It’s Valentine’s Day! You know what everyone probably wants to do today? Talk about inflation! Chocolate prices recently hit all-time highs. I think that can tell us a number of things about today’s ASX share market.

Chocolate prices see an unwelcome spike

According to reporting by CNBC, cocoa prices hit an all-time high last week because of deteriorating weather conditions and disease challenges, which hurt crop production in the African countries of Ghana and the Ivory Coast.

Those two countries are responsible for almost two-thirds of global production.

Cocoa futures have reportedly jumped around 40% since the start of 2024, reaching an all-time high of US$5,874 per metric tonne.

David Branch, senior vice president at Wells Fargo Agri-Food Institute, said:

What’s really driving all of this is basically this El Nino that’s in place right now. It’s really affecting the crop.

Chocolate prices are going to be higher. Product manufacturers are just raising the margins and telling the retailers to eat it, and they have to try to sell it at a higher price.

What this tells me about the ASX share market

Firstly, I think it says that the inflation story is not completely over yet.

We heard earlier this week that the US consumer price index rose by 0.3% in January, according to CNBC, which was more than expected. It was driven by shelter prices increasing by 0.6% over the month, which made up more than two-thirds of the increase. Excluding volatile elements, the core CPI went up 0.4% for the month and 3.9% (compared to expectations of 0.3% and 3.7%, respectively). The US Federal Reserve is aiming at a target of 2% annual inflation.

With (ASX) share market investors seemingly pinning their hopes on multiple rate cuts this year, that view may end up premature. It’s possible there could be multiple cuts in Australia this year, but it’s also possible there may be no cuts at all. Remember, Australia’s interest rate is materially lower than the US, the UK, New Zealand and Canada.

Ultimately, share prices should be representative of what’s happening with a company’s profit and growth. A lot of share prices have risen over the last few months, so they need to report numbers that justify the valuation.

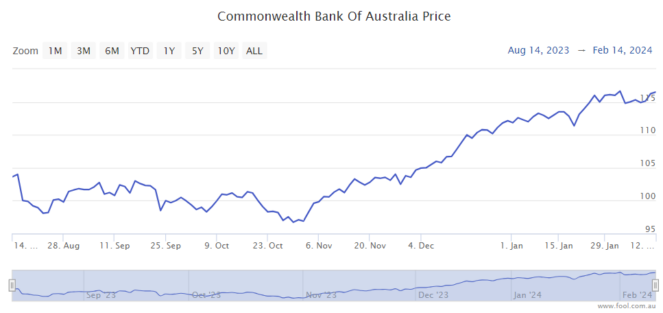

Look at what happened to Commonwealth Bank of Australia (ASX: CBA), it reported that net profit after tax (NPAT) declined amid strong competition, and that sent the CBA share price lower. Some retailers have managed to beat forecasts.

Also, remember interest rates should be influential on asset prices. We haven’t seen this RBA cash rate for a long time, yet share prices are generally at/close to all-time highs. Even a reduction of the RBA cash rate to 4% or 3.5% would mean it’s much higher than where it was in 2019.

I do think business profits (and share prices) can climb over the longer term, and I continue to see long-term opportunities in certain places. But, I also believe investors should be careful about some industries and some valuations if the aim is to beat the market’s return.

If we look carefully, there are definitely still some appealing ASX share market opportunities.

The post What all-time high chocolate prices can tell us about the ASX share market appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 10 November 2023

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- Guess which ASX 300 director just cashed in $2.3 million worth of company shares

- Are Metcash shares worth buying for that fat 6% dividend yield?

- How are Woodside shares avoiding the market selloff today?

- How price cuts on the shelves could hurt Coles shares

- I’d grow my wealth by buying these so-called ‘expensive’ ASX stocks

Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Mc4BSKt