One-fifth of Australian share investors would own shares that went against their personal beliefs if it meant reaping a higher return.

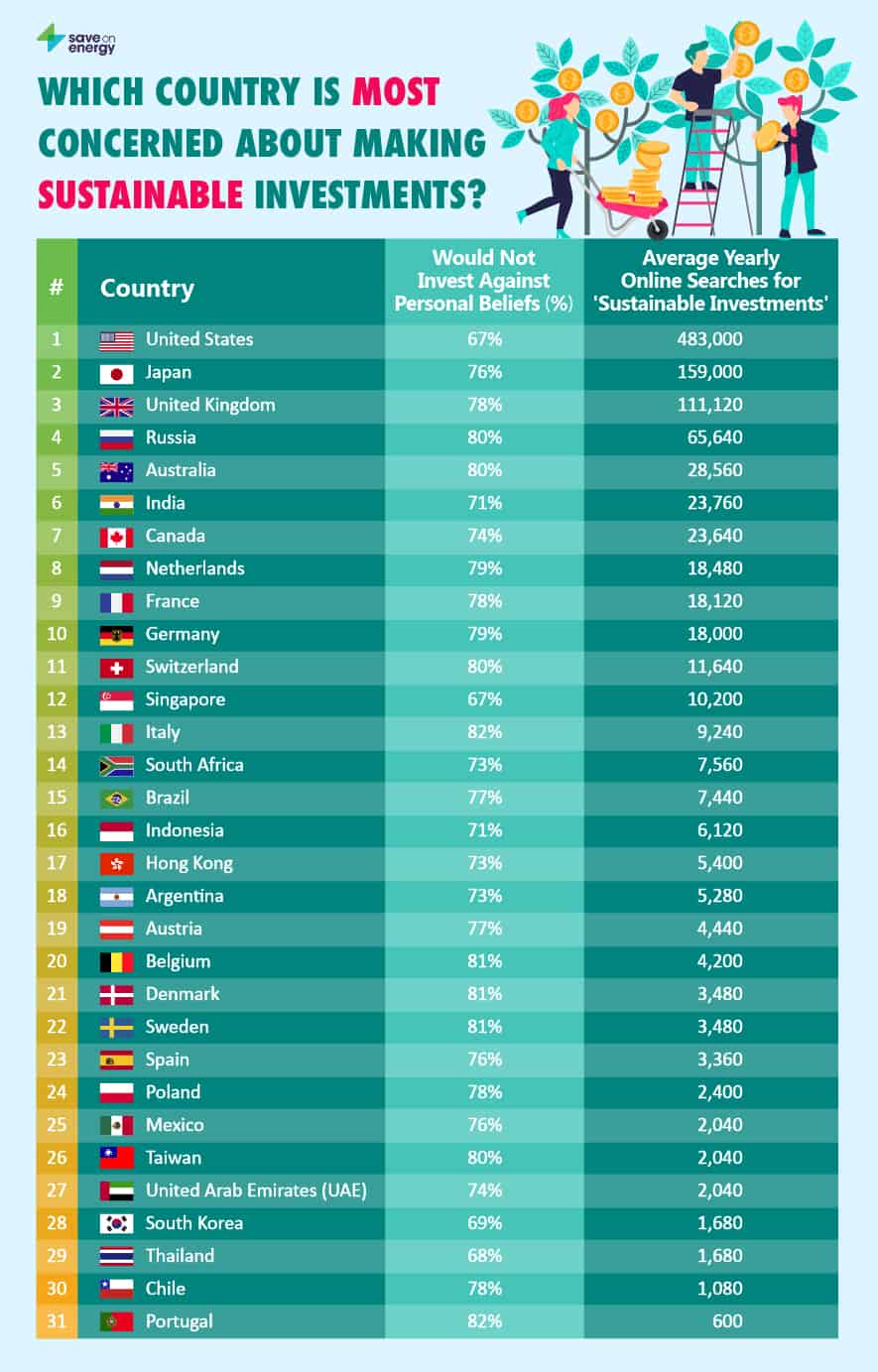

The finding came out of an international study conducted by UK company SaveOnEnergy, which showed US and Japanese investors were the most concerned about holding sustainable investments.

The data, sourced from investment firm Schroders (LON: SDR), showed Australians were ranked 5th.

Although 80% of Australian investors would never buy into a company that went against their moral code, 20% were willing to go for it in the search for higher returns.

The environmental issue that the most Australian investors thought companies should be focusing on this year was global warming.

Environmental priorities for Australian investors

| Rank | Issue | % of Australian investors |

|---|---|---|

| 1 | Global warming (climate change) | 59% |

| 2 | Plastic pollution | 55% |

| 3 | Air pollution | 52% |

| 4 | Biodiversity loss | 47% |

| 5 | Food waste | 44% |

| 6 | Deforestation | 40% |

| 7 | Water pollution | 36% |

| Source: SaveOnEnergy; Table created by author | ||

Plastic pollution and air pollution were not far behind, with 55% and 52% respectively judging it as a high priority in 2021.

Almost 2-in-3 Australian investors thought companies can do “much more” this year to improve environmental sustainability.

World is moving on to a new era

Despite the significant number willing to sacrifice the environment for higher returns, the world seems to be moving on with finances and sustainability increasingly linked to each other.

The rise-and-rise of Tesla Inc (NASDAQ: TSLA) shares is a case in point.

Investors savvy enough to bet that zero-emission electric cars are the way of the future saw their stocks rise almost 700% during 2020. Tesla shares have soared another 4% on top of that in the first few days of this year.

A more local example is AGL Energy Limited (ASX: AGL)’s Liddell power plant.

Last month investor groups called for the coal-powered station to be shut down.

Source: SaveOnEnergy

An AGL employee suffered a serious injury after an incident at one of Liddell’s power generation units, causing it to be temporarily closed. The unit could be inactive for 2.5 months, skipping over the entire high-demand summer season.

Australasian Centre for Corporate Responsibility director Dan Gocher said at the time maintenance costs for ageing coal plants increased from 25% of AGL’s total capital spend in 2013 to 74% in the 2020 financial year.

“Investors must question whether this expenditure is in the long-term interests of shareholders,” he said.

“AGL intends to operate Bayswater beyond 50 years, and Loy Yang A beyond 64 years. It’s ridiculous and completely out of step with Australia’s climate goals and it will continue to risk the safety of its workers.”

Forget what just happened. We think this stock could be Australia’s next MONSTER IPO…

One little-known Australian IPO has doubled in value since January, and renowned Australian Moonshot stock picker Anirban Mahanti sees a potential millionaire-maker in waiting…

Because ‘Doc’ Mahanti believes this fast-growing company has all the hallmarks of genuine Moonshot potential, forget ‘buy now pay later’, this stock could be the next hot stock on the ASX.

See how you can find out the name of this stock

Returns as of 6th October 2020

More reading

- Why ASX lithium shares are running hot in 2021

- Why the AGL Energy (ASX:AGL) share price is climbing today

- Tesla’s Q4 deliveries soar

- Forget Tesla. Facebook is a better buy now

- These were the worst performers on the ASX 200 last week

Tony Yoo has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. owns shares of and recommends Tesla. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

The post 20% of Aussie investors would take high returns over personal ethics appeared first on The Motley Fool Australia.

from The Motley Fool Australia https://ift.tt/2ME2iHd