The Flight Centre Travel Group Ltd (ASX: FLT) share price fell 17.8% in 2022.

Flight Centre shares closed 2021 trading at $17.62 each and ended 2022 swapping hands for $14.49 apiece.

For some context, the S&P/ASX 200 Index (ASX: XJO) dropped 5.5% over the past calendar year.

So far, the first two trading days of 2023 have been a mixed bag for the Flight Centre share price.

Yesterday, the travel stock closed down 0.7%. In late afternoon trading today, shares are up 1.74% to $14.64.

So whatâs in store for the year ahead?

Is the travel stock set to take off?

Following the past yearâs fall, the Flight Centre share price remains down 59% from where it was shortly before the COVID-fuelled market sell-off.

Yet many ASX 200 investors believe the stock has further to fall.

Flight Centre shares are the most shorted on the Australian share market, with a massive 14.7% of its shares held short.

As my Fool colleague James Mickleboro noted last week, Flight Centre shares were the most shorted on the ASX, with 14.7% of the company’s shares held short on 30 December.

Investors are likely skittish over the companyâs struggles to return to profitability.

After posing hefty losses in FY21, Flight Centre reported a statutory loss before tax of $378 million for FY22. Thatâs a 37% improvement from the losses of the prior year. But still…

Potential headwinds for the Flight Centre share price in 2023 include any significant delays with the global reopening.

The biggest risk there at the moment looks to be China. COVID cases in the Middle Kingdom are skyrocketing following the nationâs reopening last month. This has seen numerous countries, Australia included, reintroduce virus testing for Chinese travellers.

Should the situation come under control in short order, without major disruptions to international travel demand, the Flight Centre share price could be one to benefit.

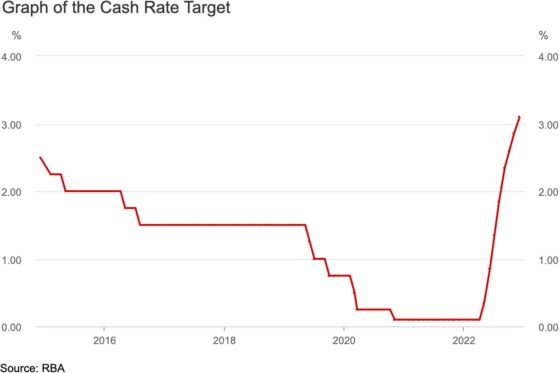

Other headwinds for ASX 200 investors to bear in mind are the impacts of further interest rate hikes and continuing high inflation. Both of these will see consumer spending power eroded by more than any expected wage increases in 2023.

And at the end of the day, air travel â pent-up demand or not â will take a back seat to making mortgage payments. Or fuelling up the family car.

With that said, a number of brokers, while not actively recommending Flight Centre, have a positive outlook on its share price.

Macquarie has a price target of $17.35; Citi has a price target of $16.60; and Goldman Sachs has a price target of $16.10. All three brokers have a neutral rating on Flight Centre shares.

The stock is currently trading for $14.64 per share.

How has the Flight Centre share price performed longer-term?

As mentioned up top, and shown in the chart below, the Flight Centre share price dropped 18% in 2022.

Longer-term investors who snapped up shares in the travel stock on 19 March 2020, following the sharp pandemic fire sale, are sitting on gains of 64%.

The post The Flight Centre share price nosedived 18% in 2022. Is it preparing for take-off in 2023? appeared first on The Motley Fool Australia.

FREE Investing Guide for Beginners

Despite what some people may say – we believe investing in shares doesn’t have to be overwhelming or complicated…

For over a decade, we’ve been helping everyday Aussies get started on their journey.

And to help even more people cut through some of the confusion “experts’” seem to want to perpetuate – we’ve created a brand-new “how to” guide.

Yes, Claim my FREE copy!

*Returns as of November 7 2022

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- What could gas caps mean for the Woodside share price?

- ANZ shares were slaughtered in 2022. Does the new year bring fresh hope?

- Forget gold! Hereâs why Iâd buy ASX 200 dividend shares to hedge against inflation

- 5 things to watch on the ASX 200 on Wednesday

- Broker tips significant upside for the Woodside share price

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has recommended Flight Centre Travel Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/2qOI5mx