![]()

The CSL Limited (ASX: CSL) share price is climbing higher today following the release of its annual general meeting presentation.

At the time of writing, the biotherapeutics company’s shares up 1.5% to $302.96.

What was in CSL’s annual general meeting update?

As well as the usual rundown on its performance over the last 12 months and board changes, CSL provided the market with a trading update and its expectations for FY 2021.

According to the release, trading conditions have been relatively mixed for CSL this financial year because of the pandemic.

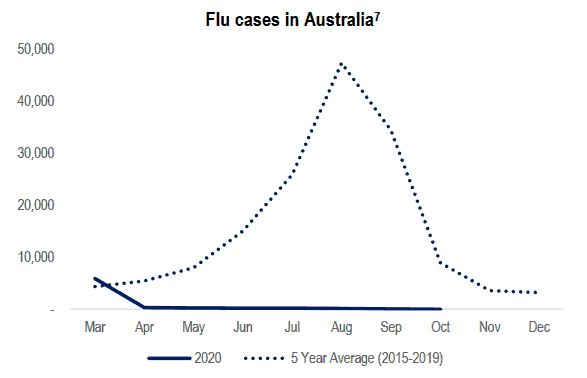

Management expects its Seqirus vaccines business to continue to benefit from its differentiated products and strong demand for influenza vaccines. The latter is being driven in part by Governments wanting to protect their populations from contracting COVID and influenza.

The company’s Albumin sales are expected to normalise following the successful transition to its new business model in China.

Management is also expecting strong demand for its plasma and recombinant therapies to continue. However, due to COVID restrictions, which are expected to restrain its ability to collect plasma, the costs of collection are expected to increase.

The good news is that the company has a number of initiatives underway to mitigate the impact.

What about research and development?

CSL also provided an update on its research and development (R&D).

While its R&D response to COVID, as well as new initiatives, will put upward pressure on its R&D expense, it is still expected to be within its guidance range of 10-11% of revenue.

Speaking of guidance, CSL has updated its profit guidance for FY 2021.

It now expects revenue growth in the range of 6 to 10% in FY 2021, with net profit after tax of approximately $2.170 to $2.265 billion in constant currency. The latter implies growth of 3% to 8%.

This is a slight tightening of the range advised with its FY 2020 results of 0% to 8%.

These 3 stocks could be the next big movers in 2020

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for more than eight years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

In this FREE STOCK REPORT, Scott just revealed what he believes are the 3 ASX stocks for the post COVID world that investors should buy right now while they still can. These stocks are trading at dirt-cheap prices and Scott thinks these could really go gangbusters as we move into ‘the new normal’.

Find out the names of our 3 Post COVID Stocks – For FREE!

*Returns as of 6/8/2020

More reading

- 3 ASX 200 growth shares to buy today

- $10,000 invested in the CSL (ASX:CSL) IPO is worth how much now?

- Ignore EBITDA and P/E ratios? This fundie does

- Leading brokers name 3 ASX shares to buy today

- ASX 200 Weekly Wrap: Budget, US election sparks 5% surge in ASX shares

James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. owns shares of CSL Ltd. The Motley Fool Australia has no position in any of the stocks mentioned. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

The post CSL (ASX:CSL) share price pushes higher on FY 2021 guidance update appeared first on Motley Fool Australia.

from Motley Fool Australia https://ift.tt/2SYx0dL