I’d love to receive $30,000 of annual passive income, but right now, I’m only getting a fraction of that. I hope to get there in the future!

So how quickly could I reach that target?

It’d be easy if I won the lottery or inherited $1 million. Then I’d just need to invest in a portfolio of ASX shares with an average dividend yield of 3%.

Every household has a different financial setup, so regularly putting money into the stock market will depend on individual situations. Investing $1,000 per month seems like a nice round target, so I’m going to use that as an example to get us to $1 million.

The share market has returned an average of roughly 10% per annum over the long term. Future returns could be stronger or weaker than that, particularly in the short term.

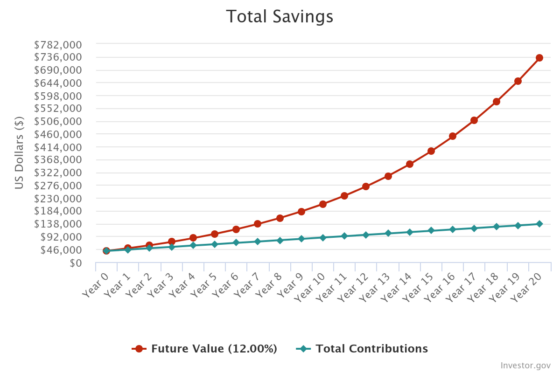

In 24 years, the total value could grow to $1.06 million. With a 3% dividend yield, that’s actually $31,800 of annual passive income. If a 20-year-old could reach that by age 44, they’d be sitting very nicely (financially)!

Do I need to wait 24 years to get $30,000 of annual passive income?

There are a few key ways to build up that cash flow faster.

First, by investing more. In my example, we talked about $1,000 per month. Maybe you can only invest $1,000 per month in the first year, but then circumstances change, and you can invest $2,000 per month. It would take less than 18 years if $2,000 were invested per month.

The second option is to choose investments that could deliver stronger growth. I regularly write about ASX shares I think are capable of producing returns that could beat the market.

FiThe third option is to choose investments with a higher dividend yield. I’ve assumed the dividend yield for the portfolio will be 3%. But there are plenty of businesses with much higher dividend yields.

Keep in mind that higher-yielding ASX shares could reduce their passive income and company growth rate (because it’s not keeping as much money available to invest for growth).

Having said that, a portfolio with an average yield of 6% would mean the portfolio only needs to reach $500,000. That’s half the size!

Reaching $500,000 is a much more achievable total. Going for higher-yield stocks may sacrifice some growth, but we can re-invest the dividends received into more shares and build wealth using compounding.

The post How quickly could I build a $30k annual passive income with ASX shares? appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 10 November 2023

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- At 20x earnings and a 4% yield, surely I can’t ignore this ASX 200 stock?

- Brokers say buy these ASX 200 dividend stocks with juicy yields

- Why I think Lovisa stock is an amazing ASX 200 buy for both dividends and growth

- If I invested $10,000 into Pilbara Minerals shares 10 years ago, I would haveâ¦

- Retirees: 2 Top ASX dividend shares I’d buy now for passive income in 2024

Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/AhZWYIn