The CSL Limited (ASX: CSL) share price is defying the market selloff and pushing higher on Thursday.

In afternoon trade, the biotherapeutics giantâs shares are up almost 1% to $286.37.

This compares favourably to a 1.4% decline by the ASX 200 index.

Why is the CSL share price outperforming?

Investors have been buying CSLâs shares despite there being no news out of the company.

However, when market volatility is high and the global economic outlook becomes uncertain, companies with defensive earnings are often in favour with investors.

CSL ticks a lot of boxes here. Because it develops life-saving therapies, they are in demand with end-users whatever is happening in the economy.

In addition, plasma is a key ingredient in the companyâs therapies. This means that it relies heavily on plasma donations at its collection centres.

When the global economy is booming, there is less need for people to donate plasma. This can lead to CSL having to increase its financial reward for donations. Whereas when thereâs an economic downturn, there are more people willing to donate and collection costs tend to reduce accordingly.

The team at Citi is likely to approve of anyone buying CSL shares today. It currently has a buy rating and $350.00 price target on the companyâs shares. This implies potential upside of 22% from current levels.

Before you consider CSL , you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and CSL wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor James Mickleboro has positions in CSL. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended CSL. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/c3qQyP9

S&P/ASX 200 (ASX: XJO) shares are rebounding on news of stronger-than-expected jobs data and an $80 billion central bank bailout for Switzerland’s second-largest bank.

During morning trade, the benchmark ASX 200 index fell by more than 150 points following dramatic trading sessions across Europe and in the United States overnight.

At the time of writing, the ASX 200 has recovered somewhat to be down 101 points, or 1.43%.

What’s helping the ASX 200 recover this afternoon?

Credit Suisse Group AG has announced it is taking out an A$81 billion loan from Switzerland’s central bank.

This follows a 24% plunge in Credit Suisse shares overnight after its major shareholder refused to up their stake.

This caused a bank share rout in France, Germany, the United States, and here in Australia this morning.

Credit Suisse has been besieged by various problems over time, with its market capitalisation halved since 2021.

The bank’s shares have tumbled by more than 50% since early February.

In a statement, Credit Suisse said:

Credit Suisse is taking decisive action to pre-emptively strengthen its liquidity by intending to exercise its option to borrow from the Swiss National Bank (SNB) up to CHF 50 billion under a Covered Loan Facility as well as a short-term liquidity facility, which are fully collateralized by high quality assets.

Credit Suisse also announces offers by Credit Suisse International to repurchase certain OpCo senior debt securities for cash of up to approximately CHFÂ 3Â billion.

The cash tender on 10 US-dollar-denominated senior debt securities will expire on Wednesday, 22 March.

What other news is pushing the ASX 200 higher?

The Australian Bureau of Statistics has released its monthly labour force data today.

The data revealed a surprise fall in the seasonally adjusted unemployment rate to 3.5%.

This is back to where it was in December. The rate went up to 3.7% in January.

ABS head of labour statistics Bjorn Jarvis said:

The latest monthly increase in trend employment was only slightly below the monthly average for the 20 years before the pandemic.

This now shows that, while underlying employment growth has slowed down compared with what we saw through much of 2022, it is still increasing at close to its long-term historical rate.

The better-than-expected data indicates the economy is still doing well despite inflationary pressure.

Low unemployment indicates businesses are thriving, which is why the ASX 200 is up on the news.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bronwyn Allen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/okMVp1A

The past week has certainly not been kind to ASX shares and the S&P/ASX 200 Index (ASX: XJO). Over the past five trading days, the ASX 200 has fallen by a nasty 4.7% â a dramatic fall by any reading. But that’s nothing compared to the woes of the Flight Centre Travel Group Ltd (ASX: FLT) share price.Â

Flight Centre shares have certainly had a week to forget. At the end of last Wednesday’s session, this ASX 200 travel stock was asking $19.70 a share. Today, Flight Centre is trading at just $17.50 at present.

That’s down a depressing 3.77% for the day alone, and down by an even more sobering 11.14% since last Wednesday:

So what’s going on with Flight Centre shares that have made this ASX 200 travel company such a poor performer over the past week?

Why has the Flight Centre share price seen so much turbulence this week?

Well, it’s hard to say. The last time we had any news from the company itself was on Monday. As we covered at the time, Flight Centre told investors that its recent share purchase plan (SPP) had been successful.

So much so that the company decided to raise $60 million instead of the original $40 million. That was despite demand of up to $350 million from investors.Â

These shares were issued at a price of $14.60, which has probably played a major role in the share price weakness we have seen over the past week. The funds raised from investors will go towards the acquisition of the British luxury travel company Scott Dunn.

Together with Flight Centre’s ongoing presence on the ASX 200’s most shorted shares list, this share purchase plan looks like the most likely reason Flight Centre had had such a tough week. But it’s not the only ASX 200 travel share that has.

Most of Flight Centre’s peers in the travel sector have also dramatically underperformed the broader market since last Wednesday. The Qantas Airways Limited (ASX: QAN) share price has lost almost 7% over the same period, while Corporate Travel Management Ltd (ASX: CTD) shares are down by close to 8%.

So it was always going to be a tough week for the Flight Centre share price. No doubt investors will be hoping for a smoother end to the trading week tomorrow.

Should you invest $1,000 in Flight Centre Travel Group Limited right now?

Before you consider Flight Centre Travel Group Limited, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Flight Centre Travel Group Limited wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor Sebastian Bowen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has recommended Corporate Travel Management and Flight Centre Travel Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/2xXoSI1

S&P/ASX 200 Index (ASX: XJO) oil stocks are having a day to forget, with the big oil and gas companies facing multiple headwinds.

In early afternoon trade, the Santos Ltd (ASX: STO) share price is down 3.7% while Woodside Energy Group Ltd (ASX: WDS) shares have tumbled 5.17%.

Indeed, while the ASX 200 is down a hefty 1.42% at the time of writing, the S&P/ASX 200 Energy Index (ASX: XEJ) has dropped 4.4%.

So, whatâs going on?

What are investors considering?

ASX 200 oil stocks are being hit with two related but separate concerns that have sent the Brent crude oil price to its lowest level since late 2021. Brent is currently trading for US$73.95 per barrel.

First, investors are broadly skittish as the contagion from the United States banking crisis has spread to Europe.

Last week markets were roiled by the collapse of US-based SVB Financial Group (NASDAQ: SIVB), or Silicon Valley Bank.

This week itâs Credit Suisse Group (SWX: CSGN) stoking investor fears. With the bank struggling to access additional funds, the Credit Suisse share price cratered 24% on the SIX Swiss Exchange overnight, reaching new all-time lows.

The prospect of a global banking crisis is sparking fresh recession fears. And a world in recession would demand less oil.

Thatâs the demand side.

The second concern hitting ASX 200 shares today is an oversupply of crude oil. At least in the short term.

According to a monthly report just out from the International Energy Agency (IEA), oil stockpiles are at 18-month highs. Thatâs partly due to Russia managing to actually up its crude production in February, despite international sanctions.

The IEA noted (quoted by Bloomberg):

World oil supply should comfortably exceed demand in the first half of the year. Much of the supply overhang reflects ample Russian barrels racing to re-route to new destinations… Russian oil supply has held up surprisingly well following its invasion of Ukraine … the country is still shipping roughly the same amount of oil to world markets.

Is now the time to buy ASX 200 oil stocks?

With ASX 200 oil stocks now well into the red in 2023, is now the time to buy?

That, of course, hinges on how crude oil prices track over the remainder of the year.

But for investors with a medium-term horizon of at least a year or so, I believe both the Santos and Woodside share prices will trade significantly higher inside the next 12 months than where theyâre at today.

Of course, there are no guarantees. And both ASX 200 oil stocks may well slide further from their current levels in the short term.

But the outlook for oil demand in the latter half of 2023 remains robust.

Both the Organization of Petroleum Exporting Countries (OPEC) and the IEA believe oil demand from China â the worldâs number two economy and most populous nation â will increase over the year.

CBA mining and energy analyst Vivek Dhar also believes China will help drive an uptick in global oil demand, along with the worldâs second most populous nation, India.

Dhar said he expects the current ample supply scenario wonât last, which will drive crude oil prices higher in the second half of the year.

âWe see deficit risks rising in H2 2023, as global oil supply growth, driven mainly by US, Norway and Brazil, fails to keep up with global oil demand growth,â he said.

Dhar forecasts the Brent oil price will increase to $US88 per barrel in the second half of 2023.

Thatâs up 19% from todayâs oil price.

If that proves accurate, it should offer some strong support for the ASX 200 oil stocks.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

SVB Financial provides credit and banking services to The Motley Fool. Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended SVB Financial. The Motley Fool Australia has recommended SVB Financial. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/oCrDiNa

In afternoon trade, the S&P/ASX 200 Index (ASX: XJO) is on course to record a sizeable decline. At the time of writing, the benchmark index is down 1.4% to 6,970.9 points.

Four ASX shares that are falling more than most today are listed below. Hereâs why they are dropping:

The Bendigo and Adelaide Bank share price is down 3% to $8.83. This follows news that the banking crisis has spread to Europe with Credit Suisse the latest bank rumoured to be fighting for survival. And while the Swiss central bank has assured Credit Suisse that it will provide extra liquidity if needed, it isnât painting a positive picture of the sector as a whole.

The BHP share price is down 4% to $43.73. This follows a similarly large decline by the mining giantâs shares on the NYSE during overnight trade. This has been driven by concerns over the state of the global economy and what this might mean for commodity demand and pricing.

The IPH share price is down 12% to $7.37. Investors have been selling this intellectual property services companyâs shares after it was hit by a cyber-attack. IPH advised that it detected unauthorised access to a portion of its IT environment on 13 March. An investigation into the incident could take âsome time to complete.â

The Woodside share price is down 5% to $31.20. This has been driven by another pullback by oil prices overnight on global economic growth concerns. WTI crude oil futures fell more than 5% to settle at US$67.61 per barrel, whereas Brent crude oil fell 4% to settle at US$74.36 per barrel. WTI crude oil futures were at their lowest level since December 2021.

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has positions in and has recommended Bendigo And Adelaide Bank. The Motley Fool Australia has recommended IPH. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/jnI5TfW

The Coles Group Ltd (ASX: COL) share price has performed quite well since the start of 2023, rising by around 7%.

That compares to a return of just 0.2% for the S&P/ASX 200 Index (ASX: XJO). The index is suffering today amid banking problems in the northern hemisphere with Silicon Valley Bank and now Credit Suisse.

As for Coles, its share price last traded above $19 in August 2022. But much has happened since then, with multiple interest rate rises in Australia, as well as annual inflation still stubbornly high.

For me, one of the biggest drivers of longer-term share price performance is profit improvement and plans for business improvement.

Despite the Coles share price being down close to 10% since August 2022, the company has actually delivered sales and earnings growth since then.

This enabled dividend growth of 9.1% to 36 cents per share.

Coles is divesting its Coles Express to Viva Energy Group Ltd (ASX: VEA), which is why the supermarket business has outlined its âcontinuing operationsâ earnings so investors can see the performance of the ongoing business.

By the end of FY23, the business is expecting to achieve cumulative smarter selling benefits of $1 billion across its four-year program. Some of these benefits include trolley-assisted checkouts, energy reductions across heating, ventilation, and cooling, measures to tackle theft, and the use of advanced analytics and store-specific data to âmarkdown ratesâ.

Can the outlook drive the Coles share price higher?

Coles said that in the third quarter of FY23, its supermarkets’ volume growth returned to âmodestly positiveâ from mid-January.

However, supplier input cost pressures remain, âparticularly related to packaged goods, wages and energyâ.

In January, the supermarket business commenced operations at the Witron automated Queensland distribution centre, with the receipt of its first inbound supplier deliveries. Itâs expecting to ramp up operations in the fourth quarter of FY23.

I think that the new distribution centres can help improve Colesâ efficiencies and profit margins. The business has made the right moves, in my opinion, by investing in these impressive buildings.

With ongoing food inflation and a return to volume growth, I think Coles will be able to deliver profit growth and dividend growth.

With the current Commsec estimates, the Coles share price is valued at 22x FY23âs estimated earnings with a potential grossed-up dividend yield of 5.3%. With ongoing profit growth expected over the financial years to FY25, I think Coles will be able to generate more investor interest and rise to $19 and beyond.

My colleague James Mickleboro also reported on Citi’s $20.20 price target on Coles, which implies the next 12 months could be a promising time for investors.

One “Under the Radar” Pick for the “Digital Entertainment Boom”

Streaming TV Shocker: One stock we think could be set to profit as people ditch free-to-air for streaming TV (Hint It’s not Netflix, Disney+, or even Amazon Prime.)

Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has positions in and has recommended Coles Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/aMgmdRT

In afternoon trade, the S&P/ASX 200 Index (ASX: XJO) is off its lows but still on course to record a disappointing decline. The benchmark index is currently down 1.45% to 6,966.3 points.

Four ASX shares that are not letting that hold them back are listed below. Hereâs why they are charging higher:

The Atlantic Lithium share price is up 11% to 49 cents. Investors appear to be taking advantage of recent weakness to pick up shares in this lithium explorer. Its shares were crushed after being hit by a scathing short attack alleging corruption. The company has refuted these claims.

The Pushpay share price is up 15% to $1.30. This morning, this payments company revealed that it has received an improved takeover proposal from Pegasus BidCo. According to the release, Pegasus has lifted its offer by 6% from NZ$1.34 cash per share to NZ$1.42 per share. This represents an offer of A$1.32 per share and values Pushpay at A$1.52 billion.

The St Barbara share price is up 3% to 59.2 cents. Investors have been buying gold miners again on Thursday in response to the market volatility. This has led to the S&P/ASX All Ordinaries Gold index rising over 0.5% this afternoon.

The Temple & Webster share price is up 2.5% to $3.54. This has been driven by news that the online furniture retailer is undertaking an on-market share buyback. Temple & Webster intends to acquire up to $30 million worth of its shares over a 12-month period starting on 3 April. It commented: âThe board considers the acquisition of shares at prevailing prices to be effective capital management while retaining financial flexibility to fund accretive organic and inorganic opportunities as part of its growth strategy.â

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Pushpay and Temple & Webster Group. The Motley Fool Australia has positions in and has recommended Pushpay. The Motley Fool Australia has recommended Temple & Webster Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/YKJvfFL

The S&P/ASX 200 Index (ASX: XJO) is tumbling today, but most S&P/ASX All Ordinaries Index (ASX: XAO) gold shares are defying the sell-off to leap higher.

In contrast, the benchmark ASX 200 Index is 1.51% in the red today.

So why are ASX investors buying up All Ords gold shares today?

What’s going on?

ASX All Ords gold shares appear to be rising today amid a lift in the gold price overnight.

Amid market turmoil, investors appear to be turning to gold as a safe haven asset.

The gold price rose by more than 1% to its highest level since early February during Wednesday’s trade in the USA, Reuters reported. Spot gold hit US$1,924.63 per ounce.

Commenting on this pivot to gold, Blue Line Futures chief market strategist in Chicago, Phillip Streible said:

It’s a total safe-haven trade. There’s a lot of concern about Credit Suisse and now European banks are really coming under quite a bit of pressure. So it’s a complete flight to safety.

The ASX 200 is struggling today after the S&P 500 Index (SP: .INX) slid 0.7% and Dow Jones Industrial Average Index (DJX: .DJI) fell 0.87% in the USA overnight. News that Swiss bank Credit Suisse’s largest investor would not raise its stake beyond 10% (as reported by Reuters) sent the market into turmoil.

However, gold is bucking this trend. We saw a similar pattern on Tuesday, with ASX investors turning to gold despite the ASX 200 sliding.

In a research note this morning, ANZ economist John Bromhead commented on today’s gold rally in the midst of the banking crisis. He said.

After a shaky start, gold rallied sharply as investors rushed to have assets amid the widening banking crisis.

Investors struggled to form a unified view on the Federal Reserveâs next move. Producer prices in the US unexpectedly fell in February. This comes following strong consumer prices earlier in the week. However, fresh woes at Credit Suisse saw safe haven buying continue to pick up. This was aided by the sharp drop in yields on US Treasuries.

Despite the rise overnight, the gold price is now pulling back and is down 0.89% to US$1,914.20 an ounce, CNBC data shows.

Motley Fool contributor Monica O’Shea has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Bevf3Zs

The Bendigo and Adelaide Bank Ltd (ASX: BEN) share price is down 2.86% today as ASX bank shares are hammered in the fall-out from the Credit Suisse stock plunge overnight.

As we reported earlier, shares in Switzerland’s second-largest bank fell 24% as fear spreads of a contagion in the global banking system following the collapse of two banks in the United States over the past week.

We’ve seen a 105-point fall in the S&P/ASX 200 (ASX: XJO) today, with bank shares faring badly.

What’s happening with ASX bank shares?

Among the small ASX bank shares, the Bendigo Bank share price has fallen the most at 2.86%.

Shares in Bank of Queensland Ltd (ASX: BOQ) are down 1.96%.

The big four banks are not immune, either. They all opened lower this morning before recovering a little.

At the time of writing, the ANZ Group Holdings Ltd (ASX: ANZ) share price is down 1.63%.

The National Australia Bank Ltd (ASX: NAB) share price is down 1.02% while the Westpac Banking Corp (ASX: WBC) share price has dropped 1.64%.

Commonwealth Bank of Australia (ASX: CBA) shares have recovered somewhat to be just 0.06% lower.

It is unclear why the Bendigo Bank share price has been hit hardest among the small ASX banks.

The Credit Suisse drama

To recap, Credit Suisse stock plunged last night after its major shareholder, the Saudi National Bank (SNB), said it would not increase its holdings to prop up the Swiss bank.

SNB holds a 9.88% stake in Credit Suisse and can’t buy more because of regulatory restrictions.

Credit Suisse shares are now down by more than 50% since early February.

The Swiss central bank has said it will give Credit Suisse extra liquidity if needed.

Motley Fool contributor Bronwyn Allen has positions in Anz Group, Commonwealth Bank Of Australia, and Westpac Banking. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has positions in and has recommended Bendigo And Adelaide Bank. The Motley Fool Australia has recommended Westpac Banking. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/pX9hBOr

All of us at some point — barring a miraculous cure for aging — will succumb to our mortality. The following proceedings of remembrance and celebration of life will typically then be placed in the hands of a funeral operator, perhaps even the ASX All Ords share I recently invested in.

Last week, I decided it was time to bring Propel Funeral Partners Ltd (ASX: PFP) into my portfolio. The second-largest funeral operator by market share had been on my watchlist for years. During this time, I found the management team’s execution of growth consistently impressive.

The combination of a solid interim result and a falling share price sealed the deal. Alas, I secured 463 shares at an average price of $4.31 — $1,995 worth of what I believe is an exceptional company.

Follow along as I explain:

Why I’m expecting 17% per annum returns from this investment over the next five years

An area of the business I think could be overlooked

The line in the sand for a sell

Let’s begin!

What does the industry look like?

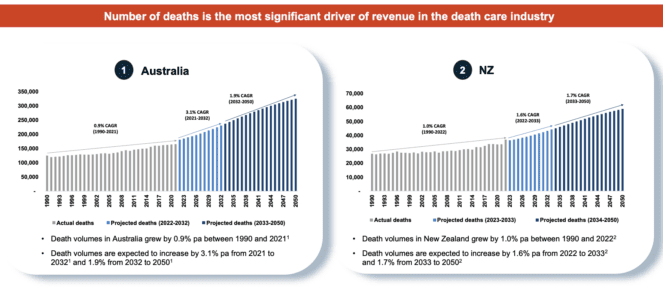

Firstly, Propel should benefit from a sector-wide tailwind for the death care services industry over the coming decades. The reality of the situation is the developed world has an aging population, leading to more deaths on an annual basis.

As noted by Propel, the next decade or so is forecast to see a compound annual growth rate (CAGR) of deaths in Australia of 3.1%. For context, this is more than three times higher than the rate of growth between 1990 and 2021.

While the increase in deaths is expected to slow between 2032 and 2050, it is still predicted to outpace our current historical rate, as shown below. If these forecasts are to be believed, most funeral operators should see an uplift in revenue.

Source: Propel Funeral Partners FY23 First Half Results Presentation

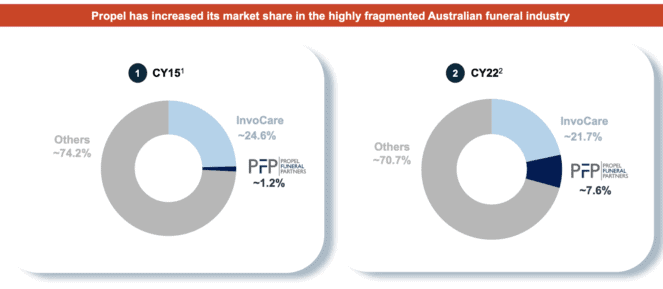

The other component of opportunity for Propel is a continuation in industry consolidation. Around 29% of the market is in the hands of InvoCare Limited (ASX: IVC) and Propel (at the end of 2022). Reducing the remaining market share — primarily made up of small independent and family-owned operators — to 71%.

Source: Propel Funeral Partners FY23 First Half Results Presentation

I believe consolidation begets consolidation. As the two largest companies in the industry take a greater share, small operators could come under greater pressure, increasing the likelihood of further mergers and acquisitions at attractive prices.

Clear growth strategy ahead

Propel holds a commendable track record for bolting on additional brands and operations. Since 2013, the company has expanded from one location in Queensland to 152 across most of Australia and New Zealand.

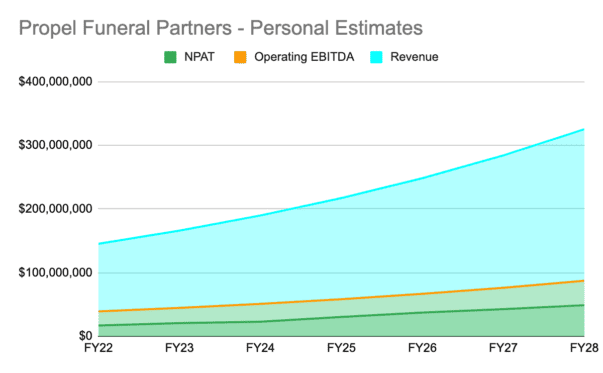

If the company continues to grow its market share, my conservative estimate is that revenue will grow at an annual compounded rate of around 14% out to FY28.

Realistically, I think Propel could end up exceeding this estimate. The company’s much larger rival, InvoCare, managed to grow its revenue by around 12% in both FY21 and FY22. Starting from a small base, Propel should find it easier to grow at a faster pace given the law of large numbers.

Please note these are my own personal estimates and should not form the basis of an investment decision

My own projections have this ASX All Ords share pulling in net profits after tax (NPAT) of $48.8 million in FY28. At that time, the business will be in a much more mature position, so I’ve assumed a price-to-earnings (P/E) ratio of 20 times.

These estimates add up to a projected market capitalisation of $914.5 million — 79.5% above today’s valuation.

What could be getting overlooked?

There’s another income source for Propel that I haven’t factored into my forward projections, that could deliver high-margin income… investment income from prepaid funerals.

It’s a somewhat controversial practice. Funeral providers offer people the option to pay for their funeral in advance, allowing the company to earn returns on the funds until they are required. As long as the funds are grown beyond the cost of the agreed-upon service, the difference can be pocketed.

Overall, the additional returns from this are likely to be modest. At the moment, Propel’s contract assets are actually $4.8 million in the red compared to its liabilities. However, it is worth at least knowing that this business practice could influence the bottom line later on.

What would prompt a change of mind?

Even the best companies can fail to deliver. That’s why it is helpful to lay out the conditions for failure in advance. For this, there are two key aspects of the business I’ll be keeping close tabs on:

Firstly, EBITDA margins will be valuable for monitoring any detriment to profitability if cremations grow in popularity.

The alternative to burials is a cheaper option, which could present a headwind. Propel’s most recent full-year margin came in at ~27%. Personally, I’d have some concerns if this metric were to fall below 20%.

Secondly, my thesis for this ASX All Ords share rests on management sustaining its approach to industry consolidation, increasing its market share. I personally don’t believe the company will grow to its valuation 100% organically. As such, if a halt to its acquisition activity occurred for some reason, I would reconsider my investment.

Final takeaway

There are few things in life as predictable as death. As an investor, I look at a company like Propel and see a business that provides an essential service. A service that possibly will never be disrupted.

The older I get, the more value I see in businesses that could exist for 30 years, 50 years — heck, even 100 years. Indeed, the best investment I could make is one that outlives me… how ironic.

Like other great long-term compounders on the ASX such as Washington H. Soul Pattinson and Co Ltd (ASX: SOL) and Brickworks Limited (ASX: BKW), Propel may not be the most exciting ASX All Ords share, but I think it could have the staying power needed to allow compounding to work its magic.

Should you invest $1,000 in Propel Funeral Partners Limited right now?

Before you consider Propel Funeral Partners Limited, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Propel Funeral Partners Limited wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor Mitchell Lawler has positions in Propel Funeral Partners. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Brickworks and Washington H. Soul Pattinson and Company Limited. The Motley Fool Australia has positions in and has recommended Brickworks and Washington H. Soul Pattinson and Company Limited. The Motley Fool Australia has recommended Propel Funeral Partners. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Ho1wmdT