Itâs a good day to be an owner of Woodside Energy Group Ltd (ASX: WDS) shares.

Thatâs because it is payday for eligible shareholders, with the energy giantâs monster dividend hitting bank accounts today.

The Woodside dividend

In February, Woodside released its full-year results for FY 2022. These were the first set of results since its merger with the petroleum assets of BHP Group Ltd (ASX: BHP).

Thanks to a combination of merger benefits (increased volumes), higher realised prices, and a strong operational performance, Woodside reported a 142% increase in operating revenue to US$16,817 million.

Things were even better on the bottom line, with Woodsideâs profits more than tripling over the 12 months. It posted a 223% increase in underlying net profit after tax to a record of US$5,230 million.

However, given its increased share count from the BHP merger, its dividends per share didnât grow as quickly as its earnings. Though, that doesnât mean it didnât pay a bumper final dividend!

The Woodside final dividend came in 37% higher year over year at a record of US$1.44 per share. This brought its full-year dividend to US$2.53 per share, which was an increase of 87% year over year and represents a total distribution of US$4,804 million.

The US$1.44 (A$2.154) per share final Woodside dividend that is being paid today equates to a sizeable 6.3% yield based on its current share price. Not bad at all!

Whatâs next?

The good news is that the Woodside dividend looks set to remain a very attractive option for income investors in the coming years.

According to a note out of Citi, it is forecasting the following fully franked dividends:

FY 2023: $2.63 per share

FY 2024: $2.56 per share

FY 2025: $2.21 per share

This will mean dividend yields of 7.7%, 7.5%, and 6.5%, respectively, over the next three financial years.

Should you invest $1,000 in Woodside Petroleum Ltd right now?

Before you consider Woodside Petroleum Ltd, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Woodside Petroleum Ltd wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/gy1CiMj

Over decades, Warren Buffett has constructed a portfolio of some of the greatest long-term compounders in modern America. The monumental success has attracted countless aspiring investors who wish to emulate his vast fortunes by uncovering Buffettesque investments.

The legendary stock picker has amassed a fortune of more than US$100 billion by diligently applying a value investing approach at Berkshire Hathaway — the conglomerate holding company of which he is chair and CEO.

But, what if you wanted to build a similar portfolio with shares from within the S&P/ASX 200 Index (ASX: XJO)?

Whether the reason behind a domestic desire is grounded in taxes, fees, area of competence, or something else entirely — here’s how I would go about building an Aussie version of the Berkshire portfolio.

What does Warren Buffett hold in the Berkshire portfolio?

The initial step in taking inspiration from an existing portfolio is to first find the blueprint. Fortunately, this isn’t difficult due to Berkshire Hathaway being required to report its holdings to the US Securities and Exchange Commission on a regular basis.

Based on currently available information (as of 4 April 2023), the US$682 billion investment company holds the following listed investments.

It should be noted that the above list does not include businesses that are solely owned by Berkshire Hathaway. Examples of such companies are GEICO and Berkshire Hathaway Primary Group, among many others.

Berkshire’s top 20 largest positions make up 94% of the total portfolio. I have disregarded the 34 smaller investments given their near-negligible overall impact.

Furthermore, owning 54 positions as an individual investor is a daunting and unnecessary undertaking in my opinion. Hence, my objective of an Aussie alternative will be centred around the 20 main contributors.

Building an alternative with ASX 200 shares

Now that we know what we’re aiming for, it’s time I put in the leg work and find worthy ASX-listed replacements… which is easier said than done in some cases.

Nevertheless, here’s how I would apply the fundamentals of the Warren Buffett curated portfolio to stocks residing in the land down under.

Structuring the portfolio

Buffett is quoted as saying, “Diversification is a protection against ignorance. It makes very little sense for those who know what they’re doing.”

It appears the Oracle from Omaha practices as he preaches — holding roughly 75% of Berkshire’s portfolio in just five companies.

Selecting the top 5 heavy lifters

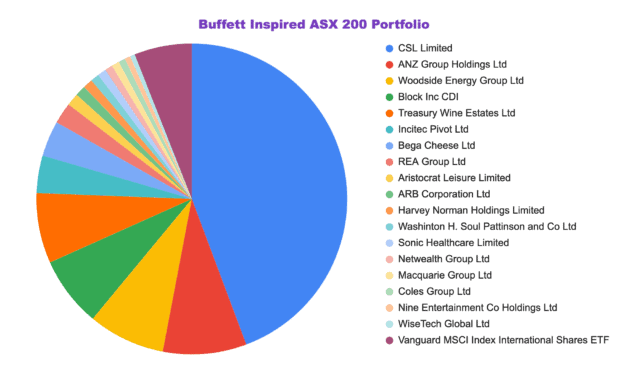

It goes without saying, the ASX 200 stand-ins need to be some of the highest-quality listed businesses Australia can offer to earn such a substantial weighting. Especially the top holding, Apple, which alone accounts for a 44.3% portion.

In my opinion, there simply isn’t an ASX share of the same calibre as the US tech giant. It wields the strongest and most recognisable brand on the planet; is highly profitable; attracts wealthy customers; and sells extremely sticky products and services.

However, consider the graphic below:

Note: These are my own personal selections and should not form the basis of an investment.

As shown above, I landed on CSL Limited (ASX: CSL) as the most fitting Australian substitute for Apple. While the two companies are worlds apart in what they do, there are similiarities. The overlap exists in their hard-to-disrupt nature, thick profit margins, diverse product offerings, and future growth potential.

The second-largest position I would award to ANZ Group Holdings Ltd (ASX: ANZ). Like Bank of America, ANZ has a similar degree of operating leverage to its peers, yet trades at a discounted earnings multiple to the other big four banks.

Moving along, the third, fourth, and fifth largest positions would go to Woodside Energy Group Ltd (ASX: WDS), Block Inc CDI (ASX: SQ2), and Treasury Wine Estates Ltd (ASX: TWE). The reasons are as follows:

Woodside holds the financial firepower to conduct share buybacks if it so chooses. A likely reason for Warren Buffett adding Chevron to the Berkshire portfolio.

Block, formerly Square, is pioneering modern financial solutions with a loyal and growing customer base. Not too dissimilar to the origins of the American Express card in the late 1950s.

Treasury Wine Estates owns a variety of established and recognisable brands, commanding premium margins over its peers. The ASX 200 alcoholic beverage maker offers a dividend yield of 2.6%.

That’s three-quarters complete already.

What about the rest?

There are still another 15 ASX companies as part of this investing mimicry. Though, I would probably need to write a book to explain the reasoning behind all the selections. So, let’s concentrate on one of the more obscure picks.

In place of Occidental Petroleum, I would opt for the fertiliser and chemicals manufacturer — Incitec Pivot. Both companies operate in cyclic industries but have demonstrated hefty operating leverage in the past year.

Additionally, both companies are trading on earnings multiples of six times or less. If the commodities boom can be sustained for even a few more years, current valuations might appear cheap in hindsight. That’s a frame of thinking that might explain Warren Buffett’s large positions in Occidental and Chevron.

Which Warren Buffett picks I think are irreplaceable

I’d like to think I’ve picked a handful of reasonable alternatives among our ASX 200 shares. However, there are some US counterparts that I’d insist are simply unmatchable in what they offer investors.

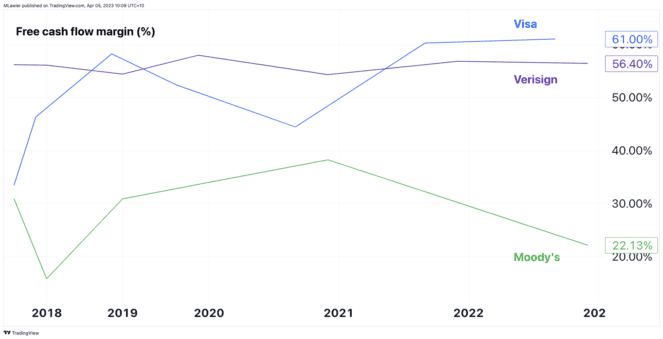

From my perspective, companies that fall into this category include Moody’s, Verisign, and Visa. All three command breathtakingly wide moats, mindblowing free cash flows (see above), and returns on equity that would make your head spin.

For those reasons, if I were to make a few exceptions from staying within the confines of Australia, those would be the three Warren Buffett finds I’d happily duplicate.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Citigroup is an advertising partner of The Ascent, a Motley Fool company. American Express is an advertising partner of The Ascent, a Motley Fool company. Bank of America is an advertising partner of The Ascent, a Motley Fool company. Motley Fool contributor Mitchell Lawler has positions in Apple, Block, Macquarie Group, and Sonic Healthcare. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended ARB Corporation, Activision Blizzard, Apple, Bank of America, Block, CSL, HP, Harvey Norman, Moody’s, Netwealth Group, Vanguard Msci Index International Shares ETF, VeriSign, Visa, Washington H. Soul Pattinson and Company Limited, and WiseTech Global. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has recommended Kraft Heinz and has recommended the following options: long January 2024 $47.50 calls on Coca-Cola. The Motley Fool Australia has positions in and has recommended Block, Coles Group, Harvey Norman, Macquarie Group, Netwealth Group, Washington H. Soul Pattinson and Company Limited, and WiseTech Global. The Motley Fool Australia has recommended ARB Corporation, Activision Blizzard, Apple, Nine Entertainment, REA Group, Sonic Healthcare, Treasury Wine Estates, and Vanguard Msci Index International Shares ETF. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/VIhKCO1

The Coles Group Ltd (ASX: COL) share price beat the S&P/ASX 200 Index (ASX: XJO) return quite significantly in the first quarter of 2023.

Coles shares have risen by around 10.6% in the first three months, while the ASX 200 has gone up by 4.2%.

It has been a strong start for the company, more than doubling the performance of the index.

What has happened to the Coles share price?

The most important thing that the company has announced since the start of the year was its FY23 half-year announcement.

Investors often like to value a business based on how much profit itâs generating and expected to make. The business was able to reveal a good amount of growth for the first six months of the financial year.

Seeing growth in all of those financial metrics is a good sign for the business and it also showed that each of the profit lines grew faster than the profit level above it â EBIT grew faster than EBITDA, NPAT grew faster than EBIT. Itâs helpful to see scale benefits coming through for the company.

The business has managed to get through this period of high inflation â Colesâ supermarkets gross profit margin improved by 43 basis points (0.43%) to 26.5%.

Coles also revealed that in terms of the outlook, that supermarket volume growth returned to âmodestly positiveâ from mid-January. Thatâs a positive sign for earnings growth in the second half of the year.

What is the outlook?

Investors are very future-focused, so commentary about the rest of the year could have been influential for the Coles share price.

It said that supplier input cost pressures âremainâ, but inflation is âexpected to moderate from the peak levelsâ. Coles is expecting more customers will be âvalue consciousâ as cost of living pressures increase.

In the liquor division, itâs expecting earnings growth when itâs no longer competing against the COVID period and itâs focusing on building sales momentum.

The company is expecting to see the benefits of the automated distribution centres, with store deliveries starting in the fourth quarter of FY23 from the Queensland facility and ramping up from that date.

The business said that itâs well positioned and that itâs expecting population growth and moderation in out-of-home dining. These could help investor sentiment about the business.

Coles share price snapshot

While Coles has been rising in recent months, interestingly it is close to the same price that it was a year ago.

Discover one tiny “Triple Down” stock that’s 1/45th the size of Google and could stand to profit as more and more people ditch free-to-air for streaming TV.

But this isn’t a competitor to Netflix, Disney+ or Amazon Prime Video, as you might expect…

Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has positions in and has recommended Coles Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/0PxZw4d

The Novonix Ltd (ASX: NVX) share price is edging higher on Wednesday morning.

At the time of writing, the battery technology companyâs shares are up 0.5% to $1.27.

Though, this isnât going to make any difference to the longer term picture, which looks very ugly.

As you can see on the chart below, Novonix shares are down over 80% since this time last year.

Will the Novonix share price recover?

The company is holding its annual general meeting today and management has taken time to comment on the underperforming Novonix share price.

Novonix chair, Admiral Robert Natter, commented that he believes the performance of the companyâs shares fails to reflect the huge progress being made over the period.

Admiral Natter said:

Clearly, the performance of stock has not reflected the considerable work that is being done with customers and in progressing our graphitization technology and related materials and process technologies. Our share price has gyrated along with the rest of the market and, in particular, the technology sector which has seen even greater volatility. As a battery technology emerging growth company, we have been part of that and felt it to a greater degree than many in our sector.

However, the Novonix chair appears confident that this will change in the future when the company executes on its strategy to deliver its long term goals. He adds:

As we have noted previously, as the Board and management team, we cannot control the share price. What we can control are the decisions we take to ensure we have a sound strategy, and that management is executing that strategy to deliver on our long-term goals. Chris and his team continue to educate the market as to the opportunity that stands before NOVONIX and their progress. Importantly, if we continue to deliver against our key operating milestones, the share price will respond appropriately over time.

Patience may be key here if youâre a believer in the Novonix story.

Should you invest $1,000 in Novonix Limited right now?

Before you consider Novonix Limited, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Novonix Limited wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/O9pTNv8

The Viva Energy Group Ltd (ASX: VEA) share price has climbed to a new multi-year high on Wednesday morning.

At the time of writing, the ASX 200 fuel retailerâs shares are up 5% to $3.24.

Why is the Viva Energy share price scaling new heights?

Investors have been bidding the Viva Energy share price higher today after the company announced a major acquisition.

According to the release, the company has entered into a binding agreement to acquire the OTR Group from Peregrine Corporation for a total consideration of $1.15 billion. Based on estimated earnings and synergies, this represents a 7x EBITDA multiple.

The release notes that the $1.15 billion consideration will be funded through $1 billion of debt and working capital, and an equity component of $150 million to be issued to the sellers.

The deal is expected to deliver earnings per share accretion of 6% on a pro forma FY 2022 basis and 11% on a normalised FY 2022 basis.

What is OTR?

OTR, also known as On the Run, is a leading independent convenience retailer in Australia, generating more than $3 billion of revenue annually and employing approximately 6,500 people.

It comprises OTR Convenience Retail, Smokemart and Giftbox (SMGB), and Mogas Regional and Reliable Petroleum.

The OTR Convenience Retail business is a network of 205 company owned and controlled leasehold stores operating under the OTR brand, comprising 174 integrated fuel and convenience stores and 31 stand-alone stores. It also includes 92 stores which incorporate quick service restaurants (QSRs) operated by OTR.

SMGB provides tobacco and cigarette wholesale arrangements to OTR and other retail third-party networks. Its retail network consists of 257 company owned and controlled leasehold stores across Australia, together with an online retail website.

Finally, the Mogas Regional and Reliable Petroleum wholesale fuel and lubricant businesses service customers in regional South Australia.

Acquisition rationale

Management highlights that this acquisition supports its âvision to be Australiaâs leading convenience retailer, with a pathway to establish more than 1,000 stores.â

It also secures cutting edge convenience capabilities. It highlights that OTR generates over 70% of its earnings from non-fuel retail, which would otherwise have taken the company years to develop. This diversifies its earnings exposure, lifting the share of earnings from non-fuel sources from ~30% (post Coles Express) to an expected ~50%.

In addition, with electric vehicle usage growing, the company believes the deal leaves it well-placed to benefit from the change.

Viva Energyâs CEO and Managing Director, Scott Wyatt, commented:

The introduction of OTRâs superior convenience offering, including quick serve restaurants, will help revolutionise the diversity and attraction of our retail offering. As our stores increasingly become retail destinations, we expect convenience earnings will grow and reduce our dependency on traditional fuels.

OTR outlets offer an attractive and welcoming store environment, supporting increased dwell time, which is likely to be a key factor in successfully introducing electric vehicle recharging facilities over time.

The deal remains subject to customary regulatory approvals including FIRB and ACCC.

Should you invest $1,000 in Viva Energy Group Limited right now?

Before you consider Viva Energy Group Limited, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Viva Energy Group Limited wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/OcMUNVd

If you are looking for some exchange traded funds (ETFs) to buy this month, then it could be worth checking out the ones listed below.

These ETFs have recently been recommended by Betasharesâ chief economist, David Bassanese, as great options in the current uncertain economic environment. They are as follows:

Global Healthcare ETF â Currency Hedged (ASX: DRUG)

The first ETF that has been tipped as a buy is the Global Healthcare ETF.

This ETF provides investors with easy access to the largest global healthcare companies, hedged into Australian dollars.

Bassanese highlights that the largest global healthcare companies are predominantly pharmaceutical companies, which are often considered defensive. Especially considering how they can typically pass rising costs on to consumers. This provides investors with some level of inflation protection.

Among its holdings are healthcare giants such as Astra Zeneca, Johnson & Johnson, Merck & Co, and Pfizer.

Betashares Global Quality Leaders ETFÂ (ASX: QLTY)

Another ETF to look at is the Betashares Global Quality Leaders ETF. It offers investors exposure to a portfolio of approximately 150 global companies (excluding Australia).

To be included in the ETF, a company needs to rank highly on four key metrics. These are return on equity, debt-to-capital, cash flow generation ability, and earnings stability. The ETF includes companies such as Alphabet, LâOreal, Microsoft, Nvidia, and Visa.

Alternatively, thereâs an option you can consider if you would prefer to invest in high-quality ASX shares instead. Bassanesse has suggested investors look at the Betashares Australian Quality ETF (ASX: AQLT). It is currently home to 40 high-quality ASX shares, which includes companies such as biotherapeutics behemoth CSL Limited (ASX: CSL) and telco giant Telstra Group Ltd (ASX: TLS).

Scott Phillips’ ETF picks for building long term wealth…

If you’re an investor looking to harness the sheer compounding power of ETFs, then you’ll need to check out this latest research from 25-year investing veteran Scott Phillips.

He’s painstakingly sorted through hundreds of options and uncovered the small handful he thinks are balanced and diversified. ETFs he thinks investors could aim to hold for years, and potentially build outstanding long term wealth.

Motley Fool contributor James Mickleboro has positions in CSL. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended CSL. The Motley Fool Australia has positions in and has recommended Telstra Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/AGbXUzu

Are you looking for ASX 200 dividend shares to buy? If you are, then you may want to check out the two listed below that have recently been named as buys.

Hereâs why brokers rate these dividend shares highly right now:

The first ASX 200 dividend share that has been named as a buy is big four bank NAB.

The team at Goldman Sachs is positive on NAB and has named it among its top two picks.

Goldman likes NAB in the current environment due to its exposure to commercial lending. Its analysts highlight that they âsee volume momentum over the next 12 months as favouring commercial volumes over housing volumes” and note that “NAB provides the best exposure to this thematic.â

The broker currently has a buy rating and $35.42 price target on its shares.

In respect to dividends, Goldman is forecasting fully franked dividends of $1.73 per share in FY 2023 and $1.76 per share in FY 2024. Based on the current NAB share price of $28.07, this implies yields of 6.15% and 6.3%, respectively.

Another ASX 200 dividend share that has been named as a buy is Wesfarmers.

It is the conglomerate behind a range of businesses such as Bunnings, Kmart, Officeworks, and Priceline.

The team at Morgans are positive on Wesfarmers in the current environment. This is due to its value offering. The broker highlights that âKmart is well-placed to benefit with the average price of an item at around $6-7.â

As for dividends, its analysts are forecasting fully franked dividends per share of $1.79 in FY 2023 and $1.92 in FY 2023. Based on the current Wesfarmers share price of $51.50, this will mean yields of 3.5% and 3.7%, respectively.

Morgans has an add rating and $55.60 price target on Wesfarmersâ shares.

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has positions in and has recommended Wesfarmers. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/2uOUPEk

The NIB Holdings Limited (ASX: NHF) share price has only risen by 15% in the last five years. Could the next five years be a lot better for the private health provider?

One of the main things that have happened in the past five years is that NIB has diversified its sources of earnings.

The business has managed to grow its Australian resident policyholders at a much stronger rate than the wider industry over the long term. It also has other segments including âinternational inbound health insuranceâ, a New Zealand business and travel insurance.

Thereâs one area in particular where the business thinks there is strong growth potential for the company to pounce on â the NDIS. NIB has a division called Thrive which it thinks has lots of potential.

Significant marketplace

According to NIB and the NDIS quarterly report for June 2022, the NDIS âmarketplaceâ was worth $29 billion in FY22, with plan management and support co-ordination worth over $1 billion.

The company noted that it has long and deep experience in connecting buyers and sellers of healthcare, itâs a well-known and trusted brand, and it has technology advantages.

NIB suggests that it has the capacity to lead orderly consolidation, improve efficiencies and integrity.

In the first half of FY23, it raised $158 million to make acquisitions in the NDIS space.

It has also entered into an agreement to acquire plan manager All Disability Plan Management, based in Port Macquarie, which has about 3,000 participants.

The company said that itâs considering further acquisitions.

NIB Thrive is expecting to manage plans for 50,000 NDIS participants by FY25. The ASX share said that the NDIS is expected to double in size by 2030, which may be a very positive sign for the NIB share price in the next five years and beyond.

Other aspects of the business are promising

With borders now open after COVID, the business is benefiting from the increased availability of travel. As more international travel occurs, I think this business will see improved earnings from higher volumes.

The international student volumes are strongly rebounding, while international workers are also adding to NIBâs growth.

NIB is hoping to keep growing its policyholder numbers. Hospital claims are expected to remain subdued in the second half of FY23, though conditions (including margins) are expected to normalise as time goes on.

Is the NIB share price good value?

According to estimates on Commsec, NIB could generate 43.2 cents of EPS in FY25. This would put NIB shares at under 17 times FY25âs estimated earnings. I think thatâs a reasonable valuation considering the business is expected to grow both its EPS and dividend in each of the next few years.

I think it can keep growing its policyholders and profit, making it an attractive option for the next five years and perhaps beyond.

Should you invest $1,000 in Nib Holdings right now?

Before you consider Nib Holdings, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Nib Holdings wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor Tristan Harrison has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has recommended NIB Holdings. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/mQKG8v4

The Qantas Airways Limited (ASX: QAN) share price has put on a rollercoaster performance over the last five years. Meanwhile, the airline operator battled through the onset of, and its recovery from, the COVID-19 pandemic.

If one were to have invested $8,000 in Qantas in early April 2018, they likely would have walked away with 1,322 shares, paying $6.05 apiece.

Today, that parcel would be worth $8,976.38. The Qantas share price has gained 12% over the last five years to trade at $6.79 as of Tuesdayâs close.

For comparison, the S&P/ASX 200 Index (ASX: XJO) has risen 25% in that time.

But what about the dividends on offer from the ASX 200 travel giant? Letâs factor them into the stockâs returns.

All dividends paid to those holding Qantas shares since 2018

Find all the dividends that have been paid to those holding Qantas shares over the last five years below:

Qantas dividendsâ pay date

Type

Dividend amount

September 2019

Final

13 cents

March 2019

Interim

12 cents

October 2018

Final

10 cents

April 2018

Interim

7 cents

Total:

42 cents

As the above chart shows, each Qantas share has yielded just 42 cents in dividends since this time five years ago.

Should you invest $1,000 in Qantas Airways Limited right now?

Before you consider Qantas Airways Limited, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Qantas Airways Limited wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor Brooke Cooper has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/ciKnj7x

Although the JB Hi-Fi Limited (ASX: JBH) share price is having a decent start to 2023, things arenât quite as positive on a longer term basis.

For example, over the last 12 months, the ASX 200 retail giantâs shares are down over 17%, as you can see on the chart below.

This has been driven by concerns that the cost of living crisis could weigh on its sales and earnings in the near term.

There is one positive with this decline, though. That positive is that it has made the potential dividend yield on offer with this ASX 200 stock very attractive.

Should you buy this dirt cheap ASX 200 stock for its big dividend yield?

According to a recent note out of Citi, its analysts believe this is an ASX 200 stock to buy right now.

It has put a buy rating and $55.00 price target on its shares, which implies potential upside of 25% for investors based on the current JB Hi-Fi share price.

In addition, the broker is forecasting a fully franked $3.26 per share dividend in FY 2023, which represents a yield of approximately 7.5%.

What is the broker saying?

Citi acknowledges that JB Hi-Fiâs earnings are likely to peak this year. This is due to its âview that household goods will be among the weaker retail categories given falling house prices and a rotation into travel spending.â

However, it still believes this ASX 200 stock is dirt cheap at the current level. Particularly given its belief that consensus estimates may be too low.

Citiâs analysts âcontinue to see upside risk to consensus expectations given the degree of decline expected in sales (~4%) and margins (~32%) in 2H23e appears inconsistent with the current trajectory of the business.â

The broker is forecasting earnings per share of $4.95 in FY 2023, $3.66 in FY 2024, and then $3.49 in FY 2025. This implies below average price to earnings ratios of 8.9x, 12x, and 12.6x, respectively.

And while this is expected to lead to dividend cuts, the yields on offer are expected to remain very attractive. Citi is forecasting fully franked dividends per share of $2.41 in FY 2024 and then $2.30 in FY 2025. This will mean yields of 5.5% and 5.2%, respectively, for owners of this ASX 200 stock.

Should you invest $1,000 in Jb Hi-fi Limited right now?

Before you consider Jb Hi-fi Limited, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Jb Hi-fi Limited wasn’t one of them.

The online investing service heâs run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has recommended Jb Hi-Fi. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/xXnKauE