The Carsales.com Ltd (ASX: CAR) share price has jumped into the green again on Monday, reaching a new record high at $25.98.

It’s been a great few weeks for shares in the online automotive company, with the Carsales share price up almost 16% in the past month. In contrast, the S&P/ASX 200 index (ASX: XJO) has slipped 0.08% lower over the same period.

What are the tailwinds behind Carsales shares?

The Carsales share price has been on the move since the company reported its FY21 earnings in mid August.

In its report, Carsales recognised a 4% year on year increase in revenue, whereas earnings before interest, tax, depreciation and amortisation (EBITDA) grew 20% to $241 million.

This led to a net profit after tax (NPAT) of $131 million, a 9% increase from the year prior.

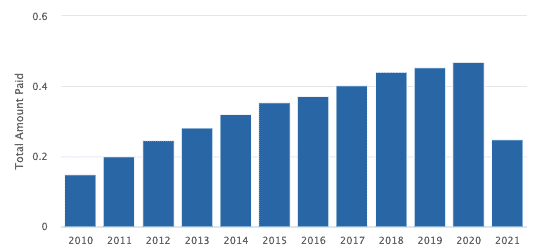

In addition, Carsales gave its dividend a 10% haircut from FY20, setting a final dividend payment of 22.5 cents per share.

Carsales dividend history 2010 – 2021

Source: The Motley Fool

Despite the dividend cut, Carsales’ shares have shown strengths on the chart, as investors look towards the company’s earnings growth instead.

The Carsales share price immediately shot up from $22.72 to $25.60 in the week following its FY21 earnings release, and has gained more than 14% from this event to date.

Carsales also completed the 49% acquisition of Trader Interactive in an announcement on 1 September.

Trader Interactive is a digital marketing corporation and a “provider of online market places and digital marketing products”.

Carsales advised that the acquisition was financed through a successful $600 million fully underwritten pro-rata accelerated renounceable entitlement offer and an “upsize” of the company’s existing debt facilities.

Given there has been no other market sensitive information for the company over the last month, it appears that investors are buying Carsales shares on the back of this momentum.

Carsales share price snapshot

The Carsales share price has climbed 31.3% into the green since January 1 and has gained 29.6% over the previous 12 months.

Both of these results have outpaced the S&P/ASX 200 index (ASX: XJO)’s return of around 25% over the past year.

The post Up 15% in a month, the Carsales.com (ASX:CAR) share price hits record high appeared first on The Motley Fool Australia.

Should you invest $1,000 in Carsales.com right now?

Before you consider Carsales.com, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Carsales.com wasn’t one of them.

The online investing service he’s run for nearly a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

*Returns as of August 16th 2021

More reading

- These ASX 200 dividend shares slashed their payouts in August

- 2 ASX shares shining this results season

- ASX 200 drops, Bendigo Bank sinks, JB Hi-Fi rises

- Here are the top 10 ASX shares today

- Carsales (ASX:CAR) share price records a modest rise on dividend slash

The author Zach Bristow has no positions in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has recommended carsales.com Limited. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/2YwqEsn