While Westpac Banking Corp (ASX: WBC) is a popular option for income investors, its shares are currently trading at a 52-week high.

In addition, they are trading beyond the valuations of almost all brokers. This makes them a riskier than usual proposition for investors.

In the absence of a decent pullback that creates a better entry point, income investors might find more value from the ASX dividend stocks listed below.

Goldman Sachs thinks that telco giant Telstra could be a great option for income investors.

The broker rates the company highly due to its low risk earnings and dividends growth over FY 2023 to FY 2025.

It is expecting this to lead to Telstra paying fully franked dividends of 18 cents per share in FY 2024, 19 cents per share in FY 2025, and then 20 cents per share in FY 2026. Based on the current Telstra share price of $3.97, this equates to yields of 4.5%, 4.8%, and 5%, respectively.

Goldman has a buy rating and $4.65 price target on Telstra’s shares.

Another ASX dividend stock that analysts think could be in the buy zone at current levels is toll road operator Transurban.

Citi remains positive on the company following its first half results release last week. So much so, it continues to expect Transurban to pay dividends ahead of guidance in FY 2024.

The broker is forecasting dividends per share of 63 cents in FY 2024, 65 cents in FY 2025, and 68 cents in FY 2026. Based on the current Transurban share price of $12.90, this will mean yields of 4.9%, 5%, and 5.3%, respectively.

Citi has a buy rating and $15.60 price target on the company’s shares.

Finally, in case you were wondering, Goldman and Citi have neutral ratings and $22.85 and $22.25 price targets on Westpac’s shares.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Citigroup is an advertising partner of The Ascent, a Motley Fool company. Motley Fool contributor James Mickleboro has positions in Westpac Banking Corporation. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group and Transurban Group. The Motley Fool Australia has positions in and has recommended Telstra Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Q7ktm1H

On the face of it, buying investment property in Australia’s regions may seem like the inferior choice.

Historically, regional properties have been a cheaper option for investors, delivering superior rental returns but less capital growth than the cities. And it was harder to find a good long-term tenant.

Depends on your point of view. Small-caps are riskier investments but the good ones can deliver more share price growth than the large-caps over the long term. But they typically don’t pay dividends, so there’s no yield for their investors, and they can struggle to perform in poor economic conditions.

But are times changing? Are regional properties and ASX small-caps looking more attractive these days?

Over the past three years, regional properties have actually grown at a faster rate than city properties.

They’ve still delivered superior rental returns, and it’s become much easier to find a tenant with the average regional vacancy rate currently as low as the cities at 0.8%, according to Domain data.

And what about ASX small-cap shares?

Some experts are saying they’re looking more attractive, given they were sold off as interest rates rose, and now that rates are expected to fall, their prospects for share price gains look better.

Let’s investigate further.

Buying investment property in regional areas

A key reason why capital cities have historically delivered better capital gains is population density and growth.

Migration is the primary driver of our population growth, and we don’t build enough new homes. That means housing demand goes up at a rapid rate every year, with all those new arrivals needing homes immediately. Natural increase (births minus deaths) raises housing demand much more slowly.

On top of that, Australia only has eight capital cities, and almost 70% of us choose to live in one of them.

But Australia has just undergone a dramatic population shift.

During the pandemic, working from home enabled thousands of city dwellers to relocate to the regions for more affordable housing and arguably a better lifestyle.

This trend continued for a while, leading to massive property price growth. So much so that the 10-year rate of capital growth is now higher in the regions, as this chart shows.

This has changed the game when it comes to buying investment property.

While that COVID surge in interstate migration has tapered back, remote work is a permanent change.

This means future generations will have far more choices as to where to live. This may create permanent changes in our population movement, especially given the housing affordability challenges in our cities.

The Regional Australia Institute (RAI) estimates that 3.5 million Australians are interested in relocating to regional areas today.

Difficulty finding employment was previously a deterrent to regional living. Now, people can take their jobs with them, or find one pretty easily locally.

The Federal Government’s newly released State of Australia’s Regions 2024 report says three years of record agricultural production and expanded tourism have contributed to strong regional economic growth and a more than doubling of regional job ads over the four years to October 2023.

Put all that together, and regional property markets seem to have stronger economic fundamentals to support better capital gains in the future.

Plus, most of them are still cheaper than city markets and still deliver better rental yields.

Will this see more people buying investment property in regional areas?

It seems so, with research by MCG Quantity Surveyors revealing the average distance between landlords’ primary residences and their property investments soared to 1,502km in the year to November 2023.

ASX small-cap shares are those with a market capitalisation of between a few hundred thousand and $2 billion.

They are typically young and growing companies that have yet to establish strong, consistent earnings. They often don’t do well when interest rates are rising because they’re carrying debt to enable expansion.

Their share prices are volatile, and their trading liquidity is often constrained.

However, for investors with medium to high risk tolerance, ASX small caps can be more attractive. This is mainly because their prospects for long-term capital growth can be better.

In an interview with my colleague Bernd last month, Gracey said:

Small companies and particularly microcap companies have underperformed their Australia blue-chip peers over the last few years, so there certainly is rationale to anticipate some form of catchup for these emerging companies.

Gracey has some tips for investors interested in buying ASX small-cap stocks this year.

Morgans analysts also think ASX small-cap shares may be in for a good year, commenting:

Small-caps have historically bounced hardest upon confirmation of a flattening-out in the rates cycle. Several ingredients remain in place supporting a rebound in this space (rates, trading/fundamentals, sentiment/positioning). We think the tide is turning for small-caps, and now is an opportune time to build exposure to forgotten small-caps.

Broker Bell Potter says luxury retailer Cettire Ltd (ASX: CTT) and electrical infrastructure products group IPD Group Ltd (ASX: IPG) are small-caps worth buying.

LSN Emerging Companies Fund likes financial services provider EQT Holdings Ltd (ASX: EQT) and MMA Offshore Ltd (ASX: MRM).

Joe Wright of Airlie Funds Management says ASX small-cap stock selection is crucial. He recommends avoiding ‘concept’ companies and those with excessive gearing.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bronwyn Allen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Ipd Group. The Motley Fool Australia has recommended Cettire, Ipd Group, and Mma Offshore. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/xcbHNnO

You don’t need to be a millionaire to start earning a meaningful annual passive income stream.

In fact, by investing just $833 a month in ASX shares, you could create a passive income of $845 a year, or more, in only 12 months’ time.

Now, there are a wide number of quality S&P/ASX 200 Index (ASX: XJO) dividend stocks that could help you achieve this goal. But, keeping in mind the importance of diversification, you wouldn’t want to invest all of your money into a single, high-yielding company.

Even quality companies with a good track record of annual dividend payouts can run into short-term troubles that could slash the passive income you were expecting to bank.

However, as you may have noticed in the title, I did mention one particular ASX share.

Here’s why.

This ASX ETF is a passive income leader

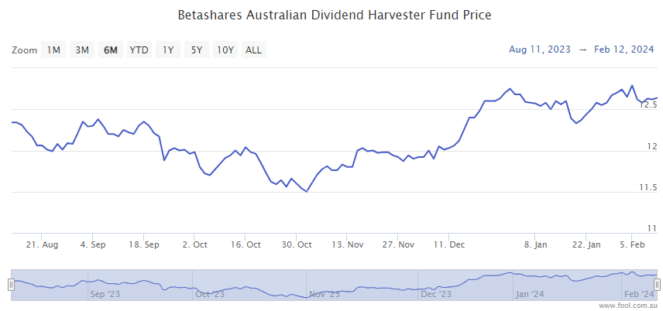

The ASX share in question is the BetaShares Australian Dividend Harvester Fund (ASX: HVST).

The appealing thing for passive income hunters is that this exchange-traded fund (ETF) gives investors instant diversity through its portfolio of 40 to 60 high-yielding, blue-chip ASX shares.

As of the end of December, the ETF’s top three holdings are Commonwealth Bank of Australia (ASX: CBA) BHP Group Ltd (ASX: BHP) and CSL Limited (ASX: CSL).

And HVST pays out dividends on a monthly basis, meaning your next passive income payout is never too far away.

Because the ETF’s holdings are actively managed and rebalanced every three months to target higher-yielding ASX dividend stocks, the annual management fee is 0.72%.

If you’re looking to capture the magic of compounding so you can watch your annual income soar over the years, HVST offers a partial or full dividend reinvestment plan.

As at 31 January, the ETF had a 12-month trailing yield of 5.94%, 79.5% franked. Those franking credits bring the grossed-up yield to 8.45%.

Based on this grossed-up dividend yield alone, investing $833 a month (or $10,000 over a year) should deliver $845 in annual passive income.

Of course, we’re also hoping to see the ETF deliver some share price gains in 2024.

The HVST share price is down 2% since this time last year. But the ETF has gained 10% since 31 October.

If that upward trend continues, it could see this ASX ETF deliver significantly more than $845 in passive income from those 12 monthly $833 investments.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended CSL. The Motley Fool Australia has recommended CSL. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Yxo1Z5F

Fletcher Building Ltd (ASX: FBU) shares be suspended until later today to give the building products company time to explain its bombshell announcement to analysts and investors. The ASX 200 stock’s suspension request states:

[Fletcher Building] considers it appropriate for additional time to be provided following the conclusion of the investor call, to enable investors and the market to consider and assess the information released by FBU and the commentary provided at the investor call.

What’s going on with this ASX 200 stock?

This morning Fletcher Building released its half-year results which were significantly weaker than the market was expecting. It also announced the impending exit of its CEO, Ross Taylor.

In respect to its results, the ASX 200 stock reported:

Revenue down 1% to NZ$4,248 million,

EBIT before significant items down 27% to NZ$264 million,

Net loss after tax of NZ$120 million

Dividend suspended

What happened?

Fletcher Building’s outgoing chief executive, Ross Taylor, revealed that its performance was impacted largely by challenging trading conditions in New Zealand. He said:

Against the backdrop of materially weaker trading conditions, particularly in the NZ residential sector where volumes declined 20%, Group revenue of NZ$4,248 million was in line with the prior period’s NZ$4,284 million. EBIT before significant items was NZ$264 million, compared to NZ$360 million in the prior period.

Taylor also advised that significant items weighed on its profits. He adds:

The Group reported a net loss after tax of NZ$120 million, compared to a profit of NZ$92 million in the prior period. Disappointingly, the result was heavily impacted by the NZ$165 million significant items provision on the New Zealand International Convention Centre announced on 5 February and a $122 million non-cash impairment and writedown on the Tradelink Australia business.

Management is now looking to divest the Australian Tradelink business after deciding that “further ownership of the business is not in line with the strategic objectives of Fletcher Building.”

CEO and chair to exit

In a separate announcement, the ASX 200 stock advised that Ross Taylor will be leaving the company along with its chair, Bruce Hassall.

Hassall commented:

The Board, Ross and I believe it is in the best interests of the business and the team that he handover to a new leader and that I hand over to a new Chair at the time of the ASM in October.

Mr Taylor has a six-month notice period, which he will serve in full if required to facilitate an orderly handover to his successor.

Fletcher Building shares are down 19% over the last 12 months.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/KbifuCo

Thinking of buying the Vanguard Australian Shares Index ETF (ASX: VAS)? You’re probably not alone. VAS is the most popular exchange-traded fund (ETF), and index fund, on our ASX stock market. And by quite a mile too.

But although this ETF looks relatively simple, with just one ticker code, the reality is that it is a rather complex investment.

So if you’re thinking of buying VAS units today or in the future, it’s probably a good idea to know exactly where your money is going.

The ASX’s most popular index fund

As we touched on earlier, the Vanguard Australian Shares ETF is an index fund. This means that it represents an investment in an entire index, rather than a single ASX company.

In this particular case, the Vanguard Australian Shares ETF mirrors the S&P/ASX 300 Index (ASX: XKO). The ASX 300 is an index that tracks the fortunes of the 300 largest companies listed on the Australian stock market.

However, it doesn’t give equal representation to those 300 shares. Like most indexes, the ASX 300 is weighted by market capitalisation (size). This means that the largest shares have more influence in the index (and therefore the index fund) than the smaller ones.

What does VAS’ ASX portfolio look like?

To illustrate, let’s look at the five largest ASX 300 shares in VAS’s portfolio right now, along with their portfolio weightings (as of 31 December):

BHP Group Ltd (ASX: BHP) with a VAS portfolio weighting of 11.01%

Commonwealth Bank of Australia (ASX: CBA) with a weighting of 8.07%

National Australia Bank Ltd (ASX: NAB) with a weighting of 4.14%

Westpac Banking Corp (ASX: WBC) with a weighting of 3.46%

ANZ Group Holdings Ltd (ASX: ANZ) with a weighting of 3.36%

Macquarie Group Ltd (ASX: MQG) with a weighting of 2.84%

Wesfarmers Ltd (ASX: WES) with a weighting of 2.79%

Woodside Energy Group Ltd (ASX: WDS) with a weighting of 2.54%

Rio Tinto Limited (ASX: RIO) with a weighting of 2.17%

In very simple terms, this means that for every $100 you invest into VAS’s ASX units, $11.01 will be allocated to BHP shares. A further $8.07 will go towards an investment in CBA, and so on.

But a company like Kogan.com Ltd (ASX: KGN), which is up the back end of the ASX 300, and thus, VAS’ ASX portfolio, only commands a weighting of 0.019%. That means that of your $100, only 1.9 cents will find its way into Kogan shares.

As you can see, putting money into the Vanguard Australian Shares ETF will see your money spread out over a huge number of different investments. So hopefully you now have a better understanding of how an index fund like VAS works on the ASX if you’re thinking about buying into this popular ASX ETF.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Sebastian Bowen has positions in CSL, Kogan.com, National Australia Bank, and Vanguard Australian Shares Index ETF. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended CSL, Kogan.com, Macquarie Group, and Wesfarmers. The Motley Fool Australia has positions in and has recommended Macquarie Group and Wesfarmers. The Motley Fool Australia has recommended CSL and Kogan.com. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/TOmdX36

The first ASX dividend share that could be a buy is Dexus Convenience Retail REIT. It is a convenience retail and service station property company.

Morgans is positive on the company and believes its shares are good value at current levels. Last week the broker put an add rating and $3.23 price target on its shares.

Its analysts are expecting some big dividend yields in the coming years. They are forecasting dividends per share of 21 cents in both FY 2024 and FY 2025. Based on its current share price of $2.84, this implies yields of 7.4%.

Another ASX dividend share for income investors to look at is agribusiness company Elders. It provides livestock, real estate, feed and processing, wool agency services, and grain marketing services to rural and regional customers.

Bell Potter is a fan of the company, particularly given how operating conditions have been more favourable for Elders since the release of its FY 2023 results. It has a buy rating and $9.50 price target on its shares.

As for income, the broker is forecasting dividends per share of 34 cents in FY 2024 and 41 cents in FY 2025. Based on the current Elders share price of $8.99, this will mean yields of 3.8% and 4.55%, respectively.

Finally, Goldman Sachs believes that Orora would be a good option for income investors. It designs and manufactures packaging products such as fibre-based packaging, glass bottles, beverages cans, and corrugated boxes.

Goldman likes the company due to its defensive qualities and positive growth outlook. The broker has a buy rating and $3.50 price target on its shares.

In respect to dividends, it expects dividends per share of 14 cents in FY 2024 and 15 cents in FY 2025. Based on the current Orora share price of $2.83, this will mean yields of 4.9% and 5.3%, respectively.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has recommended Elders and Orora. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/Oo74AjL

The Commonwealth Bank of Australia (ASX: CBA) share price will be on watch today.

That’s because the banking giant has just released its half-year results and delivered a cash profit slightly ahead of expectations.

CBA share price on watch following half-year results

For the six months ended 31 December, Australia’s largest bank reported the following compared to the prior corresponding period:

Operating income up 0.2% to $13,649 million

Operating expenses up 4% to $6,011 million

Cash net profit after tax down 3% to $5,019 million

Fully franked interim dividend up 2.4% to $2.15 per share

What happened during the half?

CBA’s operating income was up slightly to $13,649 million during the first half. This was supported by volume growth and higher volume-based fee income, offset by margin compression.

Speaking of which, the bank’s net interest margin has fallen 6 basis points since the end of FY 2023 to 1.99%. This reflects increased deposit price competition and deposit switching.

Also heading in the wrong direction were the bank’s expenses. CBA’s operating expenses increased 4% to $6,011 million due to inflationary pressures and additional spending on technology to support the delivery of strategic priorities.

This ultimately led to CBA’s cash net profit after tax falling 3% to $5,019 million. Statutory net profit after tax was down by 8% to $4,837 million.

Nevertheless, this didn’t stop the CBA board from lifting its fully franked interim dividend by 2.4% to $2.15 per share. This represents a payout ratio of 72%, which is up from 68% a year earlier.

CBA ended the period with a CET1 ratio of 12.3%.

How does this compare to expectations?

The good news for the CBA share price is that this result appears to have come in slightly ahead of expectations.

The market consensus estimate was for a first half cash profit of $4,972 million.

Outlook

CBA’s CEO, Matt Comyn, commented that 2023 was a challenging year and warned that there could be some tough times ahead. He said:

2023 was increasingly challenging for many of our customers who are finding it harder to absorb cost of living pressures. The economy has been fairly resilient, supported by a strong labour market, savings and repayment buffers, population growth and relatively high commodity prices. However, downside risks are building as slowing demand and persistent inflation impact Australian businesses. Ongoing geopolitical tensions also create uncertainty.

As cash rate increases have a lagged impact on households and business customers, we expect financial strain to continue in 2024, with an uptick in our arrears and impairments. We remain well provisioned and capitalised, with capacity to navigate an uncertain economic environment.

The CBA share price is up 6% over the last 12 months.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/WUnk2BP

This hugely popular fund provides investors with access to 100 of the best companies the world has to offer. These are the giants of Wall Street’s Nasdaq index and include the likes of Apple, Microsoft, and Tesla.

Over the last five years, the index it tracks has delivered an average return of 23% per annum.

If you’re a fan of Warren Buffett and his style of investing, then this could be the fund for you. That’s because it mirrors his investment style by providing you with access to companies with fair valuations, strong business models, and competitive advantages.

Over the last five years, it has delivered an average return of 16.5% per annum for investors.

Vanguard MSCI Index International Shares ETFÂ (ASX: VGS)

This fund provides investors with easy access to approximately 1,500 of the world’s largest listed companies from major developed countries.

Not only does this give investors access to global economic growth, but it also provides almost instant diversification to a portfolio. This is thanks to it offering exposure to sectors ranging from technology to financials and healthcare to energy.

Over the last five years, it has generated an average return of 13.75% per annum.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has positions in BetaShares Nasdaq 100 ETF. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Apple, BetaShares Nasdaq 100 ETF, Microsoft, and Tesla. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool Australia has positions in and has recommended BetaShares Nasdaq 100 ETF. The Motley Fool Australia has recommended Apple, VanEck Morningstar Wide Moat ETF, and Vanguard Msci Index International Shares ETF. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/6i5BU9d

On Tuesday, the S&P/ASX 200 Index (ASX: XJO) slipped into the red. The benchmark index ended the day 0.15% lower at 7,603.6 points.

Will the market be able to bounce back from this on Wednesday? Here are five things to watch:

ASX 200 expected to sink

The Australian share market looks set for a very red day on Wednesday after a hotter than expected inflation reading in the US spooked investors. According to the latest SPI futures, the ASX 200 is expected to open the day 106 points or 1.4% lower. In late trade on Wall Street, the Dow Jones is down 1.8%, the S&P 500 has fallen 1.8%, and the Nasdaq is 2.1% lower.

Oil prices rise

It could still be a good session for ASX 200 energy shares including Beach Energy Ltd (ASX: BPT) and Woodside Energy Group Ltd (ASX: WDS) after oil prices charged higher overnight. According to Bloomberg, the WTI crude oil price is up 1.4% to US$78.01 a barrel and the Brent crude oil price is up 1.1% to US$82.90 a barrel. Oil prices have been on a good run amid tensions in the Middle East.

Computershare results

The Computershare Ltd (ASX: CPU) share price will be on watch today after the company released its half-year results. The administration services company reported a 6% increase in management revenue to $1.6 billion and a 23% jump in management earnings per share to 54.8 cents. This was in line with the market’s expectations.

Gold price tumbles

ASX 200 gold shares including Newmont Corporation (ASX: NEM) and Northern Star Resources Ltd (ASX: NST) could have a difficult session on Wednesday after the gold price sank overnight. According to CNBC, the spot gold price is down 1.4% to US$2,005.4 an ounce. Traders were selling gold in response to the higher than expected inflation reading.

CBA results

Commonwealth Bank of Australia (ASX: CBA) shares will be on watch on Wednesday when the banking giant releases its half year results. The market is expecting Australia’s largest bank to report a first half cash profit of $4,972 million. This will be down from last year’s record half-year cash profit of $5,153 million.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has positions in Woodside Energy Group. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/3EcWeON

Love it or loathe it, Valentine’s Day has arrived.

Regardless of what you think of the concept, there is no doubt the day has become a big deal commercially.

“Australians expected to spend around $1.1 billion on Valentine’s Day, according to Finder’s research,” said Moomoo market strategist Jessica Amir.

“The Australian Retailers Association and Roy Morgan suggest Australians plan to spend $485 million on Valentine’s Day gifts, with 42% choosing roses.”

And with all this consumption going on, there must be some ASX shares that will benefit, right?

Indeed, here are three stocks that Amir reckons could do pretty well out of all this outpouring of love:

First, some wine

Like it or not, many Australians like to commemorate a special occasion with a glass or two.

Especially so on a romantic day like Valentine’s Day.

“What’s a celebration without a bit of wine, of course,” said Amir.

“Keep an eye out for the Australian global wine-making business Treasury Wine Estates Ltd (ASX: TWE).”

Even without 14 February, many professional investors are in love with Treasury Wine shares at the moment because of the possibility that China will reduce punitive tariffs on Australian wine imports.

According to CMC Invest, 12 out of 14 experts are recommending a buy for Treasury Wine shares.

The share price is already up more than 4% so far this year.

Then let’s light the candles and see what happens

Then after you’ve enjoyed some social lubrication, it might be time to dim the house lights and fire up the candles.

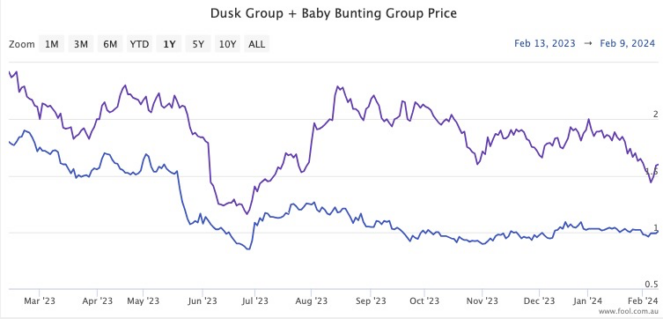

“For other Aussie stocks that might be boosted amidst V-Day spending, consider⦠candle stockist Dusk Group Ltd (ASX: DSK).”

The Dusk share price has lost 43% over the past year, but that does mean it now has a mouthwatering — and fully franked — 11% dividend yield.

So maybe if the candles led to the ultimate expression of love, there may be some further great news down the track.

And Amir has the ASX stock perfectly poised to take advantage.

“Offering Aussies baby products, Baby Bunting Group Ltd (ASX: BBN) might just tick up amidst Valentine’s Day celebrations.”

The retailer also pays out a decent income, currently distributing a fully franked yield of 4.5%.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tony Yoo has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has recommended Treasury Wine Estates. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/47WTKjr