu. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended CVS Health and Domino’s Pizza and has recommended the following options: long January 2022 $1,920 calls on Amazon and short January 2022 $1,940 calls on Amazon. The Motley Fool Australia has recommended Alphabet (A shares), Alphabet (C shares), and Amazon. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

This article was originally published on Fool.com. All figures quoted in US dollars unless otherwise stated.

from The Motley Fool Australia https://ift.tt/3zXhbbh