The dust has settled on the February earnings season, giving us the opportunity to now reflect on the ASX shares that reported.

Unlike a typical recap of the standout winners and losers, I wanted to do something a little different — maybe more valuable — than other reporting season post-mortems.

While it can be useful to know which companies smoked expectations and which left their shareholders bitterly disappointed, often those exceptional reports are met with similarly exceptional moves in the share price (either positive or negative).

I’m more interested in the ASX shares with solid numbers that were maybe underappreciated. In my eyes, these could be companies that the broader market is disregarding for reasons outside of the fundamentals. But, in the long run, those fundamentals become rather hard to ignore.

So, here are the companies that failed to attract the level of attention I believe would be commensurate with their results.

The ASX shares working hard when no one is watching

Netwealth Group Ltd (ASX: NWL)

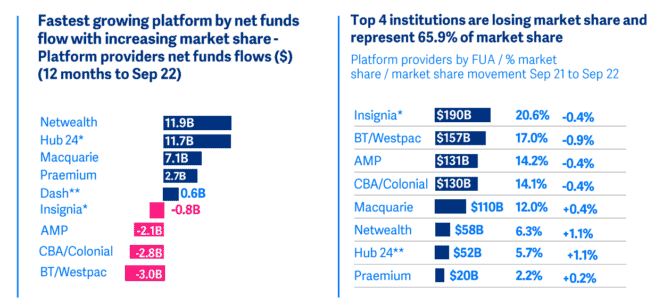

Netwealth brings wealth management to the twenty-first century with its cloud-based software platform. As its management attests, it is the fastest-growing financial services platform with $11.9 billion of net fund inflows for the 12 months to September 2022.

In my opinion, the Netwealth team delivered on all key objectives in the first half. Funds under administration (FUA) and funds under management (FUM) grew by 12.2% and 10.4% respectively. In turn, the company was able to increase its total revenue by 18.9% to $102.8 million and deliver a statutory net profit after tax (NPAT) of $30.6 million — up 12.9%.

Netwealth is executing its mission to provide a better platform than the big wealth-managing incumbents, as demonstrated by the image above. The company continues to nibble away at the market share of competitors.

How did investors react to the release? The Netwealth share price finished 2.7% higher on 15 February… hardly a move to write home about. Although the ASX share trades on a price-to-earnings (P/E) ratio of 56 times, I think there is a level of underappreciation for the extent of growth that could still lie ahead for Netwealth.

DGL Group Ltd (ASX: DGL)

The next company I believe the market could be sleeping on is chemicals manufacturer, transporter, storer, and processor, DGL Group. Shares in this ASX small-cap share finished flat after the company released its first-half results to the market on 28 February.

After a string of acquisitions during the half, DGL reported a 52% increase in sales revenue compared to the prior corresponding period. Impressively, the company notched up its earnings before interest, taxes, depreciation, and amortisation (EBITDA) by 35%.

I have a suspicion that the market may have written off DGL’s growth as purely a byproduct of acquisitions. However, as noted in the presentation, 69% of EBITDA growth was organic. Morgans also highlighted that the result showed an ability to grow organically. The broker currently has a buy rating on the ASX share.

What I find enticing about this company, that I think others are overlooking, is the moat it is building through its geographic footprint. Its operations are widely spread across Australia and New Zealand through its network of warehouses (see here). Such a network is difficult to replicate without significant capital.

In my opinion, the expanded network could give DGL an edge in terms of beating competitors on price for transport and product (due to scale) and time for delivery fulfilment (due to proximity).

Supply Network Limited (ASX: SNL)

The last ASX share that I think the market snubbed upon the release of its results during the earnings season is Supply Network. This company sells after-market parts primarily for trucks and buses within Australia and New Zealand.

Simply put, Supply Network’s results were extremely strong. Shares lifted a dismal 0.3% on the day of the company’s reporting. The half-year filing left a bit to be desired in terms of commentary and added details.

However, the numbers speak to a period of continued demand for parts. In quantifiable terms, revenue increased by 23.6% to $119.2 million, while net profits surged 34.1% to $12.7 million. These figures add to a consistent growth trend over the past five years, as depicted below.

Furthermore, analysts at Ord Minnet think the outlook is still solid for Supply Network with the broker holding an accumulate rating on the ASX share.

Personally, I share a similar perspective. Cost pressures could linger for a year or two, nudging the average tenure of truck ownership higher. As a result, replacement parts could be in higher demand.

Aside from this, the company’s balance sheet is in the strongest position its been in years, opening the door to additional growth avenues.

The post Underappreciated: 3 ASX shares I believe were the quiet achievers of earnings season appeared first on The Motley Fool Australia.

FREE Guide for New Investors

Despite what some people may say – we believe investing in shares doesn’t have to be overwhelming or complicated…

For over a decade, we’ve been helping everyday Aussies get started on their journey.

And to help even more people cut through some of the confusion “experts’” seem to want to perpetuate – we’ve created a brand-new “how to” guide.

Yes, Claim my FREE copy!

*Returns as of March 1 2023

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- Here are the top 10 ASX 200 shares today

- Wake up! Buy 5 ASX shares that are reporting season gems: Morgans

- 7 ASX 200 growth shares to buy for possible takeovers: expert

- 3 ASX 200 shares on the move amid strong earnings updates

- Why Cochlear, GUD, Netwealth, and Wesfarmers shares are charging higher

Motley Fool contributor Mitchell Lawler has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended DGL Group, Netwealth Group, and Supply Network. The Motley Fool Australia has positions in and has recommended Netwealth Group and Supply Network. The Motley Fool Australia has recommended DGL Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/7jGt5SA

Leave a Reply