The S&P/ASX 200 Index (ASX: XJO) has concluded the week’s trading on a decidedly high note. Literally. For today, the ASX 200 minted a fresh new all-time high of 7,853.1 points.

The index closed slightly below that new high watermark at 7,847 points, up an impressive 1.07% for the day.

This happiest of Fridays for the ASX comes after a strong night of trading up on Wall Street last night (our time).

The Dow Jones Industrial Average Index (DJX: .DJI) jumped up by an encouraging 0.34%.

Meanwhile, the Nasdaq Composite Index (NASDAQ: .IXIC) did even better again, galloping 1.51% higher to a new record of its own.

But let’s get back to the ASX now with a look at where the various ASX sectors finished their weeks.

Winners and losers

There were only two red sectors today, with most of the stock market leaping higher.

Missing out on the fun were gold stocks though. The All Ordinaries Gold Index (ASX: XGD) was left out in the cold, sliding 0.41%.

Also shunned were industrial shares. The S&P/ASX 200 Industrials Index (ASX: XNJ) had a flat day, slipping by 0.02%.

But that was the worst of it.

Leading the charge higher this Friday were ASX financial stocks. The S&P/ASX 200 Financials Index (ASX: XFJ) had a ball, surging by 2.03%.

Healthcare shares had a great day too, with the S&P/ASX 200 Healthcare Index (ASX: XHJ) rocketing 1.25%.

Consumer staples stocks also did well. The S&P/ASX 200 Consumer Staples Index (ASX: XSJ) jumped by 1.21% by the closing bell.

Utility shares weren’t far behind that, evidenced by the S&P/ASX 200 Utilities Index (ASX: XUJ) leaping 1.12%.

Communications shares were in demand as well. The S&P/ASX 200 Communication Services Index (ASX: XTJ) enjoyed a 1.09% lift.

Then we had ASX energy stocks. The S&P/ASX 200 Energy Index (ASX: XEJ) finished its week on a high with a gain of 1.02%.

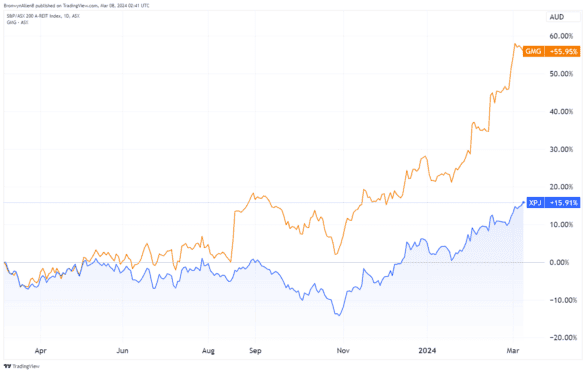

Real estate investment trusts (REITs) came next, with the S&P/ASX 200 A-REIT Index (ASX: XPJ) bouncing 0.95%.

Consumer discretionary stocks were yet another bright spot. The S&P/ASX 200 Consumer Discretionary Index (ASX: XDJ) vaulted 0.94% higher.

Tech shares came in just behind, as you can see from the S&P/ASX 200 Information Technology Index (ASX: XIJ)’s rise of 0.82%.

Finally, mining stocks had a rather tame Friday by comparison, but the S&P/ASX 200 Materials Index (ASX: XMJ) still managed a 0.12% bump.

Top 10 ASX 200 shares countdown

Coming in with a barnstorming win today was ASX bank Virgin Money UK plc (ASX: VUK). Virgin Money shares skyrocketed today, jumping by a massive 32.9% up to $4.08.

This comes after it was revealed that the London-based bank has been approached with a takeover offer worth approximately $4.26 a share.

Here’s the rest of today’s winners and how they ended the trading week:

| ASX-listed company | Share price | Price change |

| Virgin Money UK plc (ASX: VUK) | $4.08 | 32.90% |

| Life360 Inc (ASX: 360) | $12.34 | 5.83% |

| Alumina Ltd (ASX: AWC) | $1.22 | 5.17% |

| Strike Energy Ltd (ASX: STX) | $0.225 | 4.65% |

| Polynovo Ltd (ASX: PNV) | $2.39 | 4.37% |

| Paladin Energy Ltd (ASX: PDN) | $1.245 | 3.75% |

| Webjet Ltd (ASX: WEB) | $7.31 | 3.39% |

| Telix Pharmaceuticals Ltd (ASX: TLX) | $11.70 | 3.27% |

| Pro Medicus Limited (ASX: PME) | $101.25 | 2.93% |

| Star Entertainment Group Ltd (ASX: SGR) | $0.545 | 2.83% |

Our top 10 shares countdown is a recurring end-of-day summary to let you know which companies were making big moves on the day. Check in at Fool.com.au after the weekday market closes to see which stocks make the countdown.

The post Here are the top 10 ASX 200 shares today appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 1 February 2024

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- Why is this ASX 200 share rising at nearly quadruple the rate of its peers?

- Is this surging ASX 200 stock an under-the-radar buy?

- Why Judo, Paladin Energy, Virgin Money, and WA1 shares are racing higher

- Virgin Money share price pops 34% on takeover bid

- ASX 200 soars to another new all-time high on Friday!

Motley Fool contributor Sebastian Bowen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Life360, PolyNovo, Pro Medicus, and Telix Pharmaceuticals. The Motley Fool Australia has recommended Pro Medicus and Telix Pharmaceuticals. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/jNQ9szG