With interest rates around the developed world close to zero, and central banks pumping trillions of dollars into global financial systems in quantitative easing (QE) programs, share market and housing prices have been remarkably resilient in the face of the pandemic.

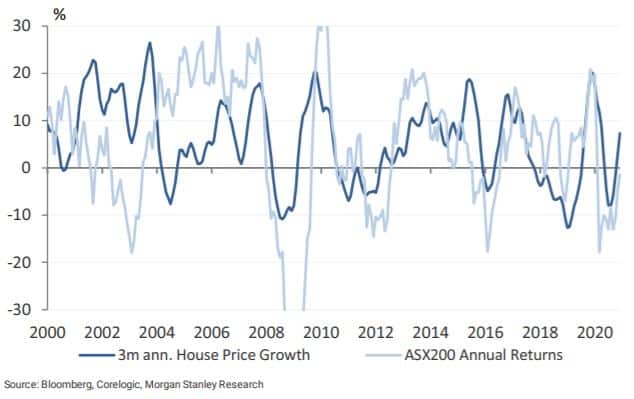

In fact, in Australia, our house prices have now edged above the level they were at before the pandemic struck.

The S&P/ASX 200 Index (ASX: XJO), slipping today, is only 5% below its all time February 2020 highs.

It’s a similar story in China, where speculators are snapping up prime properties. And China’s benchmark CSI 300 Index (SHA: 000300) is just 3% below its own record high which was set last week on 25 January.

25 January is the same date that the United States benchmark S&P 500 (INDEXSP: .INX) closed at new all time highs as well. It’s down a slender 0.7% since then.

With asset prices soaring amid economies still hamstrung by COVID-19 and an uncertain vaccine outlook, should you be worried about the potential for bursting bubbles?

Not particularly. At least, not according to the leaders of some of the world’s top central banks.

US Fed buying $1.9 trillion of bonds per year

If you thought the Reserve Bank of Australia’s (RBA) QE program was impressive, have a gander at the US Federal Reserve.

The Fed has been buying US$120 billion of bonds per month. That’s US$1.44 trillion (AU$1.9 trillion) per year. The bank has said it will maintain the purchases until “substantial further progress” is made towards its employment and inflation goals. The Fed has also indicated its target interest rate is unlike to increasing for the current 0.00–0.25% range any time soon.

However, the Fed has distanced itself from being the cause of asset bubbles or the recent share market volatility fuelled by speculative retail trading frenzies around likes of GameStop Corp. (NYSE: GME).

Asked about the concerns, St. Louis regional Fed President James Bullard said (quoted by Bloomberg):

I’m not really seeing that right now. Fed policy has been appropriate given the crisis that we are in. I think it has helped to stabilize the economy and put the economy on a recovery path since May of 2020, and that recovery looks poised to continue, possibly very strongly.

People’s Bank of China injects $56 billion in 3 days

Moving closer to home, the People’s Bank of China (PBoC) is no stranger to market intervention.

As the Australian Financial Review reports, the PBoC injected174 billion yuan (AU$55.7 billion) into the financial system to bring down the soaring overnight lending rate. That’s the rate banks tend to charge each other for short-term loans. The overnight rate has now fallen from 3.33% to a more palatable 1.85%.

While some analysts fear that volatility in the overnight rate could lead to tighter monetary policy, Haitong International Securities chief economist Sun Mingchun dismisses those concerns. Speaking at VanEck’s China investor symposium, Sun said:

A lot of the investors are quite worried about a tightening in China’s monetary policy. We have seen some slight changes over the past few months but I think it’s not a change in direction. It’s more about trying to be practical and flexible. I don’t worry about monetary tightening. I think the People’s Bank of China is very smart. They are very flexible in determining their monetary policy.

RBA’s Lowe “not essentially” worried

Bringing it back home, the RBA on Tuesday left the official cash rate at a rock bottom 0.1%. The central bank also committed to another $100 billion of government bond purchases once the first $100 billion program runs its course in April.

How long can we expect this to continue?

According to Governor Philip Lowe:

The Board remains committed to maintaining highly supportive monetary conditions until its goals are achieved. Given the current outlook for inflation and jobs, this is still some way off.

I see.

So should ASX investors and property owners and investors be worried about the possibility of deflating bubbles?

Not essentially so.

According to Lowe (quoted by the AFR):

Am I worried about asset prices rising too quickly? At the moment, not essentially so. At the moment, I don’t see anything that’s unsustainable. I find it hard to express concerns about either of these developments in asset prices to date…

There’s a lot of focus at the moment on the fact that housing prices are rising again and the stock market has been strong. Well, the national house price index today is where it was four years ago… and the equity market, we’re back to where we were at the beginning of last year.

Lowe did point out that the RBA will be keeping a sharp eye on lending standards. Lowe stated “we would be concerned if there were to be a deterioration in these standards”. Adding “but there are few signs of this at the moment.”

So there you have it.

To date, the world’s most powerful central banks have worked alongside their governments to help keep housing prices and share markets from crumbling under the pressure of viral mitigation measures and the devastating impact of the virus itself.

And to date, the leaders of those banks appear confident they can manage any bubbles that may arise.

Where to invest $1,000 right now

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for more than eight years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes are the five best ASX stocks for investors to buy right now. These stocks are trading at dirt-cheap prices and Scott thinks they are great buys right now.

*Returns as of June 30th

More reading

- GameStop (NYSE:GME) appoints 3 new Vice Presidents from Amazon and Chewy

- The worst isn’t over for GameStop: Here’s why

- GameStop chaos: How Aussie fund doubled money in 2 days

- COVID, US stimulus, Gamestop and a retreating Reddit army: The battles continue

- Millionaire maker! Rent.com.au (ASX:RNT) share price now up 300% in a week

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

The post These central bankers aren’t worried about share market bubbles. Should you be? appeared first on The Motley Fool Australia.

from The Motley Fool Australia https://ift.tt/2My8iBx