Goldman Sachs believes that this language testing and student placement company’s shares are significantly undervalued following a recent selloff.

Its analysts have a buy rating and $27.60 price target on its shares. This implies potential upside of 43% for investors over the next 12 months.

While Goldman acknowledges that there has been a series of negative events that could impact IDP Education, it remains very positive and believes that structural tailwinds will underpin very strong medium term growth. It said:

IEL trades at 28x our 12mf EPS estimate vs 45x historically and against a +17% FY23-26E EPS CAGR. Reiterate Buy into a strong 1H result where we sit +10% ahead of VA Consensus EBIT based on a strong start to FY24E as seen in the available visa data. News flow may continue to be choppy, however IEL’s fundamental quality and structural growth drivers remain intact while the company possesses levers to continue to grow earnings (e.g. costs).

Goldman Sachs also sees major upside potential for this enterprise software provider’s shares.

It currently has a buy rating and a $4.50 price target on the ASX growth share. This implies a 12-month potential return of over 30% for investors.

Goldman likes Readytech due to its positive growth outlook and attractive valuation. It said:

We believe RDY remains undervalued compared to SaaS peers on an absolute and growth adjusted basis, trading on 11.5x FY24E EV/EBITDA vs a 19% FY23-26E EBITDA CAGR or a growth-adjusted multiple of 0.6x vs peers typically at ~1.5x.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group, Idp Education, and ReadyTech. The Motley Fool Australia has recommended Idp Education and ReadyTech. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/qGx1iWO

If I were aiming to build a bulletproof passive income stream by investing $10,000 in S&P/ASX 200 Index (ASX: XJO) dividend stocks, here’s how I’d go about it.

Sticking to ASX 200 stocks should give my portfolio less volatility than investing in small-cap shares. That in turn should help smooth out the annual passive income I can expect to land in my bank account.

Second, I’d strongly lean towards companies paying fully franked dividends. This should see me hold onto more of that dividend income at tax time.

Third, I’d invest my $10,000 across a range of companies operating across a variety of sectors. That will decrease the odds of my passive income portfolio taking a big hit if any particular sector comes under pressure.

Now, I’d also keep in mind that the yields I generally see quoted are trailing yields. Future yields may be higher or lower depending on a range of company-specific and macroeconomic factors.

However, by spreading my $10,000 across the retail, finance, energy and resources sectors, my long-term aim is to see any dip in dividends from one stock balance out by increased payouts from another.

With that said…

Four ASX 200 shares for diversified passive income

The first ASX 200 dividend stock I’d invest in for reliable passive income is home furnishings and white goods retailer Harvey Norman Holdings Ltd (ASX: HVN).

Over the past 12 months, the retail stock has delivered 25 cents a share in fully franked dividends. At Friday’s closing price of $4.65, Harvey Norman shares trade on a trailing yield of 5.38%.

The second company I’d target for passive income is financial stockAustralia and New Zealand Banking Group Ltd (ASX: ANZ).

Over the past 12 months, ANZ has paid out $1.75 a share in partly franked dividends. At Friday’s closing price of $27.68, ANZ shares trade on a trailing yield of 6.32%.

Turning to the resources sector for passive income, I’d target mining giantFortescue Ltd (ASX: FMG).

Over the past 12 months, Fortescue has paid out $1.75 a share in fully franked dividends. At Friday’s closing price of $28.26, the ASX 200 resources stock trades on a trailing yield of 6.19%.

Which brings us to the fourth company I’d invest in for a bulletproof passive income portfolio, ASX 200 oil and gas stockWoodside Energy Group Ltd (ASX: WDS).

Over the past 12 months, Woodside has paid out $3.40 in fully franked dividends. At Friday’s closing price $31.86, Woodside shares trade on a trailing yield of 10.6%.

To the maths!

To aim for that bulletproof passive income stream, I’d invest an equal amount into each of the above four companies. Or $2,500 apiece.

Based on the trailing yields, I can then expect to earn an average yield from these four ASX 200 dividend stocks of 7.1%.

This means my $10,000 investment should see me earning $710 a year in passive income, with potential tax benefits from those franking credits.

And, of course, I’ll be hoping for some share price gains as well!

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has positions in and has recommended Harvey Norman. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/MwgiTJC

It was another busy week for Australia’s top brokers. This led to the release of a large number of broker notes.

Three ASX broker buy ratings that you might want to know more about are summarised below. Here’s why brokers think these ASX shares are in the buy zone:

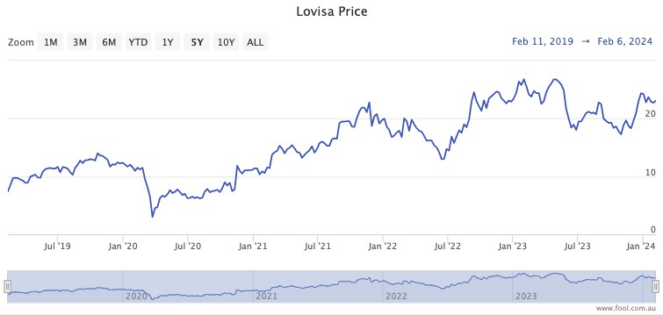

According to a note out of Bell Potter, its analysts have retained their buy rating on this fashion jewellery retailer’s shares with an improved price target of $26.50. The broker has been looking into the company’s opportunity in China following the launch of its first store at the end of 2023. Bell Potter highlights that the latest customer reviews for Lovisa from Mainland China on the dominant social media app, Xiaohongshu, have been positive. This bodes well for the company given that the market is 25 times larger than Australia. The Lovisa share price ended the week at $24.37.

A note out of Macquarie reveals that its analysts have retained their outperform rating and $9.95 price target on this energy producer’s shares. This follows news that its merger talks with Woodside EnergyGroup (ASX: WDS) have ended without a deal being reached. Macquarie isn’t fazed by the news, believing there’s still significant value in its assets that is being overlooked. In addition, it suspects that Santos may soon reinstate its buyback program. The Santos share price was fetching $7.32 on Friday.

Analysts at Morgan Stanley have retained their overweight rating and $85.00 price target on this logistics solutions company’s shares. Morgan Stanley highlights that the market is expecting a strong half year result from WiseTech this month. It suspects that if the company beats the market’s estimate of 30% revenue growth, its shares could jump. Though, it warns that softer than expected revenue growth could mean the opposite for its shares. The WiseTech share price ended the week at $77.15.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has positions in Lovisa and Woodside Energy Group. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Lovisa, Macquarie Group, and WiseTech Global. The Motley Fool Australia has positions in and has recommended Macquarie Group and WiseTech Global. The Motley Fool Australia has recommended Lovisa. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/RLNX3oE

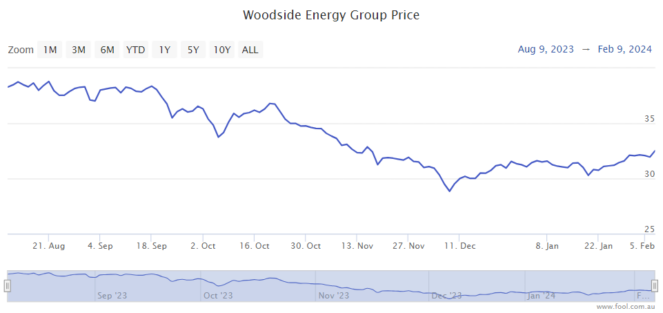

Woodside Energy Group Ltd (ASX: WDS) shares may be in line to benefit in the medium term if a compelling oil-price prediction comes to fruition.

US company Occidental Petroleum CEO Vicki Hollub told CNBC that the oil market will face a supply shortage by the end of 2025 because the world is not replacing crude oil reserves fast enough.

What does this mean for Woodside?

This could spell good news for Woodside shares. If there is less supply than demand for oil, it could push up the oil price, which may then boost Woodside’s profitability. It costs roughly the same to extract oil each month, so a boost to revenue would probably translate directly into higher net profit as well.

But, keep in mind that Woodside earns a large amount of its profit from LNG (liquified natural gas), which is a different commodity. A 10% rise in Woodside’s oil earnings won’t necessarily translate into a 10% in overall profit. In the HY23 result, crude oil and condensate made up US$1.76 billion, or 24%, of Woodside’s overall revenue from hydrocarbons.

Oil supply forecast

According to reporting by CNBC, Hollub said 97% of the oil being produced right now was discovered in the 1900s. The world has reportedly replaced less than 50% of the crude oil produced in the last decade. The CEO said:

We’re in a situation now where in a couple of years’ time we’re going to be very short on supply.

At the moment, the market is “oversupplied”, which has kept a lid on prices despite the conflict in the Middle East. Places like the United States, Brazil, Canada and Guyana have pumped record amounts of oil as demand slows amid a faltering economy in China.

Hollub thinks the supply and demand balance and outlook will “flip” by the end of 2025. She said:

The market is out of balance right now, but again, this is a short-term demand issue. But it’s going to be a long-term supply issue.

The oil-producing companies of OPEC are forecasting that global oil demand will grow by 1.8 million barrels per day in 2025 thanks to a recovery of the Chinese economy. The growth of demand is expected to beat the growth of supply of 1.3 million barrels per day by countries outside of OPEC.

Woodside share price snapshot

Over the past six months, shares in the company have fallen 16%, so it’s cheaper to invest in than it was before. Added to the prediction from the Occidental CEO, this seems to be an interesting time to be looking at Woodside shares.

And possibly lending weight to the prediction is Occidental’s links with investing legend Warren Buffett. Buffett’s company Berkshire Hathaway owns at least 28% of Occidental, so he likely holds its leadership in high regard.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Berkshire Hathaway. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended Occidental Petroleum. The Motley Fool Australia has recommended Berkshire Hathaway. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/vfyRHK2

As its name suggests, this ETF maximises the yields from the top 500 companies listed on Wall Street. This includes giants such as Apple, Exxon Mobil, Johnson & Johnson, and Walmart.

And when I say maximise, I mean it. The S&P 500 index currently trades with a dividend yield of approximately 1.5%. However, this ETF’s actively managed covered call strategy means it aims to pay out significantly more.

For example, at the last count, its units were providing investors with a 5.1% dividend yield. This means that a $20,000 investment would provide $1,020 of income.

This popular funds gives investors low-cost exposure to a diverse group of ~70 ASX shares that have higher forecast dividends relative to the market average.

Among its holdings are big miners and banks, such as BHP Group Ltd (ASX: BHP) and Commonwealth Bank of Australia (ASX: CBA), as well as smaller names like Metcash Limited (ASX: MTS) and Eagers Automotive Ltd (ASX: APE).

At present, the ETF currently trades with a trailing dividend yield of 5.1%. This would also generate $1,020 of income from a $20,000 investment.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Apple and Walmart. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended Johnson & Johnson. The Motley Fool Australia has positions in and/or has recommended BetaShares S&P 500 Yield Maximiser Fund, Metcash, and Eagers Automotive. The Motley Fool Australia has recommended Apple and Vanguard Australian Shares High Yield ETF. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/ba5H4Gn

The team at Bell Potter is feeling positive about Accent Group. It is the footwear retailer behind brands such as The Athlete’s Foot, HYPEDC, and Sneaker Lab. Bell Potter currently has a buy rating and $2.50 price target on its shares.

As for those all-important dividends, Bell Potter is forecasting fully franked dividends per share of 12 cents in FY 2024 and then 14.1 cents in FY 2025. Based on the Accent share price of $2.12, this represents dividend yields of 5.7% and 6.65%, respectively.

Goldman Sachs thinks investors should be buying this packaging company. It likes Orora due to its defensive qualities and positive growth outlook. The broker has a buy rating and $3.50 price target on its shares.

In respect to income, the broker has pencilled in dividends per share of 14 cents in FY 2024, 15 cents in FY 2025, and 16 cents in FY 2026. Based on the current Orora share price of $2.84, this will mean yields of 4.9%, 5.2%, and 5.6%, respectively.

This agricultural property company could be an ASX dividend share to buy according to analysts at Bell Potter. The broker currently has a buy rating and $2.40 price target on its shares.

As for dividends, Bell Potter is forecasting dividends per share of 11.7 cents in both FY 2024 and FY 2025. Based on the current Rural Funds share price of $2.22, this will mean yields of 5.3% for investors.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has positions in and has recommended Rural Funds Group. The Motley Fool Australia has recommended Accent Group and Orora. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/8bxu0Io

Regular readers would know that there are many ways to reach the magic million using the power of ASX shares and compounding.

However, what you’re really wanting to know is which stocks will take you there.

One stock that many experts are bullish on is low-cost jewellery retailer Lovisa Holdings Ltd (ASX: LOV).

Let’s examine whether Lovisa shares have the chops to take you to seven figures:

What does Lovisa do?

Lovisa operates a network of “fast fashion” jewellery shops both in Australia and overseas.

Although the business started in Sydney, its stores can now be seen in places as far-flung as Hong Kong, Namibia, France, the US, the UAE, and Colombia.

The retail chain has a presence in 40 countries via 830+ stores, according to the last quarterly update.

How is the business going?

Although it’s definitely a consumer discretionary stock, Lovisa has withstood the recent economic downturn better than some others because of its low-cost niche.

Its target demographic also skews to younger generations, who are less likely to be under pressure from higher mortgage repayments.

The company is also on an expansion tear, with its first store openings in China and Vietnam imminent. They are both countries that have a fast-growing middle class market.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tony Yoo has positions in Lovisa. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Lovisa. The Motley Fool Australia has recommended Lovisa. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/rfnPe6H

It’s well known that Australians between the ages of 30 and 50 don’t exactly pay as much attention to their superannuation balances as those who are closer to the traditional retirement age.

On one hand, that’s fair enough. If you’re 30 years old, retirement probably seems like a distant pipedream. Certainly not something that’s worthy of as much thought as career advancement.

But I would argue that we should all be paying our super funds some attention every once in a while, regardless of our age. Superannuation is our best shot at a comfortable, self-funded retirement, after all. And thanks to the power of compounding, the earlier we show it some love, the better off we’ll be.

But today, we’re going to check out how those numbers look for Australians aged 30, 40 and 50. It might be worth seeing how your own super fund measures up to what the average person in your age group has.

What’s the average superannuation balance at 30, 40 and 50?

According to the ATO’s data, the median super balance for Australians aged between 30 and 34 in FY21 was $38,681. That compares to an average balance of $51,400. Remember, the average statistic is more heavily influenced by outsized numbers than the median.

For someone between the ages of 40 and 44, the median balance was $91,590. That was with an average superannuation balance of $123,993.

For Australians aged between 50 and 54, we get a median figure of $137,930 and an average balance of $215,115.

These figures might not mean too much to someone who’s 30 or perhaps even 40 right now. But it’s well worth checking out how your own superannuation fund compares to these average and median figures.

As we covered last year, AMP has estimated the amount that a single retiree (who already owns their own home outright) will need in their superannuation nest egg to fund a comfortable retirement. Those analysts came up with a figure of $1.25 million in today’s dollars. It was a lump sum of $795,000 to pay for even a modest retirement.

If you plug in the numbers for your own fund, you might find that your super balance could need a boost. That’s if you’re hoping to get to that rainbow’s end at the conclusion of your working life.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Sebastian Bowen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/NMr0tjm

Young Australians just starting their investment journeys are making some similar decisions, data shows.

Shares vs. property is typically the first big decision any budding investor has to make.

Of course, there are other options like simple savings accounts and bonds, but most people think of shares and property first when contemplating long-term investment for retirement.

There are lots of factors to consider in the choice of shares vs. property, but the overarching one is quite simple. Can you get enough finance to buy what you want?

Interest rates on investment property loans are at about 6%. Then the banks add a 3% ‘mortgage serviceability buffer’, as directed by APRA, to assess your long-term ability to keep up with repayments.

Being assessed at 9% makes it very hard for younger Australians to get a loan big enough for a property purchase. After all, the Australian median home value is just over three-quarters of a million dollars.

So, the affordability of property itself coupled with the difficulties of getting enough finance are big issues for beginner investors preferring bricks and mortar to shares.

But as always, the free market finds ways to adapt when challenges arise.

Shares vs. property: The path to investment

Most beginner investors can buy ASX shares tomorrow. All they need is an online broking account and a minimum of $500 in savings to make that first trade through any of the big banks.

Property is harder.

Historically, the traditional path to property investment started later in life, after first home ownership.

Back in the 1970s and 80s, most Aussies aspired to own a family home on a quarter-acre block. That was the Great Australian Dream. Then later down the track, some of those homeowners would use the equity in their residences to fund a single property investment for their retirement. That was the ‘ideal’ realised.

But over the years, the Great Australian Dream became difficult to afford. As the population grew, home prices rose more rapidly in the desirable inner city suburbs closest to work in the CBD.

So young Gen X Australians began buying further away, which led to the dawn of the commuter lifestyle. Those young families reasoned that owning a home outweighed the inconvenience of long travel to work. But eventually, those properties on the outskirts also became hard to afford, as land values shot up.

So, young people went back to the inner city and bought apartments instead. The dream of a quarter acre was lost, but home ownership remained the priority, with investment to come later in life as it always had.

Then those inner city units became expensive.

So, the next generation — the millennials — came up with a new idea. They changed the Great Australian Dream from home ownership to property ownership, with investment coming first, ahead of ownership.

That spawned a new market trend: Rentvesting.

What is rentvesting?

Rentvesting is where a young person rents where they want to live — typically a trendy inner city lifestyle area where they can’t afford to buy — and purchases an investment property wherever they can afford it.

The rent helps them pay the mortgage, and they hope for enough capital growth over time to fund a deposit on a home in a location where they actually want to live themselves, later down the track.

This choice is facilitated by it being easier to get an investment loan than a home loan. This is because the property’s rental income counts as part of the bank’s serviceability and income assessment of you.

Rentvesting has become such a significant trend that in 2019, the Australian Bureau of Statistics (ABS) began separately reporting the number of new loans going to first-time buyers purchasing for investment as opposed to owner-occupation.

Last year, 7,412 young Australians took out loans to rentvest, according to ABS lending finance data.

In 2022, it was 8,243. In 2021, it was 10,678.

That decline over recent years may be the result of interest rates rapidly increasing since May 2022.

Are more beginner investors choosing shares vs. property?

The rapid growth in property values over the past 20 years could be a factor in data that indicates more beginner investors may be choosing shares vs. property.

According to the 2023 ASX Australian Investor Study, 32% of 18 to 24-year-old investors own investment property vs. 43% who own ASX shares. Some may own both, but you see the difference.

Among 25 to 49-year-old investors, 42% own investment property vs. 52% who own ASX shares.

Which ASX shares do beginner investors like most?

ASX shares are the most popular category of stocks among both age groups.

ASX ETF provider BetaShares says investors funnelled $15 billion net into ETFs last year. This, along with gains in asset values, led to the highest increase in annual funds under management (FUM) within the Australian ETF industry, ever.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bronwyn Allen has positions in Core Lithium, Vanguard Australian Shares Index ETF, and Vanguard Diversified High Growth Index ETF. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended BetaShares Nasdaq 100 ETF and iShares S&P 500 ETF. The Motley Fool Australia has positions in and has recommended BetaShares Nasdaq 100 ETF. The Motley Fool Australia has recommended Vanguard Msci Index International Shares ETF and iShares S&P 500 ETF. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/esJDfnU

When it comes to ASX dividend shares, it’s typically the stocks offering the highest fully-franked yields that get the most attention.

That’s why most investors will name the likes of Westpac Banking Corp (ASX: WBC) and BHP Group Ltd (ASX: WDS) when asked which ASX dividend shares they like rather than something like WiseTech Global Ltd (ASX: WTC) or Washington H. Soul Pattinson and Co Ltd (ASX: SOL).

Sure, there is something to be said of the massive and immediate flow of passive income when buying a high-yielding share. But are consistent high-paying ASX dividend shares better than those with small dividend payments but that grow them over time?

ASX dividend shares: growth vs. consistency

I think this question comes down to your personal circumstances and preferences. For older investors who have perhaps retired, cash flow and franking credits are usually the most important considerations when selecting income-paying shares, with capital growth and maximising returns playing second fiddle.

As such, it might make more sense to target those consistently high-yielding ASX dividend shares like Westpac or BHP if you fall into that category.

After all, if you’re in your 70s or 80s, there’s arguably less incentive to buy low-yielding ASX dividend shares that might have a massive yield in 20 years’ time.

However, that’s not the approach I’m taking with my own portfolio. Since I’m still many years away from retirement, maximising my overall returns is a far more pressing goal than maximising dividend cash flow.

Looking at the share prices of some of the ASX’s most prolific dividend payers, it’s clear that many of these companies sacrifice growth opportunities in order to keep their dividends at the highest levels possible.

Westpac? You can buy this ASX bank’s shares today for the same price as you could way back in April 2006. Sure, It’s got a 5.85% fully franked dividend yield at present. But you don’t get too much more than that.

It’s a similar story with BHP. Today, investors who picked up BHP shares at the height of the 2008 mining boom can sell them back without taking much in the way of gains.

High dividend payments have a price.

Income growth comes with share price growth too

I much prefer the likes of Washington H. Soul Pattinson. Soul Patts shares may only offer a dividend yield of 2.58% today. But, as we discussed just yesterday, someone who invested in this prolific dividend grower would have grown their dividend yield on cost from 2.67% up to 22.3%.

That’s the position that I think is most conducive to long-term returns. Remember, if an ASX dividend share is consistently growing its profits, it will be able to raise its shareholder payouts over time.

This usually walks hand in hand with the price rises too. Over the 23 years that Soul Patts has hiked its annual dividend from 10.4 cents to 87 cents, its share price has also grown by more than 765%.

Another ASX dividend share I’d consider for growing dividends, and a potentially high future yield on cost is Wisetech Global.

This tech stock first started paying dividends in 2017. That year, investors enjoyed a total of 2.2 cents per share in payouts. But in 2023, Wisetech doled out a total of 15 cents per share.

Yet despite this huge ramp-up in raw dividends going to shareholders, its yield still looks pitiful today at 0.2%. But bear in mind this is because the WiseTech share price has also ballooned 10-fold since 2017.

If it’s between WiseTech and Westpac, between BHP and Soul Patts, I’m going to take the ASX dividend share grower any day of the week.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Sebastian Bowen has positions in Washington H. Soul Pattinson and Company Limited. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Washington H. Soul Pattinson and Company Limited and WiseTech Global. The Motley Fool Australia has positions in and has recommended Washington H. Soul Pattinson and Company Limited and WiseTech Global. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/wXIY0ro