If you want to strengthen your income portfolio this month with some new additions, then it could be worth looking at the ASX dividend shares named below.

The team at Citi think that Charter Hall Retail REIT could be a good option for income investors. It is a supermarket anchored neighbourhood and sub-regional shopping centre markets-focused property company.

Citi currently has a buy rating and $4.00 price target on its shares.

As for income, the broker is forecasting dividends of 28 cents per share in both FY 2024 and FY 2025. Based on the current Charter Hall Retail REIT share price of $3.58, this will mean huge yields of 7.8%.

Over at Morgans, its analysts think that Dexus Industria could be an ASX dividend share to buy.

It is a real estate investment trust that primarily invests in high quality industrial warehouses located across Sydney, Melbourne, Brisbane, Perth and Adelaide.

Morgans currently has an add rating and $3.18 price target on its shares.

In respect to dividends, the broker expects dividends per share of 16.4 cents in FY 2024 and 16.6 cents in FY 2025. Based on the current Dexus Industria share price of $3.07, this will mean dividend yields of 5.3% and 5.4%, respectively.

Finally, Goldman Sachs thinks this drinks giant could be another ASX dividend share to buy next week.

Its analysts have a buy rating and $6.20 price target on the BWS and Dan Murphy’s owner’s shares.

As for dividends, the broker is forecasting fully franked dividends per share of 22 cents in both FY 2024 and FY 2025. Based on the current Endeavour share price of $5.24, this represents attractive dividend yields of 4.2% for investors.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Citigroup is an advertising partner of The Ascent, a Motley Fool company. Motley Fool contributor James Mickleboro has positions in Endeavour Group. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/xarBJNf

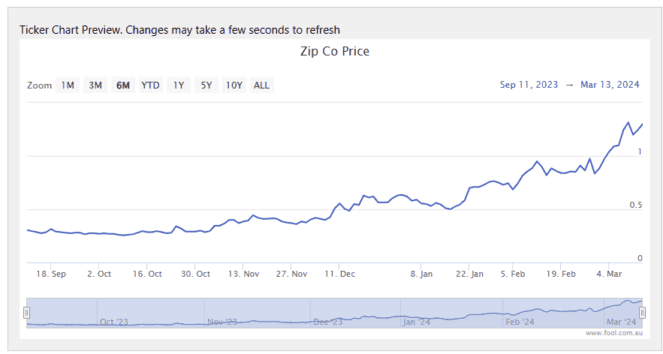

I didn’t buy Zip Co Ltd (ASX: ZIP) shares on 9 October.

But I sure wish I had.

Shares in the All Ordinaries Index (ASX: XAO)buy now, pay later (BNPL) stock have taken off over the past six months.

Here’s what’s been boosting ASX investor sentiment.

Zip shares have been rocketing

Although Zip shares remain well down from their February 2021 highs, the stock has enjoyed a remarkable rebound over the past six months.

Stock markets are often said to be forward-looking.

And while the market doesn’t always get it right, in the case of Zip shares, the steady march higher that began in October looks prescient.

Zip’s half-year results for the six months to 31 December showed increased customer engagement and boosted revenues.

Total transaction volume (TTV) for the half-year increased by 9.6% from the prior corresponding half-year to $5 billion, with TTV in Zip Americas notching a record half-year after growing by 33.3%.

Cash profits were up 45.9% year on year to $176 million. And the company’s revenue margin of 8.5% was up 1.30% year on year.

Zip CEO Cynthia Scott also painted an optimistic picture for Zip shares for the year ahead.

“We remain firmly focused on our three strategic pillars for FY24 â driving sustainable, profitable growth, product innovation and operational excellence,” she said.

Scott added, “Zip is very well-positioned to capitalise on the near and medium-term opportunities in our core markets of ANZ and the Americas and deliver greater value for our customers and merchants.”

And boom!

Now, the day before those half-year results were released on 27 February, Zip shares were already trading for 94 cents apiece.

But if I’d bought shares on 9 October, less than six months ago, I could have picked them up for 25.5 cents apiece.

Meaning my $5,000 would have netted me 19,607 Zip shares and some pocket change.

At market close on Friday, the ASX 200 BNPL stock was trading for $1.25 a share.

So, my $5,000 investment would be worth an enviable $24,508.75 today!

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Zip Co. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/04L3u6c

On Friday, a bunch of ASX REITS hit new 52-week highs, including Scentre Group (ASX: SCG) shares at $3.34 and Stockland Corporation Ltd (ASX: SGP) shares at $4.85.

Centuria Industrial REIT (ASX: CIP) shares also rose to a new annual peak of $3.59 per share.

ASX 200 market sector snapshot

Here’s how the 11 market sectors stacked up last week, according to CommSec data.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bronwyn Allen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has positions in and has recommended Apa Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/xEOKr0U

Notwithstanding Friday’s nasty dip of 0.56%, the S&P/ASX 200 Index (ASX: XJO) is sitting just 182.8 points shy of its all-time high right now. Therefore, finding cheap ASX shares to snap up can be a tough ask!

But our Foolish writers, who live and breathe the Aussie share market, are always up for a stock-picking challenge.

So, we asked them to pop their bargain-hunting hats on and let us know which ASX shares they reckon have been unfairly sold off and now represent top buying for investors in March.

Here is what they told us:

5 cheap ASX shares for March 2024 (smallest to largest)

Why our Foolish writers think these ASX stocks are bargain buys

Adairs Ltd

What it does: Adairs is an ASX 200 retail share and a brand you’ve probably seen in your local shopping centre. It sells linens, bedding, towels, furniture, and other homewares.

By Sebastian Bowen: Adairs is a company I’ve been tracking for the past few months with delight. Fresh off the lows we saw last year, investors have enjoyed some pleasing gains since November. However, the retailer is still well off its all-time highs of almost $5 a share we saw in 2021.

I think Adairs has what it takes to get back to its former glory. The company’s finances are steadying, and dividends have resumed. I’m also encouraged by the recent management shakeup.

I wouldn’t be surprised to see the Adairs share price with a ‘$3’ at the front by the end of 2024.

Motley Fool contributor Sebastian Bowen owns shares of Adairs Ltd.

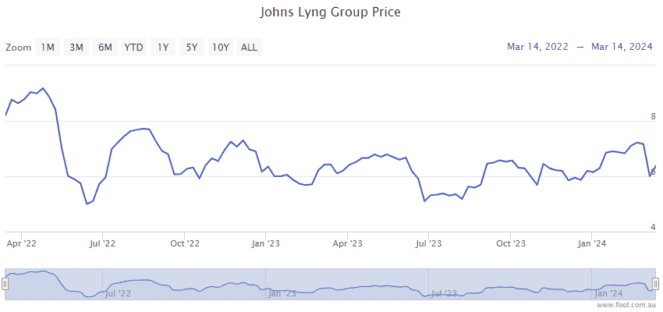

Johns Lyng Group Ltd

What it does: Johns Lyng provides construction and repair services, with work coming from insurance claims a major part of its business.

By Tony Yoo: The Johns Lyng share price has dipped around 13% since 26 February, and 32% if you go back to April 2022.

This might present an excellent buying window for a quality company that’s demonstrated an ability to grow and execute. Moreover, the nature of the business means it receives more work as extreme weather events become more frequent due to climate change.

The company’s future outlook has major backing from the professional community, with nine out of 11 analysts currently surveyed on CMC Invest rating Johns Lyng as a buy.

Motley Fool contributor Tony Yoo owns shares of Johns Lyng Group Ltd.

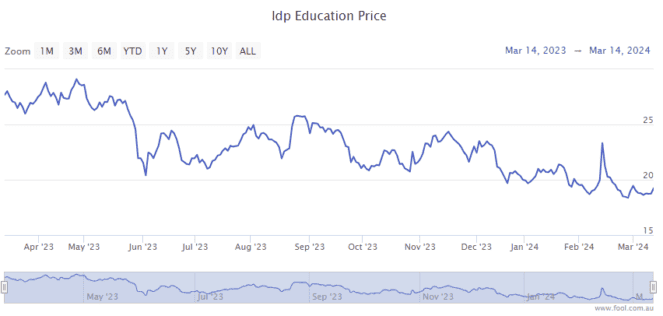

IDP Education Ltd

What it does: IDP Education is a leading provider of international student placement services and high-stakes English language testing services.

By James Mickleboro: Due to concerns over student visa changes in a number of markets and the loss of its language testing monopoly in Canada, investors have been scrambling to the exits over the last 12 months. This has led to the IDP Education share price shedding around 30% of its value during this time.

I believe this presents a buying opportunity for investors, particularly given I’m confident the company will continue its strong growth in the coming years despite these challenges.

Goldman Sachs also believes this will be the case. For example, it is forecasting earnings before interest, taxes, depreciation, and amortisation (EBITDA) of $322 million in FY 2024, $352 million in FY 2025, and $404 million in FY 2026. Goldman has a buy rating and a $26.60 price target on IDP Education shares.

Motley Fool contributor James Mickleboro does not own shares of IDP Education Ltd.

Telstra Group Ltd

What it does: Telstra is the largest telecommunications business in Australia, with a leading market share in the mobile space of the market.

By Tristan Harrison:The Telstra share price has gone backwards in recent months, but the company’s profit has been increasing. This means the price/earnings (p/e) ratio is now lower and more appealing.

I think any business that is sustainably growing its profit could present an interesting investment opportunity. Telstra is benefitting from more subscribers and a higher average revenue per user (ARPU) because of price hikes. Furthermore, the company is keeping underlying cost growth to a minimum, despite the headwinds of inflation. That combination is helping profit growth.

In FY25, Telstra is predicted (according to Commsec) to pay an annual dividend of 19 cents per share, which represents a grossed-up dividend yield of 7.1% on current pricing.

I think profit can keep rising with more subscribers, diversifying earnings (eg. Digicel Pacific, digital health and cybersecurity), and a growing number of households using 5G-powered home internet (rather than the NBN).

Motley Fool contributor Tristan Harrison does not own shares of Telstra Group Ltd.

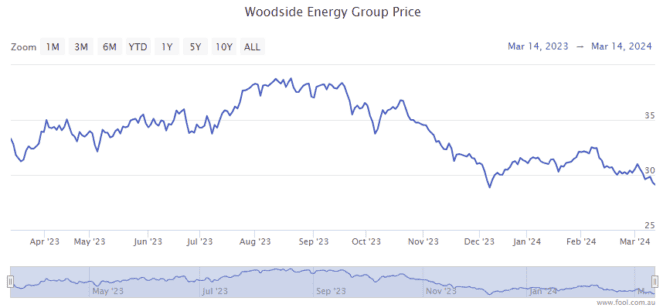

Woodside Energy Group Ltd

What it does: Woodside is Australia’s largest independent dedicated oil and gas producer. The company has a portfolio of high-quality energy assets in Australia, the Gulf of Mexico, the Caribbean, Senegal, and Timor-Leste. Woodside continues to actively explore for new oil and gas deposits.

By Bernd Struben: The Woodside share price is down by around 22% in the last six months. Much of that selling pressure came amid a retrace in global oil and gas prices, with Brent crude now trading for US$82 per barrel.

But with global demand forecast for modest growth and OPEC+ sticking with production cuts, the US Energy Information Administration forecasts oil will top US$88 per barrel this quarter and average US$87 over 2024. The EIA also expects LNG prices to be higher than in 2023.

And with Woodside’s offshore Scarborough LNG project on track for first production in 2026, the longer-term outlook also looks solid.

Atop potential share price gains, Woodside shares trade on a fully-franked dividend yield of 7.3%.

Motley Fool contributor Bernd Struben does not own shares of Woodside Energy Group Ltd.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Adairs, Goldman Sachs Group, Idp Education, and Johns Lyng Group. The Motley Fool Australia has positions in and has recommended Adairs and Telstra Group. The Motley Fool Australia has recommended Idp Education and Johns Lyng Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/UiRwneV

If you want to take your portfolio to the next level with some big gains, then it could be worth getting better acquainted with the ASX shares listed below.

That’s because they have been named as buys and tipped to rise 20% to 50% from current levels. Here’s what you need to know:

This diversified food company’s shares could be undervalued according to analysts at Bell Potter.

The broker believes that the market is not appreciating the impact that forecast farmgate prices could have on its costs. Its analysts feel it could be “a game changer” and reduce Bega Cheese’s milk costs by $55 million to $60 million.

Bell Potter currently has a buy rating and $5.00 price target on its shares. This implies potential upside of 23% for investors over the next 12 months.

Another ASX share that could offer big returns for investors is Corporate Travel Management. It is a corporate travel management and technology company with a global footprint.

The team at UBS believes that a recent selloff has created a buying opportunity for investors. Particularly given its belief that the company can grow at a strong rate over the coming years despite its shaky performance during the first half.

UBS has a buy rating and $21.80 price target on its shares. Based on the current share price of $17.00, this implies a potential upside of almost 30%.

Finally, the team at Bell Potter also sees huge returns on offer with this ASX lithium share.

The broker believes that the Kathleen Valley Lithium Project is highly strategic in terms of its stage of development, long mine life, and location. As a result, it was pleased to see the near-term funding overhang reduced last week with the announcement of a $550 million senior secured syndicated debt facility.

In response, the broker has reaffirmed its speculative buy rating and lifted its price target to $1.90. Based on the current Liontown share price of $1.25, this implies potential upside of 52% for investors between now and this time next year.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Corporate Travel Management. The Motley Fool Australia has recommended Corporate Travel Management. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/irWtbAd

I’m a big fan of buy and hold investing and believe it is one of the best ways to grow your wealth.

To demonstrate just how successful this investment strategy can be with ASX 200 shares, I like to see how much a single $20,000 investment in certain ASX 200 shares 10 years ago would be worth today.

Let’s see how investments in these shares have fared during this time:

The first ASX 200 share that we’re going to look at is Breville. It is one of the world’s leading appliance manufacturers.

Thanks to its investment in research and development, global expansion, and acquisitions, Breville has delivered strong sales and earnings growth over the last decade. This has unsurprisingly led to market-beating returns for its shares over the same period.

Over the last 10 years, Breville’s shares have achieved an average total return of 12.95% per annum. This would have turned a $20,000 investment into almost $68,000 today.

Goodman is another ASX 200 share that has made its shareholders smile.

Thanks to its strategy of investing in and developing high quality industrial properties in strategic locations close to large urban populations and in and around major gateway cities globally, Goodman has delivered consistently strong earnings growth.

This has led to Goodman’s shares generating a total average return of 22% per annum since 2014. This would have turned a $20,000 investment into ~$146,000.

Finally, a third market-beater has been data centre operator NextDC.

Due to strong demand for capacity in its world-class centres thanks to the structural shift to the cloud, its revenue and operating earnings have been growing at a rapid rate.

This has helped underpin some very strong returns since 2014. For example, over the last decade, its shares have generated an average return of 24% per annum. This means that a $20,000 investment in NextDC shares would have grown to be worth ~$170,000 today.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has positions in Nextdc. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goodman Group. The Motley Fool Australia has recommended Goodman Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/rLRPnfz

Do you have room in your income portfolio for some new ASX dividend shares? If you do, then it could be worth checking out the buy-rated shares listed below.

Both have been named as buys and tipped to provide investors with above-average dividend yields in the near term. Here’s what you can expect from them:

A recent note out of Ord Minnett reveals that that its analysts are positive on this banking giant and see it as an ASX dividend share to buy right now.

The broker was pleased to see that its proposed acquisition of Suncorp Bank is getting closer to completion. Its analysts expect the addition of the business to add scale to areas where the ANZ currently trails the rest of the big four banks.

As for that all-important income, Ord Minnett is forecasting fully franked dividends per share of $1.62 in FY 2024 and then $1.65 per share in FY 2025. Based on the current ANZ share price of $28.69, this will mean dividend yields of 5.65% and 5.75%, respectively.

The broker currently has a buy rating and $31.00 price target on ANZ’s shares.

Over at Goldman Sachs, its analysts are feeling bullish about this retail conglomerate and believe it could be another ASX dividend shares to buy.

As a reminder, Super Retail is the name behind the BCF, Macpac, Rebel, and Super Cheap Auto brands.

Goldman was pleased with its half year results, noting that it “was high quality and the strategic growth plan is intact.” This is important given that the latter is “core to [the broker’s] Buy thesis.”

In respect to dividends, the broker is forecasting fully franked dividends per share of 67 cents in FY 2024 and then 73 cents in FY 2025. Based on the latest Super Retail share price of $15.05, this will mean good yields of 4.5% and 4.9%, respectively.

Goldman Sachs has a buy rating and $17.80 price target on its shares.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has positions in and has recommended Super Retail Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/x4r9qvY

ResMed Inc (ASX: RMD) stock closed at $29.15 on Friday, up 0.59% for the day.

The sleep apnoea device maker has had a tumultuous time on the ASX boards over the past nine months.

As the chart shows below, ResMed stock experienced a significant sell-off in the second half of 2023.

The ASX 200 healthcare stalwart fell from $33.85 on 3 August to a four-year low of $21.14 on 13 October.

What caused the ResMed stock tumble?

The tumble was primarily caused by two things.

Firstly, a broader sell-off in ASX healthcare stocks, which commenced in June 2023.

Secondly, investors’ concerns over GLP-1 obesity drugs like Ozempic.

Their fear was that the highly effective weight loss medicines would lower demand for sleep apnoea devices given obesity is a common precursor to sleep apnoea.

During the height of this sell-off in October, ResMed CEO Mick Farrell sought to reassure investors.

He reminded them that the sleep apnoea market was huge and that not all sufferers have obesity.

He also told shares investors that RedMed was proactively tracking the potential future impact of Ozempic and GLP-1 medicines on the business, and even dared to quantify it.

Based on internal modelling, Farrell said GLP-1s may reduce the total addressable market (TAM) for sleep apnoea and ResMed’s products from 1.4 billion to 1.2 billion by 2050.

So, the company reckoned GLP-1s could cost them 200 million people in terms of TAM.

But at that stage, he said they were not seeing any declining use of ResMed products among patients using both GLP-1s to treat their obesity and ResMed’s devices to treat their sleep apnoea.

He pointed out that ResMed had 22.5 million customers using its devices at that time, which was a drop in the ocean of a 1.2 billion TAM.

Farrell said the company would continue to monitor the impact of GLP-1s, and we got another update when the last set of results was released in January.

And guess what?

Surprise! GLP-1s increase the use of ResMed devices

Farrell surprised analysts during their call by revealing that ResMed’s research was revealing a positive impact from GLP-1s.

The CEO said:

Our analysis of over 529,000 patients with GLP-1 prescriptions shows that not only is there not a reduction in the propensity to start positive airway pressure therapy, it is the exact opposite.

For patients who have been prescribed a GLP-1, there is an increase of 10% of the absolute percentage of patients that commence positive airway pressure therapy.

Farrell said another investor fear had been that patients on both therapies would quit their sleep devices use at a higher rate than the general population over time.

He said:

The real world data, again, with a cohort of over 0.5 million patients shows the exact opposite.

At … 12 months after therapy commencement on PAP, the delta from general PAP population to a PAP plus GLP-1 prescribed population shows an increase in the resupply rate of 300 basis points.

This delta actually increases over time going further with the delta from the general PAP population receiving resupply at 12 months being 500 basis points higher for a population prescribed both PAP and GLP-1s.

ResMed stock price recovery

ResMed stock began an impressive recovery during the Santa Rally that began in November 2023.

Since 1 November, the ASX 200 healthcare stock has rebounded by 34%.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bronwyn Allen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended ResMed. The Motley Fool Australia has positions in and has recommended ResMed. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/x1vXy8i

BHP Group Ltd (ASX: BHP) shares have come under pressure this month due to a pullback in the iron ore price.

So much so, the mining giant’s shares are down almost 17% from the 52-week high they reached at the very end of December.

While this is disappointing for shareholders, it could be a buying opportunity for the rest of us.

This is particularly the case for passive income investors given that this weakness has boosted the potential dividend yield on offer with its shares.

Generating passive income from BHP shares

As a reminder, BHP released its half-year results last month and reported a 6% increase in revenue to US$27.2 billion and flat underlying earnings of US$6.6 billion.

This allowed the BHP board to declare a fully franked interim dividend of 72 US cents per share (A$1.10 per share) for the period.

Unfortunately, the company’s shares have already traded ex-dividend for this payout. As a result, the rights to the dividend are now settled and buying BHP’s shares won’t lead to you receiving it on pay day on 28 March.

But never fear, there are plenty more dividends to come to earn passive income from. So, what would $10,000 earn investors?

Firstly, if I were to invest $10,000 (and an additional $8.76) into the Big Australian, I would end up owning 236 shares.

According to a note out of Citi from last week, its analysts are forecasting a $2.55 per share dividend in FY 2024. This will mean a fully franked final dividend of approximately $1.45 per share.

From that dividend alone, my 236 shares would produce passive income of $342.20.

Looking ahead, Citi then expects a 3.5% increase in the BHP dividend to $2.64 per share in FY 2025. If this proves accurate, my 236 shares would generate income of $623.04.

In total, that’s $965.24 of passive income from my $10,000 investment.

Don’t forget the gains

It is also worth noting that Citi upgraded BHP’s shares to a buy rating with a $46.00 price target last week.

If the BHP share price were to rise to that level, my 236 shares would have a market value of $10,856.

That means a total return on investment of $1,821.24 could be on the cards between now and the payment of BHP’s final dividend of FY 2025.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Citigroup is an advertising partner of The Ascent, a Motley Fool company. Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/vlVwUZ9

Next week will be a big one for homeowners and borrowers. That’s because the Reserve Bank of Australia (RBA) will be meeting for the second time in 2024 to decide on interest rates.

In case you’re wondering, the central bank traditionally meets on the first Tuesday of the month. However, starting in 2024, the RBA has reduced the number of meetings from 11 to just 8.

As part of this change, it will now be meeting on the first Tuesday in February, May, August, and November, and then during the second to last week of each quarter (March, June, September, and December).

So, with a meeting coming on Tuesday and inflation recently showing signs of slowing, could interest rates be heading lower next week?

Let’s see what the economics team at Westpac Banking Corp (ASX: WBC) are expecting the RBA to do at the meeting.

Will the RBA cut interest rates next week?

According to the latest weekly economic report from Westpac, its team are not expecting the RBA to make any changes to interest rates next week.

In fact, its chief economist, Luci Ellis, believes that rates are staying on hold at 4.35% until September. At that point, Ellis is forecasting a 25 basis points cut to 4.1%. She said:

Next week, the RBA Board will meet to discuss recent economic data, including the Q4 National Accounts and Wage Price Index, to decide whether it warrants a shift in policy. Our view is that the RBA will be comforted by recent developments, given the Board’s aim to bring demand back into line with supply and ensure inflation continues to trend toward and then into the target range. We continue to expect the RBA to remain on hold until September at which time they should have enough confidence in the inflation outlook to slowly begin easing policy.

The good news for borrowers is that it may not take long for further easing after that first cut. Ellis is forecasting a series of cuts to take interest rates down to 3.1% by September 2025.

So, while next week might be disappointing for homeowners, it does appear that relief is on the way.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has positions in Westpac Banking Corporation. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/P0NxibZ