If you want to make some buy and hold investments for your income portfolio, then it would be worth looking for ASX dividend shares with strong long-term outlooks.

But which shares could deliver the goods for investors over the next decade? Let’s take a look at three quality options:

APA Group could be a great buy and hold option for investors. Just ask its long term shareholders.

They will tell you that the energy infrastructure company is on course to increase its dividend for the 20th consecutive year.

The good news is that analysts at Macquarie believe this ASX dividend share can then continue this trend for the foreseeable future.

The broker is forecasting dividends per share of 56 cents in FY 2024 and then 57.5 cents in FY 2025. Based on the current APA Group share price of $8.33, this equates to 6.7% and 6.9%Â dividend yields, respectively.

Macquarie has an outperform rating and $9.40 price target on its shares.

Another ASX dividend share that could be a good buy and hold investment option is Coles.

It is one of Australia’s big two supermarket operators. In addition, it has a significant liquor store network and a joint ownership in the Flybuys loyalty program.

Combined, these businesses appear well-placed to support solid earnings and dividend growth over the long term.

Morgans appears to believe this is the case and is forecasting fully franked dividends of 66 cents per share in FY 2024 and then 69 cents per share in FY 2025. Based on the current Coles share price of $16.97, this implies yields of approximately 3.9% and 4.1%, respectively.

The broker has an add rating and $18.95 price target on its shares.

A third ASX dividend share that could be a great buy and hold option is Endeavour. It is the liquor giant behind store brands such as BWS and Dan Murphy’s, as well as a large network of hotels.

Goldman Sachs is very positive on the company due to its market leadership position and attractive valuation. It expects this to support the payment of fully franked dividends of approximately 21 cents per share in FY 2024 and then 22 cents per share in FY 2025. Based on the current Endeavour share price of $5.03, this will mean dividend yields of 4.2% and 4.4% yields, respectively.

The broker currently has a buy rating and $6.30 price target on its shares.

Motley Fool investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Apa Group wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

And right now, Scott thinks there are 5 stocks that may be better buys…

Motley Fool contributor James Mickleboro has positions in Endeavour Group. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group and Macquarie Group. The Motley Fool Australia has positions in and has recommended Apa Group, Coles Group, and Macquarie Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

Who doesn’t enjoy a boost to their income? Dividends are a big reason why many choose to invest. That’s why passive income chasers pay attention when an ASX 200 stock lifts its dividend payout ratio — bigger payments could be ahead.

Yesterday, a $17 billion Australian company highlighted an increase in its payout ratio. The determination, shared in an investor briefing, follows an extended period of debt reduction by one of the country’s steadfast energy providers: Origin Energy Ltd (ASX: ORG).

So, what does it mean for the back pockets of its shareholders?

Dividends to take a bigger share of earnings pie

Operating a utility company can be extremely capital-intensive. Just take a look at the gross margins of Origin and AGL Energy Limited (ASX: AGL). We’re talking respective margins of 20.8% and 28% before removing operating expenses.

Nonetheless, utility companies can still offer a fountain of dividends. Nearly every household’s needs-based nature of electricity and gas provides a reliable income. For Origin Energy, it means investors can enjoy a dividend yield of 4.8% from this ASX 200 stock.

But what about the increased dividend payout ratio?

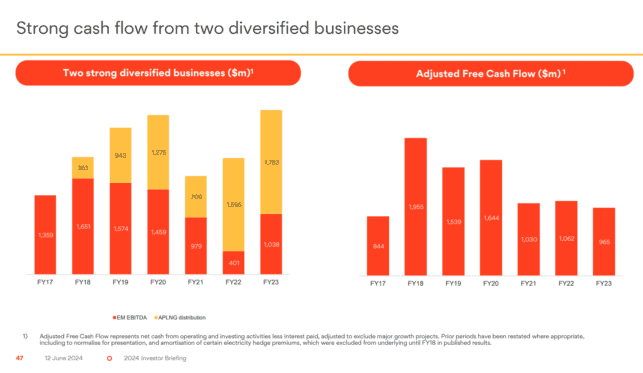

As per the investor briefing, Origin Energy will target a payout ratio of at least 50% of free cash flow.

This is slightly different from what a standard dividend payout ratio reflects. Typically, this figure is based on the percentage of net income or net profit after tax (NPAT) paid as a dividend. Free cash flow differs from NPAT, representing the company’s operating cash flow minus its capital expenditures.

Previously, Origin Energy’s targeted payout ratio was set between 30% and 50%.

Does it mean more dividends from this ASX 200 stock?

What really matters to most is whether it means more dollars hitting the account. Unfortunately, the answer to this is not as straightforward.

While Origin’s payout ratio now has a higher minimum, future free cash flows (FCF) will be the deciding factor.

Source: Origin Energy June Investor Briefing 2024

As shown on the right-hand side of the image above, the energy company’s adjusted FCF have stagnated across the last three financial years. If Origin’s free cash flow were to fall in FY24, it could mean a bigger slice of a smaller pie.

The share price of this ASX 200 stock is up 17.8% year-to-date.

Should you invest $1,000 in Origin Energy Limited right now?

Before you buy Origin Energy Limited shares, consider this:

Motley Fool investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Origin Energy Limited wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

And right now, Scott thinks there are 5 stocks that may be better buys…

Motley Fool contributor Mitchell Lawler has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

QBE Insurance Group Ltd (ASX: QBE) shares have been in fine form over the last 12 months.

During this time, the insurance giant’s shares have stormed 22% higher.

This is almost triple the return of the ASX 200 index over the same period.

Can QBE shares keep rising?

The good news for investors is that it isn’t too late to invest according to analysts at Goldman Sachs.

According to a note, its analysts have retained their buy rating and $20.90 price target on the company’s shares.

Based on its current share price of $18.32, this implies potential upside of 14% for investors over the next 12 months.

In addition, the broker is forecasting dividend yields of 5%+ each year through to at least FY 2026. This boosts the total potential 12-month return to approximately 19%.

If this proves accurate, it would turn a $10,000 investment into approximately $11,900 if you reinvest the dividends.

Why is the broker bullish?

Goldman notes that the insurance giant has recently held a number of investor meetings. It was pleased with what management said, highlighting that it is confident in can deliver a combined operating ratio (COR) of 95% in North America by 2025. As a reminder, anything below 100% is profitable for insurers.

In light of this, the broker believes that there is upside risk to consensus COR estimates. It said:

In this context, we flag 1) Upside risk to FY25 consensus COR of 92.8% (VA) – we see <92.5% as possible reflecting improvement from North America non core + organic upside. 2) North America non core run off we think could support ~0.7% -1.2% improvement to Group COR alone. 3) Organic trends also suggest possible underlying COR expansion into FY25.

Goldman also highlights a number of other key items and reasons why it thinks QBE shares could re-rate higher from here. It adds:

Rate increases earning through FY25 versus moderating claims inflation expected to remain supportive into FY25 – 1Q24 Group rate was 7.3% versus inflation assumption of 5% for FY24. b) Reinsurance markets increasingly more positive with commentary from 1 June renewals suggest lower rates (particularly in upper layers) which are supportive of direct insurer margins and positive read into 2025. c) QBE’s 2024 perils allowance was rebased to an 80% probability of sufficiency (out of the last 10 years) perhaps suggesting less pressure into FY25 and perils growth more in line with book. Perils experience to date has been below expectations. d) All in, there appears to be strong COR tailwinds to offset moderating yield pressures which is supportive of ROE / Valuation into FY25. 4) Valuation comparison versus global peers also suggests upside for QBE across P/E and P/B particularly in context of strong ROE.

Should you invest $1,000 in Qbe Insurance right now?

Before you buy Qbe Insurance shares, consider this:

Motley Fool investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Qbe Insurance wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

And right now, Scott thinks there are 5 stocks that may be better buys…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

The Steadfast Group Ltd (ASX: SDF) share price has dropped 8.9% over the past 12 months to close at $5.41 on Wednesday. The insurance broker’s shares have underperformed the S&P/ASX 200 Index (ASX: XJO), which is up 8% over the past year.

The following chart shows that the Steadfast share price has exhibited little volatility. Over the last 10 years, the maximum drop from the high price to the low has been 16%, except in March 2020 during the height of the COVID-19 pandemic.

While past share price movements don’t predict future trends, the resilient performance of the Steadfast share price seems to be supported by its strong fundamentals, in my view.

Steadfast Group is Australia’s largest general insurance broker network, providing businesses and individuals with a broad range of insurance products and services. The company operates through a network of brokerages, offering risk management solutions and support to its members. Steadfast also has interests in underwriting agencies, giving it a diversified presence in the insurance industry.

Steadfast reported a robust set of numbers in its 1H FY24 results. Underlying revenue rose 19.4% to $790.4 million, and underlying earnings before interest, tax, and amortisation (EBITA) soared by 21.4% to $229 million. While acquisitions supported the growth during the reporting period, the organic growth was also strong at 13.4%.

Its underlying net profit after tax (NPAT) increased by 17.5% to $106 million, while statutory NPAT rose similarly by 18.5% to $100 million. On a per-share basis, underlying diluted earnings rose 12.2% to 10.2 cents per share (cps).

Steadfast’s pricing power and volume growth underscored the strong results, while the company attributes its acquisition strategies as key to success. Managing director & CEO Robert Kelly explained:

Once again, our underlying earnings growth for the half year was driven by sustained organic growth from higher prices from insurers and volume increases in the Group’s insurance broking and underwriting agencies, and continued delivery of our acquisition strategy.

Consistent with our growth strategy, Steadfast Group acquired Sure Insurance, a business that is complementary to the existing portfolio. This acquisition, together with our Trapped Capital acquisitions made during the half year, further enhances Steadfast Group as the largest general insurance broker network and the largest group of insurance underwriting agencies in Australasia.

Additionally, we are progressing well with the implementation of our US expansion strategy with the acquisition of ISU Group with its established and trusted network and experienced management team.

For the full year in FY24, management guides for a 22% growth in its underlying EBITA and 18% in NPAT at the midpoint of its estimated range. Underlying diluted EPS growth is forecast to grow between 11% and 16%.

Consistent dividend payer

Among ASX investors, Steadfast is known for its steady increase in dividends.

Encouraged by a 12.2% growth in its underlying EPS in its half-year FY24 results, the company raised its fully-franked dividend by 12.5% to 6.75 cps.

Since its initial public offering in 2013, the company has consistently increased its dividend payments from 4.5 cps in FY14 to 15.75 cps in the last 12 months to March 2024. All these years, the company maintained 100% franking on its dividends, offering tax benefits to its shareholders. Its payout ratios have also increased over time, hovering around 60% to 75% in recent years.

At the current share price, Steadfast shares offer a dividend yield of 2.9%.

How expensive are Steadfast shares now?

Steadfast shares are trading at 20x FY24’s estimated earnings, which is near the midpoint of its historical trading range of 13 to 25 times.

Its smaller competitor, AUB Group Ltd (ASX: AUB), is trading at a similar multiple with a price-to-earnings ratio (PER) of 20 times based on FY24 earnings estimates provided by S&P Capital IQ.

For comparison, NIB Holdings Limited (ASX: NHF) is trading at a PER of 16 on FY24 earnings estimates, noting nib is an insurance company, which is different from insurance brokers.

Foolish takeaway

While the Steadfast share price has been moving sideways, I think its business fundamentals remain strong.

Based on its historical trading range and compared to its smaller peer, AUB Group, its shares appear to be inexpensive to me. I think it’s a good candidate for any portfolio seeking stable growth.

Should you invest $1,000 in Steadfast Group Limited right now?

Before you buy Steadfast Group Limited shares, consider this:

Motley Fool investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Steadfast Group Limited wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

And right now, Scott thinks there are 5 stocks that may be better buys…

Motley Fool contributor Kate Lee has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has positions in and has recommended Steadfast Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

Rob McElhenney and Ryan Reynolds are business partners, costars, and friends.

Randy Holmes/ABC via Getty Images

Rob McElhenney helped support Ryan Reynolds through one of the most stressful times in his life.

Reynolds says McElhenney took on more Wrexham responsibilities while he was working on the new "Deadpool."

"I'm lucky to call him my friend," the Marvel star told Business Insider.

Ryan Reynolds and Rob McElhenney aren't just business partners and costars on "Welcome to Wrexham," the FX docuseries that chronicles the pair buying a down-on-its-luck Welsh football club and turning it into a success. They're also good friends — and according to Reynolds, McElhenney helped him through a particularly stressful time in his life.

"It swallows my life whole," the actor says of making a "Deadpool" movie. Reynolds cowrote, produced, and stars in the latest, "Deadpool & Wolverine," alongside Hugh Jackman's Wolverine. "It becomes an all-hours, all-consuming, time-murdering obsession that needs to be born, raised, and sent to college in the span of 24 months."

Reynolds credits McElhenney with helping him balance his priorities, all while still allowing him to make time for his family, including his wife, Blake Lively, and their four kids.

"Over the last couple years, Rob has covered for me and cared for me in ways I can't fully comprehend," Reynolds tells BI. "He's helped me find space to see my family despite needing me in Wrexham."

Wrexham coowners Rob McElhenney and Ryan Reynolds celebrate Wrexham's promotion.

Martin Rickett/PA Images via Getty Images

Reynolds also noted it's not lost on him that McElhenney is juggling a lot, too — in addition to their shared Wrexham responsibilities, McElhenney also formed a new company, More Better Industries, that has a production arm, a creative consultancy, and an investment arm. That's not to mention his starring role on "It's Always Sunny in Philadelphia," the beloved FX comedy he created that's heading into its 17th season.

"Rob is running multiple businesses, making sure he's a present husband and dad, starring in approximately 42 television shows and somehow, some way, maintaining remarkably even skin," Reynolds jokes.

The duo's friendship, which originally started over DMs about four years ago, is something Reynolds cherishes.

"I fucking love the guy. Now and always," he says of McElhenney. "I'm lucky to know him. I'm lucky to work with him. I'm lucky to call him my friend."

Bethenny Frankel was married to Jason Hoppy from 2010 to 2012, and their divorce took nearly a decade.

Frankel started a YouTube Series chronicling her divorce experience.

She shared some of the dating red flags to watch out for before you marry someone.

In 2010, Bravo aired "Bethenny Getting Married," a one-season reality show documenting Bethenny Frankel's relationship with pharmaceutical sales executive Jason Hoppy.

The marriage lasted two years, and the couple had one child, Bryn Hoppy. The divorce took nearly a decade, finalizing in 2021 after Frankel filed for divorce in 2013.

"It was a brutal, brutal experience," Frankel, 53, told Business Insider. "I thought I would never survive it."

While Frankel shares practical divorce tips on the show, she also emphasizes the importance of spotting red flags early on.

Bethenny Frankel with her daughter, Bryn Hoppy.

Cindy Ord/Getty Images

"You can't marry someone that you wouldn't want to be divorced from," Frankel told BI. "The red flags that you see in dating will become fire engine-red flags when you're getting divorced." She said people can get "vengeful" throughout the process, especially when navigating custody battles.

Frankel shared some of her biggest dating red flags to watch out for early on in a relationship.

Charm is disarming

Frankel told BI that "charming" men should set off alarm bells.

She spoke more about the red flag in her series, stating that her life coach told her to run if charm is someone's primary personality trait.

"You don't own charm, charm owns you," she quoted the coach. Excessive charm is associated with narcissists and dark empaths, who use it to manipulate the people around them, according to therapists.

Lois M. Brenner, a divorce lawyer in New York, previously told Business Insider that she's had many clients say they were love-bombed and had "no idea who this person was" when they married them because of how charming they were at first.

While the song is a joke, Frankel still warned against going after trust fund guys in particular.

"You don't want a trust fund guy because of the way that they're going to ultimately treat you and discard you," she told BI. She believes that they will get bored and toss you aside because "they're insecure and they've been given everything."

Men can still be boys

Immaturity is another quality Frankel said to stay away from, because it can indicate how a partner handles disagreement.

She stressed the importance of being with someone who's emotionally mature. "You don't want to date boys, you want to date men," she told BI, adding that physical age means nothing. "A 65-year-old man could be a boy. A 25-year-old boy could be a man."

On TikTok, Frankel advised viewers to put men they're dating "through a strainer" and be really discerning. "If it's giving boy, it's giving 'bye,'" she said.

A weak 'yes' is a hard 'no'

Frankel said "cracks become craters" once you're married, so it's important to listen to your reservations.

"If you don't have a resounding, emphatic 'yes,' the answer is 'no,'" she told BI.

She added that someone's fears and expectations might make them feel obligated to go through with a marriage, such as their parents liking the person or feeling like they need to hit a certain milestone by a certain age. But none of that means you're ready to marry the person, and the consequences can be dire.

"You have to make smart decisions, and hopefully other people can learn from so many of my mistakes," Frankel said.

Since H5N1 made the unexpected jump from birds to cattle, experts are increasingly worried about human spread.

Rodrigo Abd/AP Photo

The bird flu, or avian influenza, is increasingly worrying public-health experts.

The H5N1 bird flu virus is changing, creeping closer to humans, and getting more opportunities to adapt.

A bird flu pandemic isn't inevitable, but it is possible. Here's why you should know what's going on.

Bird flu is flying wild, and it has many infectious disease experts more worried now than ever.

The H5N1 avian influenza virus has killed tens of millions of birds across the planet and more than 40,000 sea lions and seals. For animals, it's a pandemic.

Still, the CDC says the risk to humans is low. Most people seem to have very little chance, if any, of catching H5N1 avian influenza right now.

A farmer pets the head of his cow during a cow cuddle session at Luz Farms near Monee, Illinois.

Jim Vondruska/Reuters

But infectious disease experts are increasingly concerned that the H5N1 virus could make a sustained jump into humans and start spreading among us. That's not inevitable, but several recent developments suggest it's a growing threat.

"There's a lot going on," Dr. Monica Gandhi, a professor of medicine and associate chief of the Division of HIV, Infectious Diseases, and Global Medicine at the University of California, San Francisco, told Business Insider. "I'm becoming more worried."

You shouldn't panic, but you should probably know what's going on. This virus is a leading candidate for the next pandemic, and four developments in the past month have experts worried.

Here's what you need to know.

Bird flu hospitalized a child in Australia

On Friday the World Health Organization announced that a 2-year-old had become Australia's first human case of H5N1 in March.

After returning from travel to Kolkata, India, the child's symptoms — loss of appetite, fever, coughing, vomiting, and irritability, according to WHO — put them in the hospital for two and a half weeks, including admission to the intensive care unit.

As human cases crop up in different parts of the world, epidemiologists like Christopher Dye become more concerned.

"There's such a vast amount of virus at the moment. And clearly it is changing, and it's doing new and unexpected things," Dye, a professor and senior research fellow at the University of Oxford, told BI.

A researcher prepares milk samples in Sabeti Lab, which is testing purchased milk at area grocery stores for the presence of bird flu.

David L. Ryan/The Boston Globe via Getty Images

He recently co-authored a paper, published in the medical journal BMJ, arguing that the risk of a major human outbreak is "large, plausible, and imminent."

"Influenza has always been a concern for decades and decades, and this particular form of influenza for at least two decades," Dye said. "But now, it's risen to a level of concern, I think, which is greater than ever before."

Mice could bring bird flu into homes

A total of 47 house mice have tested positive for H5N1 in New Mexico, the US Department of Agriculture reported on Tuesday.

"Mice are kind of everywhere," Gandhi said. "They're around other animals, they're around humans a lot. And it's a little worrisome."

A mouse sits in the snow in New York City's Central Park.

Tayfun Coskun/Anadolu Agency via Getty Images

The samples were collected from the sick mice in early May. According to The Telegraph, scientists suspect that the mice, as well as some domestic cats, may have gotten the virus from drinking raw milk from infected cows. (Public health experts resoundingly advise that people should not drink unpasteurized, aka "raw," milk.)

"This brings the virus closer to human homes," Rick Bright, former director of the Biomedical Advanced Research and Development Authority, told The Telegraph. "This is out of control," he added.

Every new population of animals, and every new exposure to humans, is another opportunity for the virus to mutate and adapt.

One mutation suggests the virus has started adapting

An avian influenza A(H5N1) virion, viewed through an electron microscope.

Cynthia Goldsmith, Jackie Katz/CDC via AP

When the CDC analyzed a virus sample from the second US farmworker infected, they spotted a mutation in the virus's replication machinery — the way it gets inside its host's cells to make copies of itself.

It's a change "associated with viral adaptation to mammalian hosts," the CDC said in a statement in May. The statement also said that studies in mice indicate this type of genetic mutation in the virus is associated with more severe disease and enhanced viral replication.

That doesn't make it a human virus yet, though.

Other than this one change, H5N1 has mainly "avian virus properties and not human virus properties," Richard Webby, a virologist at St. Jude and director of the WHO Collaborating Centre for Studies on the Ecology of Influenza in Animals and Birds, told BI.

That means the virus is better adapted to thrive and spread among birds, not humans.

Still, that could change.

The latest US case had a troubling cough

The first two farmworkers to test positive for H5N1 in the US had pink eye. But the third case, reported in Michigan in May, featured a cough and sore throat.

That means H5N1 was in that worker's respiratory system, which is a scarier place to find a threatening virus than in our eyes.

Coughing can spread respiratory infections such as the common cold or COVID-19.

Stock Photo/Getty Images

The good news is that, as far as scientists can tell, H5N1 is still not adapted to humans enough to transmit between us. The CDC has reported no evidence that the coughing farmworker spread the virus to anyone else.

But that doesn't mean H5N1 can't mutate to achieve human-to-human transmission — which brings us to the second unfortunate reality of this farmworker's respiratory infection.

Compared to the eyes, human lungs are a more convenient place for an avian virus to get more mammalian, according to Webby. In the lungs, the virus is exposed to more of the cell receptors that a mammalian virus would bind to, giving H5N1 more opportunity to mutate and start grabbing onto those receptors — thereby becoming better adapted to infecting and spreading between humans.

Many experts fear the USDA and CDC aren't monitoring cattle and farmworkers closely enough to catch concerningmutations early, and that other human cases may be going undetected.

Talita de Lima Freitas, federal agricultural inspector, works on a sample to test for avian influenza virus at the Reference Laboratory of the World Organization for Animal Health in Campinas, Brazil.

Amanda Perobelli/Reuters

"I think there's enough of a threat here to be very alert so that we have a surveillance system in place that, as soon as this happens, we can find it," Dye said.

Vaccines are in the works

The good news is that bird flu is not COVID-19. Scientists have been tracking this virus and its entire viral family tree, watching for any sign of a growing threat to humans, for decades.

As a result, the key elements of a vaccine are already on standby. The US is beginning to manufacture millions of vaccines using "candidate vaccine viruses" — weakened influenza viruses — that the CDC has developed.

If H5N1 becomes a threat to humans, it could be part of your seasonal flu shot.

Marko Geber/Getty

Though the candidates are not necessarily perfect matches to H5N1, and the vaccines' use of eggs may be a manufacturing roadblock if bird flu is sweeping the chicken population, they may provide some immunity in the case of a human outbreak.

Furthermore, scientists now have proven mRNA vaccine technology at the ready. Vaccines that use mRNA, of which the COVID-19 vaccines were the first approved for use, are more flexible and faster to develop than traditional vaccines — and they don't require eggs.

Bird flu has driven up egg prices multiple times in the past few years.

Terry Chea/AP Photo

Researchers at the University of Pennsylvania have already developed an experimental mRNA vaccine for H5N1, which they've successfullytested in mice and ferrets.

If H5N1 becomes a problem in humans, a vaccine could be offered with the flu shot you get later this year.

In the meantime, bird flu is a looming threat to keep an eye on.

"As far as I can see, this is not going to go away anytime soon," Dye said.

Migrants line up along the US-Mexico border fence to apply for asylum in the United States on December 21, 2022.

John Moore/Getty Images

Immigration is one of the thorniest public policy issues and one that will define the 2024 election.

Biden has had to pivot on some of his border policies after running against Trump's efforts in 2020.

Meanwhile, Trump is seeking to run heavily on immigration this year, similar to his 2016 campaign.

Very few issues animate Americans more than immigration.

And under the presidencies of both Donald Trump and Joe Biden, divisions over the issue have only sharpened further.

Trump's 2016 presidential campaign was defined by his hard-line views on immigration: arguing for a wall at the US-Mexico border and insisting that Mexico pay for said barrier, pushing for the deportations of millions of undocumented immigrants, and calling for a temporary ban on Muslims entering the country.

Once in office, Trump sought to execute his broad vision. His administration constructed 455 miles of fencing along the southern border, but much of the wall simply replaced anti-vehicle barriers with taller steel bars. And despite Trump's rhetoric on ramping up deportations, the number of individuals who were removed from the US declined from October 2018 to September 2019.

Biden in the 2020 election strongly denounced Trump's immigration policies, voicing his opposition to a border wall, blasting the GOP administration's family separation policy, and promising a more humane approach toward migrants at the southern border.

But since Biden took office, an explosion in border apprehensions — along with scores of migrants arriving in Democratic-led cities like Chicago and New York — has became a political liability, with voters giving him low marks on the issue.

Here's a look at Biden and Trump's positions on immigration, one of the defining issues of the November election:

Where Joe Biden stands on immigration

Immigration has been one of the trickiest policy areas for Biden, as he came into office seeking to reverse many Trump-era policies but has instead often found himself on the defensive on the issue.

Republicans across the country have routinely excoriated Biden over border security since taking office, pointing their fingers at him over record levels of apprehensions at the border. In February, the GOP-controlled House of Representatives impeached Homeland Security Secretary Alejandro Mayorkas, contending that he had not enforced the country's immigration laws. (The Democratic-led Senate subsequently squashed the impeachment charges against Mayorkas.)

Texas GOP Gov. Greg Abbott over the past two years has pushed back against what he said is Biden's lack of border security by sending hundreds of thousands of migrants to Chicago and New York. And it's created a difficult situation for Democratic officials like New York City Mayor Eric Adams, who has had to tackle budgetary challenges in housing migrants.

Biden this year pushed for the passage of a Senate-crafted bipartisan bill, which would have overhauled the US asylum system, among other measures intended to strengthen security at the border. The bill seemingly put the president on the offensive on the issue, as he challenged congressional Republicans to back to proposal to get a handle on immigration.

But Senate Republicans overwhelmingly voted against the bill after Trump pressed them to tank it.

Biden last week signed an executive order that restricts asylum protections — to the frustration of immigration advocates — for migrants if there are more than 2,500 unauthorized daily border crossings over a seven-day average.

Where Donald Trump stands on immigration

Trump has staked much of his 2024 campaign on Biden's vulnerabilities on immigration among voters.

In a New York Times/Siena College poll conducted in April, 50% of registered voters approved of Trump's handling of the issue while he was in office. Meanwhile, only 32% of registered voters approved of Biden's handling of immigration.

The former president was instrumental in tanking this year's bipartisan immigration bill, blasting it as a "horrible open borders betrayal" during a January rally in Las Vegas.

Trump has made it clear that he intends to crack down on illegal immigration should he retake the White House.

The former president's conservative allies have already begun drafting executive orders and memos in preparation for potential early actions to restrict migration at the US-Mexico border, according to The Wall Street Journal.

During Trump's sole term in the White House, he also made it more difficult for foreign-born workers — which included many highly-skilled scientists and engineers — to come to the US on visas. A second Trump administration could very well see a return to such policies.

The Woodside Energy Group Ltd (ASX: WDS) share price hit a 52-week low this week, dropping to $26.99 on Tuesday. It could be a contrarian buy when resource and cyclical businesses hit lows. The Woodside share price is down around 20% in the past year, as shown on the chart below.

It’s common for share prices of companies in sectors like iron ore or retail to be volatile over the years as investors react to what’s happening.

As reported by my colleague Bernd Struben, the Organization of the Petroleum Exporting Countries and its partners (OPEC+) will lift production in October, with current production cuts removed by June 2025. Higher supply could result in lower prices.

But, Struben also reported earlier this week that energy prices are rebounding, with the Brent crude oil price up to around US$82 per barrel (up from US$79.62 on Friday).

Is the Woodside share price a buy?

Sometimes, the best time to buy a cyclical share is when there are numerous negatives which are expected to stick around the foreseeable future. It’s under those conditions where the share price can reach the most appealing low, making it the best time to invest.

The company is one of the region’s biggest oil and gas businesses, so its scale provides it with several benefits, including solid profit margins and a sturdy balance sheet.

I like the moves by the company to improve its balance sheet further. In the last few months, the company has completed the sale of a 10% stake in the Scarborough joint venture to LNG Japan for US$910 million, and it announced the sale of a 15.1% stake in the Scarborough joint venture to JERA for US$1.4 billion.

We can’t know what energy prices will do in the short term, but unlocking some of the value of its projects is wise, in my opinion. It gives the company more funding for existing projects such as Trion while also giving it a cash pile for future projects, acquisitions and/or shareholder returns.

Another recent positive for the business was that its Sangomar project achieved ‘first oil’, which will soon generate another stream of earnings for the company.

My verdict

With the lower Woodside share price, prospective investors can receive a larger dividend yield. The broker UBS currently projects that Woodside could pay an annual dividend per share of US$1.05, which translates into a grossed-up dividend yield of approximately 8%.

If investors are interested in Woodside shares, this could be a good time to consider investing because of its lower valuation, the high projected dividend yield and the first oil achievement at Sangomar. But, some investors may not like the company because of the fossil fuel element.

Should you invest $1,000 in Woodside Petroleum Ltd right now?

Before you buy Woodside Petroleum Ltd shares, consider this:

Motley Fool investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Woodside Petroleum Ltd wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

And right now, Scott thinks there are 5 stocks that may be better buys…

Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

On Wednesday, the S&P/ASX 200 Index (ASX: XJO) was out of form again and dropped into the red. The benchmark index fell 0.5% to 7,715.5 points.

Will the market be able to bounce back from this on Thursday? Here are five things to watch:

ASX 200 expected to jump

The Australian share market looks set to jump on Thursday following a strong night on Wall Street. According to the latest SPI futures, the ASX 200 is expected to open the day 53 points or 0.7% higher this morning. In the United States, the Dow Jones was down 0.1%, but the S&P 500 rose 0.85% and the Nasdaq jumped 1.5%. The S&P 500 and Nasdaq indices both climbed to new record highs overnight.

Oil prices rise

ASX 200 energy shares including Beach Energy Ltd (ASX: BPT) and Woodside Energy Group Ltd (ASX: WDS) could have a good session after oil prices rebounded overnight. According to Bloomberg, the WTI crude oil price is up 0.85% to US$78.57 a barrel and the Brent crude oil price is up 0.8% to US$82.60 a barrel. Summer fuel demand optimism has given oil a boost this week.

US inflation report

Investors were celebrating on Wall Street overnight after US inflation came in softer than expected. According to CNBC, the consumer price index (CPI) showed no increase in May. This compares to expectations of a 0.1% increase according to economists surveyed by Dow Jones. Following the release of the CPI data, futures traders lifted the chances of the US Federal Reserve cutting interest rates in September. This would be the first move lower since the early days of the pandemic.

Gold price rises

It could be a positive session for ASX 200 gold miners such as Newmont Corporation (ASX: NEM) and Northern Star Resources Ltd (ASX: NST) today after the gold price pushed higher overnight. According to CNBC, the spot gold price is up 1.2% to US$2,353.9 an ounce. The precious metal rose after the US inflation report sparked hopes that interest rates could fall this year.

WiseTech rated as a hold

The WiseTech Global Ltd (ASX: WTC) share price could be almost fully valued according to analysts at Bell Potter. This morning, the broker has reaffirmed its hold rating on the logistics solutions company’s shares with an improved price target of $100.00. This implies just 3.2% upside from current levels. It said that the price target “is a modest premium to the share price so we maintain the HOLD. Potential catalysts for the stock include a beat in the FY24 result â most likely at EBITDA â and strong guidance for FY25 consistent with or ahead of consensus.”

Should you invest $1,000 in Beach Energy Limited right now?

Before you buy Beach Energy Limited shares, consider this:

Motley Fool investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Beach Energy Limited wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

And right now, Scott thinks there are 5 stocks that may be better buys…

Motley Fool contributor James Mickleboro has positions in Woodside Energy Group. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended WiseTech Global. The Motley Fool Australia has positions in and has recommended WiseTech Global. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.