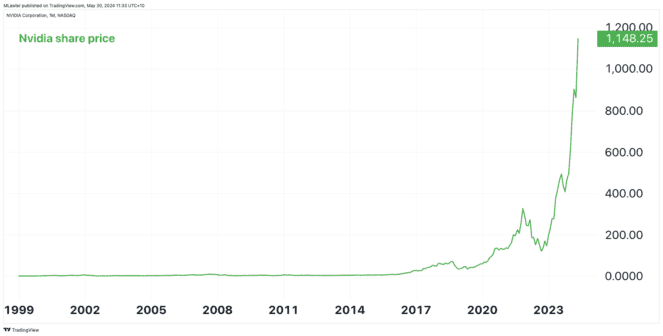

If the share market were a sport, Nvidia Corp (NASDAQ: NVDA) stock would be in the running for MVP of 2024. The computer chip technology company extended its record share price last night, reaching US$1,154.92 before settling at US$1,148.25.

Catapulted by the burgeoning demand for hardware to power artificial intelligence, the US-based graphics card maker has shot up the ranks of most valuable companies. Today, Nvidia is worth US$2.82 trillion, hot on the heels of Apple Inc (NASDAQ: AAPL) and Microsoft Corp (NASDAQ: MSFT) for the number one spot.

Only four short years ago, Nvidia’s market capitalisation stood at US$214.5 billion, one-thirteenth of what it is today. With the stock almost tripling in value in the past year alone, I think I’d be better off buying a certain ASX stock instead.

Buffett senses are tingling on Nvidia stock’s high

Don’t get me wrong… I believe Nvidia is a phenomenal company. Not that it matters from an investment perspective, but I’ve been on ‘Team Green’ for GPUs (graphic processing units) since saving enough money to buy my first high-performance gaming computer in 2015.

I toyed with the idea of investing in Nvidia stock many times over the years. In 2018 (up 1,900% since), in 2021 (up 400% since), and in 2022 (up 580% since). Not once did I pull the trigger, opting for Advanced Micro Devices Inc (NASDAQ: AMD) in its place. Betrayal of Team Green, I know.

But now, I can’t help but think there’s a bit of euphoria surrounding Nvidia.

I get a little nervous when a company’s stock price chart looks like the one below. If you’re a long-term investor, stock price action shouldn’t dictate whether to buy or sell. But it can tell you about investors’ mentality and mood.

A timeless quote from the legendary Warren Buffett is, “Be fearful when others are greedy, and be greedy when others are fearful”.

It’s rare now to hear anything but optimism about the demand for AI and the boost it will generate for Nvidia stock. My inner Buffett is detecting a euphoric vibe among investors. A ‘no questioning it, just believe!’ frame of mind.

Meanwhile, my mind is contemplating the ‘what ifs’…

What if demand for accelerated computing drastically tapers at a point?

What if Nvidia’s margins revert back to around 25% instead of its recent 53%?

What if Taiwan Semiconductor Manufacturing Co Ltd (NYSE: TSM), aka TSMC, lifts prices?

Personally, I think Nvidia’s growth is murkier now than it was two or three years ago. And while a 42 times forward earnings multiple mightn’t be the steepest ask, I’m not sure those earnings are sustainable.

Relocating the greed to where there’s fear

Channelling my inner Buffett again, I’m inclined to invest where fear has engulfed a good company. Often, this provides a greater margin of safety, minimising the downside and increasing the upside.

I genuinely believe Corporate Travel Management Ltd (ASX: CTD) is an ideal current alternative to Nvidia stock. It’s a completely different business, providing travel management solutions. However, like Nvidia, it is highly profitable, growing at an above-market rate, and is founder-led.

The difference is that this ASX stock trades at a price-to-earnings (P/E) ratio of 17 times, and its shares are out of favour — down 37% over the past 12 months. Weaker full-year FY24 guidance set the selling into motion on 21 February 2024.

I reckon the fear is overdone.

In my opinion, buying Corporate Travel Management now is more like buying Nvidia stock in 2021 or 2022 before the boom. It may not achieve the same meteoric gains, but I think there is less of a rosy outlook already baked into this ASX stock than Nvidia.

The post Which ASX stock I’d rather buy than Nvidia at $1,148 per share appeared first on The Motley Fool Australia.

Should you invest $1,000 in Corporate Travel Management Limited right now?

Before you buy Corporate Travel Management Limited shares, consider this:

Motley Fool investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Corporate Travel Management Limited wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

And right now, Scott thinks there are 5 stocks that may be better buys…

See The 5 Stocks

*Returns as of 5 May 2024

More reading

- Nvidia stock: 4 reasons to buy, 4 reasons to sell

- ‘Significant potential’: One unexpected ASX 200 AI share to buy now

- 1 ASX growth stock that turned $10,000 into $21,000 in less than 2 years

- Prediction: Nvidia stock will continue to rise…and here’s why

- Joining the revolution: How I’d invest in ASX AI shares right now

Motley Fool contributor Mitchell Lawler has positions in Advanced Micro Devices and Apple. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Advanced Micro Devices, Apple, Corporate Travel Management, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool Australia has positions in and has recommended Corporate Travel Management. The Motley Fool Australia has recommended Advanced Micro Devices, Apple, Microsoft, and Nvidia. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

screens, which will be suitable for a wide range of Android and Apple iPhones, with screens for tablets also being developed.

screens, which will be suitable for a wide range of Android and Apple iPhones, with screens for tablets also being developed.