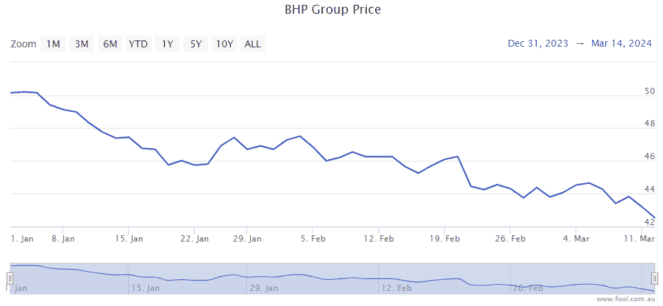

The BHP Group Ltd (ASX: BHP) share price has gone backwards by 15% in 2024. After a difficult couple of months for the ASX mining share, is it time to buy?

BHP has suffered from a falling iron ore price, as well as large one-off costs in its FY24 first-half result which included a write-down of its nickel assets, and more costs allocated for the Samarco disaster in Brazil.

Is the BHP share price a buy?

According to reporting by The Australian, the broker Citi has changed its rating on the ASX iron ore share to a buy, though its price target was unmoved at $46.

A price target is where the broker thinks the share price will be in 12 months.

At the current BHP share price â which is up more than 2% today at the time of writing â that would suggest a potential rise of close to 7% over the next 12 months. Any dividends paid would be a bonus on top of that.

Citi analyst Paul McTaggart said that BHP “now looks cheap enough” based on normalised valuation multiples.

The Australian reported McTaggart noted the enterprise value to earnings before interest, tax, depreciation and amortisation (EBITDA) ratio is 5 times, compared to the long-term average of 6.3 times. The price to cash flow ratio is 6.4 times, compared to the long-term average of 8 times.

In other words, if we look back at history, BHP is looking materially cheaper than it has in the past, based on those two ratios.

However, at the same time, Citi didn’t say that BHP was the cheapest ASX iron ore share. McTaggart explained:

We stay buy rated on Rio Tinto Ltd (ASX: RIO) and note it is still the cheapest of the large iron ore exposures with the highest mid-term production growth.

Other valuation metrics

According to the estimates on Commsec, the BHP share price is valued at 10 times FY24’s estimated earnings with a possible grossed-up dividend yield of 7.9% in FY24. We’ll have to see if Citi is right about the positive outlook for this ASX share over the next year.

The post Is the BHP share price now cheap enough to buy after falling 15% in 2024? appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 1 February 2024

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- How much could a $300,000 ASX share portfolio pay in dividends?

- Here’s the iron ore price forecast through to 2027

- After a rough start to 2024 these 3 ASX 200 mining stocks are looking cheap to me

- How much passive income will I get from shares vs. property?

- Why BHP, Brainchip, Lake Resources, and Yancoal shares are sinking today

Citigroup is an advertising partner of The Ascent, a Motley Fool company. Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/htN9ULc