The world economy’s uncertain outlook could prompt a second stock market crash in 2020. Risks such as political challenges in North America, Brexit and the ongoing coronavirus pandemic may contribute to weaker investor sentiment that sends share prices lower.

Furthermore, market declines have taken place fairly frequently in the past. Therefore, planning ahead for their occurrence could be a prudent strategy.

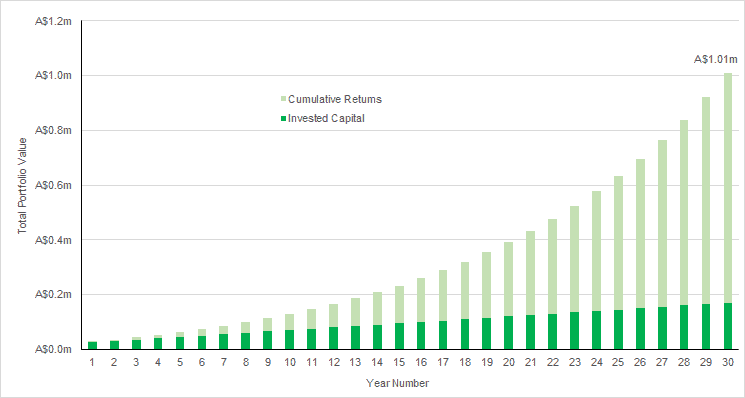

Through buying the best companies at the lowest prices today, you may be in a strong position to survive a market downturn and prosper from its recovery.

The risk of a second stock market crash

As mentioned, a second stock market crash could realistically occur in the near term. Although many stock prices have rebounded following the rapid downturn in stock markets across the world earlier this year, the outlook for the world economy is extremely challenging. Rising unemployment in many major economies, weak consumer confidence and poor financial performances from many businesses may cause investors to become increasingly risk averse.

Furthermore, upcoming events such as the US election and Brexit may affect trading conditions for some businesses and sectors. Alongside this, the coronavirus pandemic is a known unknown that could improve or worsen before the end of the year. Together, these risks may be sufficient to lead to greater selling among investors in the stock market – especially after the recent bull run.

Regular downturns

Of course, a stock market crash is not a new event. Stock prices have always been volatile at times, and have frequently been impacted by political, economic and other events that change the prospects of a wide range of businesses.

Therefore, it is good practice to ensure that your portfolio is always prepared for a potential fall in stock prices. This means that your holdings should not be overvalued. If they are, a lack of a margin of safety may mean that they suffer to a greater extent versus those businesses with valuations that factor in the potential for a downturn. Similarly, holding businesses with the financial strength and market position to overcome a period of weaker revenue growth could be a simple means of preparing for an economic downturn or bear market.

Capitalising on weak stock market performance

A stock market crash could also present buying opportunities for long-term investors. Cheaper shares can deliver superior capital gains versus the market. And, as the recent bear market showed, in many cases high-quality businesses have low valuations during a downturn as a result of weak investor sentiment towards the general equity market.

As such, holding some cash in preparation for the next downturn could be a shrewd move. It may mean you can buy stocks at cheaper prices for the long run. With risks currently high, it may also provide peace of mind ahead of the next downturn in stock prices.

Man who said buy Kogan shares at $3.63 says buy these 3 ASX stocks now

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for more than eight years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

In this FREE STOCK REPORT, Scott just revealed what he believes are the 3 ASX stocks for the post COVID world that investors should buy right now while they still can. These stocks are trading at dirt-cheap prices and Scott thinks these could really go gangbusters as we move into ‘the new normal’.

Find out the names of our 3 Post COVID Stocks – For FREE!

*Returns as of 6/8/2020

More reading

- Will you regret calling the Afterpay Ltd (ASX: APT) share price too expensive?

- Top brokers name 3 ASX shares to sell next week

- Top brokers name 3 ASX shares to buy next week

- 2 great LICs I’d buy for strong total returns

- Is the CSL (ASX:CSL) share price a buy?

Motley Fool contributor Peter Stephens has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

The post Why I’d start preparing for stock market crash part 2 today appeared first on Motley Fool Australia.

from Motley Fool Australia https://ift.tt/357bQzX