The first ASX dividend share that could be a buy is footwear retailer Accent. It owns brands such as The Athlete’s Foot, Platypus, and Stylerunner.

The team at Bell Potter is positive on the company and has a buy rating and $2.50 price target on its shares.

Its analysts highlight that they “remain constructive on AX1 given the scale & exposure in terms of channels, brands & size as the overall industry navigates a challenging retail spend environment.”

Bell Potter is expecting some attractive dividend yields in the near term. It is forecasting fully franked dividends per share of 13 cents in FY 2024 and then 14.6 cents in FY 2025. Based on the latest Accent share price of $2.02, this represents dividend yields of 6.4% and 7.2%, respectively.

The team at Goldman Sachs believes that Orora would be a good ASX dividend share to buy.

It is a designer and manufacturer of packaging products such as fibre-based packaging, glass bottles, beverages cans, and corrugated boxes.

Goldman likes the company due to its defensive qualities. In addition, its analysts “believe the current market implied valuation of Saverglass provides a favourable risk-reward skew.”

The broker has a buy rating and $3.40 price target on its shares.

As for dividends, Goldman Sachs is expecting the company to pay dividends per share of 13 cents in FY 2024 and 14 cents in FY 2025. Based on the current Orora share price of $2.68, this will mean yields of 4.9% and 5.2%, respectively.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has recommended Accent Group and Orora. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/ZMFKCN0

The Lovisa share price was the best performer on the ASX 200 with a 40.9% gain. Investors were scrambling to buy the fashion jewellery retailer’s shares following the release of a strong half-year result. Lovisa defied consumer spending weakness and delivered an 18.2% increase in revenue to $373 million and a 12% lift in net profit after tax to $53.5 million.

The Altium share price wasn’t far behind with an impressive 30.4% gain. This was driven by news that the electronic design software company received and accepted a takeover offer from Japan’s Renesas. If all goes to plan, Renesas will acquire Altium by way of a scheme of arrangement for a cash price of $68.50 per share. This represents a 33.6% premium to its last close price and values Altium’s equity at $9.1 billion.

The WiseTech share price was on form and recorded a 29.4% gain during February. Investors were fighting to get hold of the logistics solutions company’s shares following the release of its half-year results. Wisetech reported a 32% increase in revenue to $500 million and 23% lift in EBITDA to $230 million. The key driver of its first-half growth was the CargoWise business, which reported a 40% increase in revenue to $421 million.

The Reliance share price was a strong performer and rose 29.3% last month. This follows the release of the plumbing parts company’s half-year results. Reliance revealed a 2% decline in sales but a modest lift in net profit after tax for the half. While on paper this may not looking overly impressive, it was comfortably ahead of consensus estimates and garnered positive responses from brokers.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has positions in Altium and Lovisa. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Altium, Lovisa, Reliance Worldwide, and WiseTech Global. The Motley Fool Australia has positions in and has recommended WiseTech Global. The Motley Fool Australia has recommended Lovisa. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/g8Nop69

Investors in the Vanguard Australian Shares Index ETF (ASX: VAS) would be a happy bunch right about now, I’d wager. It was only back in late October that VAS units were going for under $83.50 each. But at the close on Thursday, those same units were priced at $95.63.

This means that investors in this popular exchange-traded fund (ETF) have enjoyed more than a 14% unit price appreciation in just four months. Investors can also add another approximately 0.76% to that return as a result of VAS’s December dividend distribution.

Index fund aficionados might notice that this stonking gain is well outside the norms of what VAS investors usually achieve. After all, ETF provider Vanguard tells us that VAS units have averaged a return of 9.03% per annum (with dividends reinvested) since its ASX inception in 2009. That’s as of 31 January.

That’s the average return for 12 months, not four. So we’ve witnessed a very lucrative window for this index fund indeed.

So what can explain this super-sized return that the Vanguard Australian Shares ETF has enjoyed since October last year?

How have VAS units returned 14% in four months on the ASX?

Well, to answer that, let’s do a refresher on how an index fund like this works. Index funds work by closely tracking an underlying index and replicating its holdings and allocations. Hence the name.

In VAS’s case, the index employed is the S&P/ASX 300 Index (ASX: XKO).

The ASX 300 holds the largest 300 shares on the Australian share market, weighted by market capitalisation. That’s everything from Commonwealth Bank of Australia (ASX: CBA), Woolworths Group Ltd (ASX: WOW) and Telstra Group Ltd (ASX: TLS) to JB Hi-Fi Ltd (ASX: JBH), Ampol Ltd (ASX: ALD) and Harvey Norman Holdings Limited (SX: HVN).

Because it is weighted by market capitalisation, the larger shares (such as CBA) have more weighting and influence in the index, and thus the ETF, than the smaller ones (like Ampol).

Given that the Vanguard Australian Shares ETF merely tracks the ASX 300 Index, it won’t be too surprising to learn that the ASX 300 Index has also returned around 14% since October last year. So it would have been very strange if VAS units didn’t return something similar.

These returns can be further explained by a look at how the most influential shares in the ASX 300 Index, and the VAS ETF, have performed over this period.

Take the CBA share price. It’s up more than 20% since the end of October. The other big four bank shares have all returned a similar result. Whilst the CSL Ltd (ASX: CSL) share price is up almost 24%.

So given how some of the largest shares in the ASX 300 have performed in recent months, it’s easy to see why the Vanguard Australian Shares ETF has followed suit.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor Sebastian Bowen has positions in CSL, Telstra Group, and Vanguard Australian Shares Index ETF. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended CSL. The Motley Fool Australia has positions in and has recommended Harvey Norman and Telstra Group. The Motley Fool Australia has recommended CSL and Jb Hi-Fi. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/S5zAIBQ

On Thursday, the S&P/ASX 200 Index (ASX: XJO) recovered from a shaky started to record a decent gain. The benchmark index rose 0.5% to 7,698.7 points.

Will the market be able to build on this on Friday and end the week on a high note? Here are five things to watch:

ASX 200 expected to edge higher

The Australian share market looks set to end the week in a positive fashion following a decent night on Wall Street. According to the latest SPI futures, the ASX 200 is expected to open 8 points or 0.1% higher this morning. In late trade on Wall Street, the Dow Jones is down slightly, the S&P 500 is up 0.3%, and the NASDAQ is up 0.5%.

Oil prices soften

ASX 200 energy shares Beach Energy Ltd (ASX: BPT) and Karoon Energy Ltd (ASX: KAR) could have a subdued finish to the week after oil prices edged lower overnight. According to Bloomberg, the WTI crude oil price is down 0.3% to US$78.25 a barrel and the Brent crude oil price is down slightly to US$83.66 a barrel. Higher than expected US inventories has put pressure on prices.

Life360 results

The Life360 Inc (ASX: 360) share price will be on watch on Friday when the location technology company releases its FY 2023 results. Goldman Sachs is forecasting subscription revenue of US$221.7 million for the year, which represents annual growth of 51%. EBITDA is expected to come in at US$15.9 million, which is the top end of Life360’s guidance range of US$12 million to US$16 million.

Gold price rises

ASX 200 gold shares including Evolution Mining Ltd (ASX: EVN) and Northern Star Resources Ltd (ASX: NST) could have a good session after the gold price pushed higher overnight. According to CNBC, the spot gold price is up 0.5% to US$2,054.6 an ounce. Gold hit a one-month high after US inflation data came in line with expectations.

Xero remains a buy

Xero Ltd (ASX: XRO) shares are a top buy according to Goldman Sachs. In response to its investor day event, the broker has reiterated its buy rating on the cloud accounting platform provider’s shares with an improved price target of $152.00. This implies almost 20% upside for investors over the next 12 months.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has positions in Life360 and Xero. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group, Life360, and Xero. The Motley Fool Australia has positions in and has recommended Xero. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/V6RFkU1

Since listing on the ASX in its own right back in late 2018, Coles Group Ltd (ASX: COL) has carved out a name for itself as a generous dividend payer. The supermarket giant has increased its annual dividend most years since 2019 without delivering a single dividend cut.

That’s unlike the shares of its arch-rival Woolworths Group Ltd (ASX: WOW).

Coles began by announcing a 3.7% rise in revenues to $22.22 billion over the period. As well as a 4.2% bump in underlying earnings. The company also revealed that its next interim dividend would be worth 36 cents per share, fully franked.

That dividend is flat on what the company paid out for the same period last year. Paired with Coles’ final (and fully franked) dividend of 30 cents per share from September, it keeps the company’s annual dividend steady at 66 cents per share.

This gives the Coles share price both a forward and trailing dividend yield of 3.91%. That’s based on the company’s closing share price of $16.90 yesterday.

How to secure the next Coles dividend

But if you wish to receive this next dividend from Coles, and you don’t already own this company’s stock, time is running out.

Coles is scheduled to trade ex-dividend for this upcoming payment on Tuesday, 5 March. That’s next week, and means the last day you can buy Coles shares with the rights to this payment attached is on Monday, 4 March.

If you buy Coles shares on Tuesday onwards, you’ll miss out. So expect to see a bit of a drop in the Coles share price when the markets open on Tuesday morning, reflecting this inherent loss of value.

For eligible shareholders, Coles will then finally fork out the cash on 27 March. Unless of course, you opt for the dividend reinvestment plan (DRP). If you do so by 7 March, you have the option of receiving additional Coles shares in lieu of the cash payment.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor Sebastian Bowen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has positions in and has recommended Coles Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/vaZ7RMz

With $7,000 of money to spare, I’d avoid going on a shopping spree and instead invest in ASX dividend shares to build an extra income.

Once I have the right ASX portfolio holdings in place, I can use the passive income this delivers to buy the extra goodies I’ve had an eye on.

Here’s how I’d aim to turn a spare $7,000 into an annual $1,000 extra income.

A diversified ASX investment for $1,000 in annual extra income

With $7,000 to spare, I could invest $1,000 in seven different ASX dividend stocks.

If I were to take this route, I’d primarily target companies paying franked dividends, so I can hold onto more of my extra income when the ATO comes knocking.

I’d also be sure to invest in a range of quality companies trading at fair prices. And ones that are operating in different sectors and parts of the world. That kind of diversity will lower my overall investing risks.

I could achieve similar diversity by investing in a high-yielding ASX exchange-traded fund (ETF).

The BetaShares Australian Dividend Harvester Fund (ASX: HVST), for example, holds anywhere from 40 to 60 ASX dividend shares at any given time.

The ETF’s top three holdings are BHP Group Ltd (ASX: BHP), Commonwealth Bank of Australia (ASX: CBA), and National Australia Bank Ltd (ASX: NAB).

BHP, CBA and NAB shares all pay fully franked dividends. And they have lengthy track records of making two annual payments, helping secure that extra income.

But HVST’s holdings are more diversified than just the financial and materials sectors. The ETF is also invested across the healthcare, consumer discretionary, energy and industrial sectors, among others.

As for that extra income, as at 31 January HVST had a 12-month dividend yield of 6.6%, franked at 79.5%.

This equates to a gross yield, which includes those handy franking credits, of 8.9%. The one-year gross return, which includes share price moves, is 8.45%.

Judging by the blue-chip portfolio holdings and with history as my guide, I believe that’s a sustainable long-term return from this ASX dividend ETF.

Now at those returns, my spare $7,000 would see me earning an annual passive income of $592. That’s a fair bit short of my goal.

To garner that $1,000 in yearly extra income at a return of 8.45%, I’d need to own $11,905 of HVST shares.

So I’ll be a bit patient and reinvest those dividends into the ETF as they come in.

In a little over six years, I’ll have reached that level.

And, if I can hold off going on that spending spree a bit longer, my spare $7,000 will have grown to $12,621 after seven years, offering an annual extra income of $1,066.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/F9GlgrI

It’s hard to believe we’re two months into 2024 and have already put another earnings season to bed⦠but, here we are!

For investors, the new year has kicked off quite nicely, with the S&P/ASX 200 Index (ASX: XJO) already up a not-too-shabby 0.98%.

With the hope of keeping the positive returns flowing, we asked our Foolish writers which ASX shares look like top buying opportunities right now. Here is what the team came up with:

6 best ASX shares for March 2024 (smallest to largest)

What it does: IPD Group is an Australian electrical product distributor, serving the country’s electrical equipment needs for more than 70 years. I tend to think of it as the Bunnings of specialised electrical products.

By Mitchell Lawler: There are arguably many demand drivers for electrical equipment in the years to come. Whether it is data centres, electric vehicle infrastructure, or construction growth to meet an increasing population â IPD Group is poised to soak up the expansion.

After many acquisitions, IPD is quickly becoming a one-stop shop for a diverse range of equipment, including power distribution, power monitoring, industrial motor control, and automation.

The high insider ownership among management also gives me confidence that this team is committed to the company’s long-term success.

Motley Fool contributor Mitchell Lawler does not own shares of IPD Group Ltd.

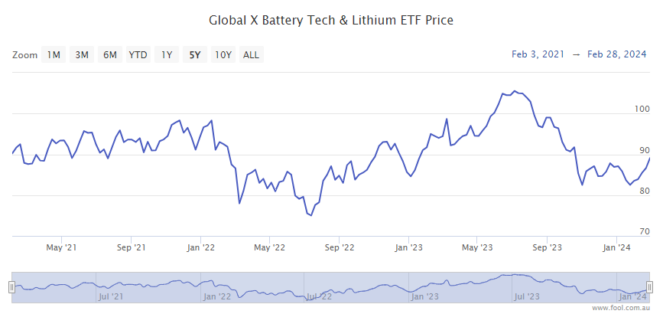

Global X Battery Tech & Lithium ETF

What it does: This exchange-traded fund (ETF) tracks the Solactive Battery Value-Chain Index, which contains stocks for companies involved in battery technology.

By Tony Yoo: Battery materials, especially lithium, have been in a painful funk for 15 months now. But investors could start looking at picking up shares for cheap with a view to the long-term demand for batteries from the electrification of fossil fuel-powered devices.

Rather than attempting to pick the wild fortunes of individual miners, this ETF provides diversification to invest in the industry as a whole. The transition to a less carbon-intensive future is real and, I believe, will be a long-running theme for years to come.

Motley Fool contributor Tony Yoo does not own units of the Global X Battery Tech & Lithium ETF.

Johns Lyng Group Ltd

What it does: The core service this ASX 200 company provides is restoring buildings and contents after an insured event, such as a fire, storm, or flooding. It also has increasing capabilities and exposure related to catastrophe work.

By Tristan Harrison: The Johns Lyng share price dipped after the company reported its FY24 first-half result. While catastrophe revenue may not have been as strong as some investors wished, it’s not the sort of work that is going to grow consistently year after year â I expect it to be lumpy. And, short-term declines can present opportunities.

Johns Lyng’s ‘business as usual’ (BAU) revenue rose 13.7% to $426.1 million, and its normalised NPAT grew by 15.8% to $25 million, demonstrating operating leverage within the business. Plus, it upgraded revenue guidance for FY24 by 3.5%.

Furthermore, I’m excited by the company’s expansion in the strata industry. Acquiring strata managers can result in more consistent (and growing) revenue and also create synergies with the core business.

I am planning to buy more Johns Lyng shares soon.

Motley Fool contributor Tristan Harrison owns shares of Johns Lyng Group Ltd.

Flight Centre Travel Group Ltd

What it does: The ASX 200 company is one of the world’s largest travel agency groups. Flight Centre operates in more than 23 countries, with a corporate travel management network that spans more than 90 countries.

By Bernd Struben:I believe the Flight Centre share price remains materially undervalued over the longer term.

Given the company’s earnings and revenue growth, not to mention its return to profitability, I think it has the potential to eventually retrace to pre-COVID levels of more than $40 a share. That essential doubling in the share price won’t come overnight. But the company is certainly moving in the right direction.

And we saw the return of the interim dividend, which followed on from the reinstatement of the final dividend in September. Flight Centre trades on a fully-franked trailing yield of 1.4%.

Motley Fool contributor Bernd Struben does not own shares of Flight Centre Travel Group Ltd.

Woolworths Group Ltd

What it does: Woolworths is Australia’s largest supermarket operator. It also owns the Big W brand and has a growing presence in the pet care market.

By James Mickleboro: With the company’s shares trading within sight of a 52-week low, I think now is a great time to invest in this high-quality company. Particularly given its leadership position in a defensive market with high barriers to entry.

In addition, recent weakness in the Woolworths share price means it offers an attractive dividend yield in the region of 3.2%.

Goldman Sachs remains very positive on the company. So much so that it has Woolworths shares on its coveted conviction list with a buy rating and $40.40 price target.

Motley Fool contributor James Mickleboro does not own shares of Woolworths Group Ltd.

CSL Ltd

What it does: CSL is the largest healthcare company in Australia. It has an extensive global plasma collections operation, as well as a world-leading vaccine and blood medicine division.

I think this presents an opportunity for CSL shares this March, though. The company is still growing at a healthy pace and has recently hiked its dividend by 12%.

CSL’s plasma collections business remains lucrative and should underpin earnings growth for years to come. I think you could do a lot worse than CSL shares at the recent pricing.

Motley Fool contributor Sebastian Bowen owns shares of CSL Ltd.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended CSL, Global X Battery Tech & Lithium ETF, Ipd Group, Johns Lyng Group, and Goldman Sachs Group. The Motley Fool Australia has recommended CSL, Flight Centre Travel Group, Global X Battery Tech & Lithium ETF, Ipd Group, and Johns Lyng Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/TZzDm2Y

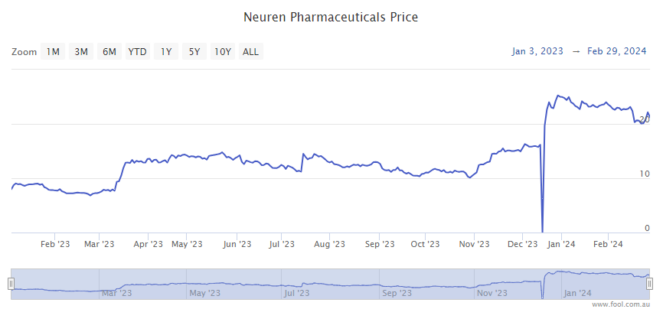

The Neuren Pharmaceuticals Ltd (ASX: NEU) share price gained 1.1% to close at $19.36 on Thursday despite encountering some turbulence in late afternoon trading.

Most of the gains occurred at the beginning of today’s session with the stock rising to an intraday high of $19.70 shortly after the open.

Neuren received $231.9 million in revenue after licencing its first drug, Daybue, to US partner Acadia Pharmaceuticals (NASDAQ: ACAD).

This included $59.4 million for the first commercial sales milestone, an upfront $145.7 million under the expanded global licence agreement, and $26.8 million from quarterly royalty income.

Other income included interest income of $5.7 million and foreign exchange gains of $2.4 million.

Neuren shares ripped up the charts, gaining 214% over the 12 months to 31 December.

Most of that gain came on the back of FDA approval and the initial sales success of Daybue, which is a world-first drug treatment for Rett syndrome.

The Neuren share price surged again in December after the company released top-line results from its Phase 2 clinical trial of NNZ-2591 in children with the debilitating Phelan-McDermid syndrome (PMS).

There are currently no approved treatments for PMS. According to the release, a significant improvement was observed by both clinicians and caregivers from treatment during the trial.

What did management say?

Neuren CEO Jon Pilcher said:

2023 delivered a profit of A$157 million, an exceptional US launch of DAYBUE by Acadia, US$100 million up-front from an expanded partnership with Acadia for trofinetide worldwide and outstanding results from the first clinical trial of NNZ-2591 in patients.

Neuren has never been in a stronger position, with substantial ongoing cash flows and a series of value creating catalysts approaching in 2024.

The short seller’s report was released in the US on 15 February, and Neuren issued a response that failed to stop the Neuren Pharmaceuticals share price crashing by 14.2%.

Ahead of today’s full-year FY23 report, Arcadia announced 4Q FY23 net sales of Daybue worth US$87.1 million in the US. This was at the top end of the company’s guidance range of US$80 million to $87.5 million, following on from net sales of US$67 million in Q3 FY23 and US$23 million in Q2 FY23.

Arcadia also provided full-year 2024 guidance of sales between US$370 million and US$420 million.

However, ASX investors were not pleased and the Neuren Pharmaceuticals share price fell 10.3%.

Neuren Pharmaceuticals share price snapshot

The Neuren Pharmaceuticals share price is down 22% in the year to date.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bronwyn Allen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/FGyL0Sa

The S&P/ASX 200 Index (ASX: XJO) overcame a slow and shaky start this morning to post a convincing gain by the close of trading this Thursday.

After falling at market open, the ASX 200 recovered during afternoon trading and posted a pleasing gain of 0.5%, leaving the index at 7,698.7 points.

This late burst of optimism for ASX shares follows a more negative night of trade up on the American markets last night (our time).

The Dow Jones Industrial Average Index (DJX: .DJI) had a fairly negative session, but closed just 0.06% lower.

It was a bit worse for the Nasdaq Composite Index (NASDAQ: .IXIC) though, which sank a more decisive 0.55%.

But returning to the local markets now, and it’s time for a checkup of how the various ASX sectors navigated this Thursday’s trading.

Winners and losers

It was a cracking day almost all around for ASX shares, with only one sector taking a backwards step today.

That unlucky sector was utilities shares. The S&P/ASX 200 Utilities Index (ASX: XUJ) was singled out, losing 0.33% of its value.

Meanwhile, every other sector advanced.

The most enthusiastic jumper was the real estate investment trusts (REIT) space. The S&P/ASX 200 A-REIT Index (ASX: XPJ) had a fantastic time, shooting up 1.67%.

As did the gold sector. The All Ordinaries Gold Index (ASX: XGD) surged by 1.46%.

Consumer discretionary shares were in demand as well, as you can see from the S&P/ASX 200 Consumer Discretionary Index (ASX: XDJ)’s rise of 1.29%.

We can say the same for tech stocks. The S&P/ASX 200 Information Technology Index (ASX: XIJ) was on fire too, bouncing 0.86%.

Communications shares came next. The S&P/ASX 200 Communication Services Index (ASX: XTJ) enjoyed a lift of 0.84% this Thursday.

Consumer staples stocks were another bright spot, evidenced by the S&P/ASX 200 Consumer Staples Index (ASX: XSJ)’s 0.56% bump.

Healthcare shares were being snapped up by investors too, with the S&P/ASX 200 Healthcare Index (ASX: XHJ) increasing by 0.51%.

Industrial stocks got an invite to the party as well. The S&P/ASX 200 Industrials Index (ASX: XNJ) got a 0.47% upgrade by the end of the day.

Mining shares were getting bought up this Thursday. The S&P/ASX 200 Materials Index (ASX: XMJ) saw its value get a 0.3% push higher.

Energy stocks were just behind that. The S&P/ASX 200 Energy Index (ASX: XEJ) recorded an uptick of 0.26%.

Our final gainer was the financial space. The S&P/ASX 200 Financials Index (ASX: XFJ) vaulted up 0.19%.

Top 10 ASX 200 shares countdown

The index winner this Thursday was tech stock Weebit Nano Ltd (ASX: WBT).

Weebit shares had a top day, rocketing 9.6% up to $4.34 each. That was despite no fresh news or announcements out of the company whatsoever.

Our top 10 shares countdown is a recurring end-of-day summary to let you know which companies were making big moves on the day. Check in at Fool.com.au after the weekday market closes to see which stocks make the countdown.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor Sebastian Bowen has positions in Ramsay Health Care. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended PolyNovo. The Motley Fool Australia has positions in and has recommended Harvey Norman. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Y73HxS6

It’s a good time to trade because all the latest financial results are on the table for all of us to see.

Go big or go home ASX REIT buy-up

The biggest insider buy so far this earnings season appears to be a $42 million ASX 300 REIT buy-up.

David Di Pilla, the managing director and CEO of the Healthco Healthcare and Wellness REIT (ASX: HCW) bought 31,912,867 shares in the real estate investment trust (REIT) this month.

Di Pilla paid an average price of $1.335. This on-market trade was worth $42.6 million and change.

The ASX 300 REIT explained the trade as follows:

As announced on 2 May 2023, HMC entered into a cash settled total return swap with Macquarie Bank Limited in respect of 31,912,867 units (TRS). HMC has now unwound the TRS and retained exposure to those units by acquiring them directly on market.

The acquisition was approved by HCW unitholders pursuant to Resolution 3 at the HCW Extraordinary General Meeting held on 24 July 2023.

The Healthco Healthcare and Wellness REIT share price was up 1.85%, trading at $1.375 at the close on Thursday.

Founder and managing director Jamie Pherous bought 87,500 Corporate Travel Management shares this month in an on-market trade worth just shy of $1.4 million. He paid an average price of $15.98 for the ASX 300 travel stock. This is the first time Pherous has traded in the travel share in two-and-a-half years.

The Corporate Travel Management share price closed 0.51% higher at $15.92 on Thursday.

ASX chair Damian Roche snapped up 10,000 shares in the market operator this month, buying at an average price of $64.363. His total investment was $643,628.

The ASX share price was up 0.94% to $65.75 in afternoon trading.

Nico Resources non-executive chair Peter Cook invested $300,000 in purchasing two million shares in the ASX 300 nickel miner. He paid an average price of 15 cents apiece. Nickel was added to the Critical Minerals List this month amid a massive and growing supply coming out of Indonesia, where China is funding the rapid development of mines.

The Nico Resources share price closed 2.86% higher at 18 cents.

IGO managing director and CEO Ivan Vella purchased 41,500 IGO shares on-market at an average price of $7.274 this month. This investment in the nickel and lithium producer totalled $301,852. IGO chair Michael Nossal also upped his holdings by 25,000 shares, paying an average price of $7.234 per share or $180,840 in total.

The IGO share price was down 2.46% to $7.94 at the close on Thursday.

Non-executive director Michael McCormack bought 30,000 Whitehaven shares this month in an on-market trade worth just over $214,000. He paid an average of $7.144 for the ASX 300 coal stock.

The Whitehaven share price closed 1.57% lower at $6.92 on Thursday.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. We believe these stocks are trading at attractive prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bronwyn Allen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Corporate Travel Management. The Motley Fool Australia has recommended Corporate Travel Management. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/FBZ3nig