From time to time, Aussie companies will decide to try their luck at opening their doors in new markets. Analysts at Sydney-based Wilsons Advisory think an ASX All Ords stock could be eyeing the United Kingdom for expansion.

Hot on the heels of a successful local acquisition, Australia’s prominent furniture retailer Nick Scali Limited (ASX: NCK) may soon look further afield for its next bolt-on business, according to Wilsons’ equity research analyst Tom Camilleri.

Nick Scali shares have rallied 62% in the last year, but could a new growth avenue pave the way to greater heights?

A bigger market beckons

Done well, acquisitions can help a company grow beyond what is possible organically. That might mean breaking into a country like the UK, which touts a population of 67 million compared to Australia’s 26 million — two and a half times the size.

Speaking with The Australian, Camilleri described the UK sofa market with three key points:

- Fragmented market with similar consumer tastes

- 19.1% less sofa spend than Australian consumers per capita; and

- Greater online penetration of 20.5% versus 13.7% in Australia

Adding further clarity, Camilleri elaborated on the benefit of branching into the UK, stating:

We believe these market nuances do not act as a barrier for Nick Scali, and can present opportunities to bring strategies back to Australia and New Zealand (with digital platforms being an example).

Wilsons’ research into the UK sofa/furniture market postulates that a weakened economy could also paint a near-term risk of insolvencies. This might create an opportunity for this ASX All Ords stock to scoop up a UK furniture business at a discount.

This brings us to the next question… what can Nick Scali afford to acquire? As of 31 December 2023, the company carried $68.3 million in cash and $71.7 million in debt.

The company’s debt-to-equity ratio reached 72% in 2021. All else being equal, Nick Scali could tap another $74.6 million worth of debt, assuming lenders are comfortable with a similarly leveraged balance sheet today.

The risk for this ASX All Ords stock

Australian corporations and international expansions have a checkered past. Who can forget Wesfarmers Ltd‘s (ASX: WES) push to take Bunnings to the UK? A move that ended in retreat and a pricey $1 billion write-down.

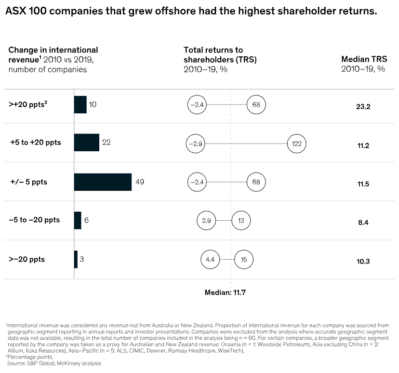

Acquisitions can also be fraught with danger. Overpaying for the acquired assets, hidden legal problems, poorly executed strategies, cultural differences — the list goes on. Yet, the team at global consultancy McKinsey challenges this default belief.

As shown above, McKinsey research indicates ASX 100 companies that experienced the largest increases in international revenue also provided the greatest shareholder returns. However, according to McKinsey, this is predicated on having the right business model.

Looking at DFS Furniture (a listed UK furniture retailer), some differences appear. Most notably, DFS generated A$2.03 billion in revenue for the 12 months ended December 2023 with only 174 stores. Meanwhile, Nick Scali operates through 108 stores and raked in $450 million, equating to:

- $11.67 million per store for DFS

- $4.17 million per store for Nick Scali

I am concerned this suggests Nick Scali is behind the ball in online sales compared to UK competitors. For this reason, I’d hold off on buying this ASX All Ords stock if it were to make a sudden UK push.

The post Would I buy this ASX All Ords stock if it flies the nest for the UK? appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 1 February 2024

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- 7 ASX small-cap shares that are cheaper than the ASX 200 in March 2024

- 3 great ASX shares I want to buy in the next bear market

- Fund manager rates these 2 undervalued ASX All Ords shares as buys

- I think they can! 3 ASX shares that can keep chugging higher

- 2 ASX companies with the firepower to raise their dividends

Motley Fool contributor Mitchell Lawler has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Wesfarmers. The Motley Fool Australia has positions in and has recommended Wesfarmers. The Motley Fool Australia has recommended Nick Scali. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Vlk51MT