Paragon Care Ltd (ASX: PGC) shares are taking off on Tuesday after returning from a trading halt.

At the time of writing, the ASX small cap stock is up 27% to 26 cents.

Why is this ASX small cap stock rocketing?

Investors have been fighting to get hold of the healthcare supplier’s shares after it announced plans to merge with CH2 Holdings.

CH2 is a privately owned, Australian based distributor and wholesaler of pharmaceuticals, medical consumables, and complementary medicines. It has an 85-year history of providing innovative supply chain solutions to the Australian healthcare industry.

According to the release, the two parties have agreed to a “transformative merger” that they believe will create a leading healthcare wholesaler, distributor, and manufacturer operating across growing healthcare markets in the Asia Pacific region.

The combined entity will have estimated FY 2024 pro-forma revenues of $3.3 billion and EBITDA of $93 million. This includes synergies and cost efficiencies of more than $5 million per annum.

As a comparison, Paragon Care recently released its half-year results and reported revenue of $159.5 million and EBITDA of $13.4 million for the six months.

How does the merger work?

Under the merger, it is proposed that Paragon Care will acquire all of the issued share capital in CH2 in exchange for issuing 943,524,071 shares.

This implies a purchase price of approximately $201.5 million based on where its shares last traded.

The merger will be subject to the approval of Paragon Care shareholders by ordinary resolution (>50%) at a general meeting in late May.

The ASX small cap stock’s board unanimously recommends that shareholders vote in favour of the resolutions to be considered at the merger meeting. This is in the absence of a superior proposal and subject to the independent expert’s report.

The post Guess which ASX small cap stock is rocketing 27% on ‘transformative’ merger appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 1 February 2024

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- How is the Coles share price down 3% today?

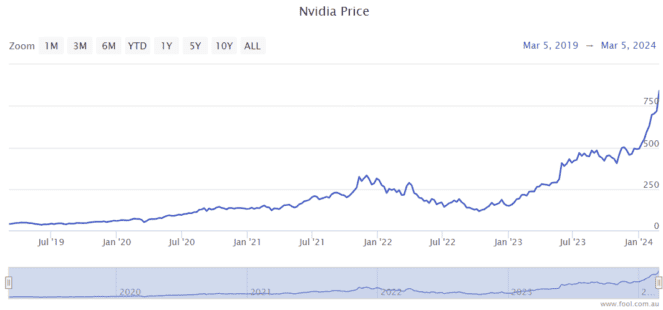

- Is the surging Nvidia share price causing a stock market bubble?

- Guess which ASX lithium stock just surged 94% on a deal with Mineral Resources

- Why is the Lovisa share price sinking today?

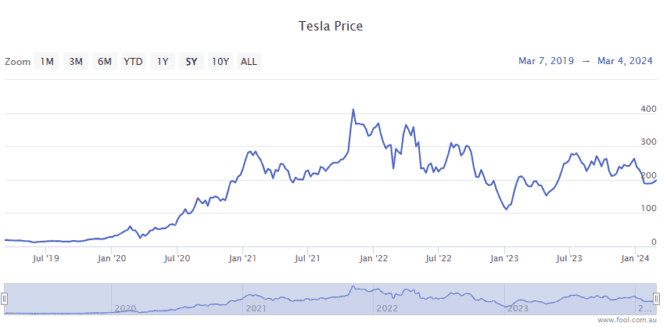

- Why did the Tesla share price just tumble 7%?

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/jszX0wq