When it comes to investing, you don’t have to start with big lump sums to build your wealth.

Particularly now there are investment platforms out there that allow you to invest small amounts or even your spare change into the share market.

In fact, if you were to give up a coffee a day and put $5 into ASX shares, you could generate big returns and even a second income over the long term.

$5 a day into ASX shares

Over the long term, the Australian share market has generated an average return of approximately 10% per annum.

It has been possible to beat this return by investing in ASX shares with strong business models, positive long-term growth outlooks, and competitive advantages. Just look at Warren Buffett’s track record at Berkshire Hathaway (NYSE: BRK.B) to see this.

But for the purpose of this article, we’re going to assume that you match the market return rather than beat it.

With that in mind, let’s see what you happen if you were to invest $5 a day into ASX shares.

Firstly, $5 a day equates to an investment of approximately $152 per month on average throughout the year.

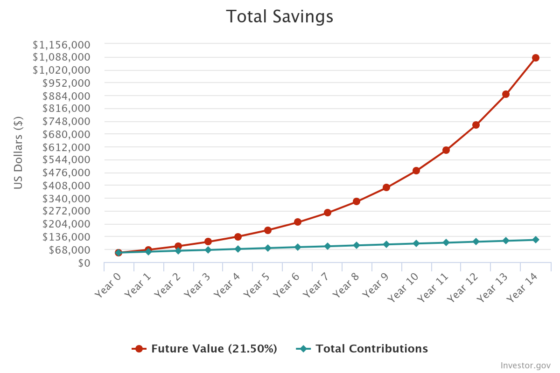

If you put this amount into ASX shares for 10 years and earned an average 10% per annum return, you would have grown your portfolio to just over $30,000.

And thanks to compounding, if you were to keep going, you would grow your investment portfolio to $110,000 after a total of 20 years and over $315,000 at the 30-year mark.

Making a second income

Once you’ve built up your investment portfolio, you can start thinking about a second income.

For example, if you were able to average a 6% dividend yield across your portfolio, your annual income would be as follows based on the above amounts:

- $30,000 â $1,800 of income

- $110,000 â $6,600 of income

- $315,000 â $18,900 of income

All in all, I believe this demonstrates that by coming up with a long-term investment plan, even with small contributions, it can lead to significant wealth in the future.

The post My $5 a day ASX second income plan for 2024 appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 10 November 2023

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- How to apply a Warren Buffett investing style in 2024

- With no savings at 50, I’d follow Warren Buffett’s approach to build wealth

- How I’d aim to turn $10k into $1 million with ASX shares

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Berkshire Hathaway. The Motley Fool Australia has recommended Berkshire Hathaway. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/8lhpdaJ