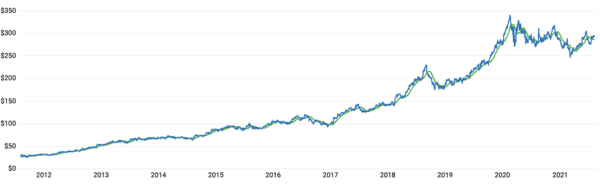

The Fortescue Metals Group Limited (ASX: FMG) share price has risen over the past 12 months, up 24%. And this doesn’t even include the juicy dividends that the company pays shareholders every time it reports its bi-annual results.

Understandably, Fortescue has been a hot topic since the spot price of iron ore has surged to astronomical levels. During July, the steel making ingredient hit US$219.77 per metric tonne – an all-time high. However, as all good things must come to an end, the spot price of iron ore has settled to around US$171.91, down 5.81% today.

Nonetheless, you may be wondering if you invested 5 years ago in Fortescue shares, how much would you have now?

Quick take on Fortescue

Recognised as the world’s fourth largest iron ore miner, Fortescue has become a dominant player in the mining industry. With world-class assets located in the Pilbara region of Western Australia, the company has been booming in recent times.

Fortescue traditionally enjoys a close trade relationship with China, which has been a major consumer of iron ore for the past decade. Although until recently, strained ties between Australia and China have sought to put a dent in the iron ore industry.

How has the Fortescue share price performed in 2021?

In the past 8 months, the Fortescue share price has been swinging both up and down throughout the period.

The company reported a strong quarterly result that drove its shares to a record high of $26.58 in late July. Yet this was only to be met by Chinese rhetoric about cutting its iron ore reliance on Australia. Since then, Fortescue shares have been off a cliff, declining 12% in just 1 week.

What would be the value of Fortescue shares buying from 5 years ago?

If you had invested $2,000 in Fortescue shares in 2016, you would have bought them for around $4.59 a piece. This gives you approximately 435 shares, without reinvesting the dividends received over those years.

Fast-forward to today, the current Fortescue share price is at $22.98. This means that those 435 shares would be worth $9,996.30 (435 shares x $22.98). When looking at percentage terms, this implies an upside of close to 400%, or on average an 80% yearly return.

Are Fortescue shares a buy today?

A number of brokers rated the company with varying price points following its June quarter results in late July.

JPMorgan cut its 12-month price target by 3.3% to $29 for Fortescue shares. Following suit, both Credit Suisse and Goldman Sachs also reduced their rating, down 4.3% to $22, and down 2.9% to $19.90 per share, respectively.

The post If you invested $2,000 in Fortescue (ASX:FMG) shares 5 years ago, this is how much it would be worth now appeared first on The Motley Fool Australia.

Should you invest $1,000 in Fortescue right now?

Before you consider Fortescue, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Fortescue wasn’t one of them.

The online investing service he’s run for nearly a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

*Returns as of May 24th 2021

More reading

- ASX 200 midday update: REA & ResMed results, Afterpay jumps

- Why the Fortescue (ASX:FMG) share price is tumbling lower on Friday

- 3 ASX 200 mining giants making moves towards renewables

- Fortescue (ASX:FMG) share price falls on COVID-19 scare

- Why the Fortescue (ASX:FMG) share price is struggling this week

Motley Fool contributor Aaron Teboneras has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/3yvd2KO