Of course, here at The Motley Fool we always recommend investors practise proper diversification to manage investment risk.

But there’s nothing wrong with fantasising about wild riches from a single ASX stock. It’s just good, clean fun.

Besides, such examples demonstrate that just one or two winners can send an entire diversified portfolio into profit by cancelling out the losers.

It’s actually an advertisement for diversification.

Let’s now take a look at the journey of Telix Pharmaceuticals Ltd (ASX: TLX) and how wealthy this healthcare stock could have made you by now:

What does Telix Pharmaceuticals do?

Telix Pharmaceuticals develops diagnostic and therapeutic products for different types of cancer.

When COVID-19 first spread around the globe, financial markets understandably went into meltdown.

After all, no one knew back then whether this disease would kill half the world’s population or whether we’d be forced to live in lockdown forever.

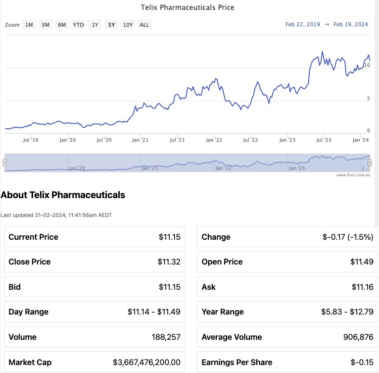

In the worst depths of the market crash, in March 2020, you could buy Telix shares for 87 cents apiece.

Imagine that you had the wisdom to buy $20,000 worth at that point.

Over the next four years, you would have watched proudly as Telix Pharmaceuticals ticked off one milestone after another.

Perhaps the biggest achievement over that time was attaining commercial approval for its ââprostate cancer imaging product Illuccix. This took Telix from a pre-revenue startup to one that makes its own money.

While Illucix is bringing in valuable revenue, Telix has been able to work on future products for other types of cancer, such as kidney, brain, and bone marrow.

The hero healthcare stock

This rapid growth and enormous future potential have forced the market to sit up and take notice of the healthcare stock.

As of Wednesday afternoon, the Telix stock price was trading at $11.19, which makes it an almost 13-bagger since you bought those 87 cent shares one Olympic cycle ago.

So that $20,000 you invested? It’s now worth $257,241.

Amazing.

Check out how this one winner could have supercharged a diversified portfolio.

At the time you bought the $20,000 batch of Telix shares, say you also bought five other stocks in other industries and geographies to spread your risk.

Then imagine that those five businesses all went through absolute devastation and have now shrunk to $0.

That portfolio would now be more than double what the original $120,000 outlay.

Ladies and gentlemen, right there is the power of ASX shares and diversification.

The post If you’d put $20,000 in this ASX healthcare stock during COVID-19, you’d have $257,000 now appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 10 November 2023

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- Here are the top 10 ASX 200 shares today

- The market is placing ‘zero value’ on this ASX 200 stock’s booming pipeline

- 2 ASX stock picks with explosive potential

- 2 top ASX growth shares to buy right now and hold for the long term

Motley Fool contributor Tony Yoo has positions in Telix Pharmaceuticals. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Telix Pharmaceuticals. The Motley Fool Australia has recommended Telix Pharmaceuticals. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/S8B2i1K