The case for raising interest rates further strengthened this week when the United States announced a 40-year high for inflation at 9.1%, which was well beyond consensus expectations. We also found out that the Australian jobs market is even tighter with unemployment falling again to a 48-year low of just 3.5%.

During times of increasing uncertainty and volatility, many investors gravitate to ASX dividend shares for their potential to deliver regular returns that may outperform share price gains.

On that note, we asked our Foolish contributors to compile a list of ASX dividend shares that they reckon could make great buying for income investors in July. Here is what the team came up with.

8 best ASX dividend shares for July 2022 (smallest to largest)

Dusk Group Ltd (ASX: DSK), $123.9 million

AUB Group Ltd (ASX: AUB), $1.7 billion

Dicker Data Ltd (ASX: DDR), $2.15 billion

Charter Hall Long WALE REIT (ASX: CLW), $3.17 billion

Wesfarmers Ltd (ASX: WES), $51.83 billion

Macquarie Group Ltd (ASX: MQG), $65.48 billion

Westpac Banking Corp (ASX: WBC), $69.64 billion

National Australia Bank Ltd (ASX: NAB), $90.38 billion.

(Market capitalisations as of 14 July 2022)

Why our Foolish writers love these ASX dividend shares

Dusk Group Ltd

What it does: Dusk is a retailer that specialises in candles, fragrances, and other homewares.

By Sebastian Bowen: Dusk is one of those companies that boomed during COVID but now seems to have lost favour with investors.

Although the company has staged something of a comeback in the past month, it remains down more than 35% over the year to date. However, this steep fall has pushed Dusk’s dividend yield up substantially.

On recent pricing, Dusk shares offer a fully franked yield of more than 9.5% (or 13.5% grossed-up).

Even if Dusk has to trim its dividends this financial year (which is very possible), that 9.5% gives the company a lot of wiggle room to still offer investors a very attractive yield going forward.

Motley Fool contributor Sebastian Bowen owns shares in Dusk.

AUB Group Ltd

What it does: The AUB Group has been in the business of insurance brokering and underwriting since 1985. Over the years, the AUB network has grown extensively to more than 500 locations across Australia and New Zealand. The companyâs operations are segmented into seven areas, including Australian broking, non-broking services, underwriting agencies, and BizCover.

By Mitchell Lawler: Interest rates are on the rise. In such times it becomes paramount that the ASX dividend shares we hold are offering meaningful upside over cash, given their added risk.

The AUB Group is in a position that appears relatively defensive in a tightening environment. Although the company operates in the insurance industry, it deals primarily with the brokering portion.

Considering recent natural disasters and the increasing cost of living, brokers such as AUB might benefit from customers wanting to weigh up their options.

At present, AUB provides a dividend yield of approximately 3% — still more than double most savings accounts at the moment.

Motley Fool contributor Mitchell Lawler does not own shares in AUB Group Ltd.

Dicker Data Ltd

What it does: Dicker Data is an Australian technology hardware, software, and cloud distributor. It exclusively sells a wide portfolio of products from the worldâs leading technology vendors including Dell Technologies, Hewlett Packard, and Microsoft to more than 8,200 resellers.

By Aaron Teboneras: The Dicker Data share price has continued to travel higher since the start of the month, up 14.6%.

The company is expected to reveal its next quarterly dividend in the upcoming earnings season in August.

For the first interim dividend declared on 11 May, Dicker Data paid 13 cents per share to eligible shareholders.

With the company previously proposing to maintain its dividend policy, this could be a good option for income investors.

The total dividends expected to be paid this year are 54 cents per share, an increase of 44%. This includes the final dividend of 15 cents per share paid in March.

Based on the share price at the time of writing, Dicker Data has a trailing dividend yield of 3.69%.

Motley Fool contributor Aaron Teboneras owns shares in Dicker Data Ltd.

Charter Hall Long WALE REIT

What it does: Charter Hall Long WALE REIT is a real estate investment trust (REIT) that owns a diversified portfolio of properties across a number of different sectors. These include agri-logistics, social infrastructure, office, industrial and logistics, retail, service stations, and hospitality. The REIT says 99% of its tenants are blue chip, being government, ASX-listed, multinational, or national companies.

By Tristan Harrison: The REIT has a net tangible asset (NTA) per unit of $6.08 after its latest quarterly update, so the current Charter Hall Long WALE REIT share price is at a 27% discount to this.

It has a long weighted average lease expiry (WALE) of around 12 years, meaning the business has long-term income security and visibility, in my opinion.

Income growth is driven by annual rent increases on all leases, with 46% linked to CPI inflation and 54% with an average fixed increase of 3.1%.

The estimated distribution of at least 30.5 cents in FY22 translates to a forward yield of 6.9%.

Motley Fool contributor Tristan Harrison does not own shares in Charter Hall Long WALE REIT.

Wesfarmers Ltd

What it does: Wesfarmers is a diversified company with a large retail portfolio including many top names like Bunnings Warehouse, Kmart, Target and Officeworks. The company also has energy & fertiliser and industrial divisions.

By Bernd Struben: Wesfarmers has long been a reliable dividend payer, making two annual payments even throughout the 2020 pandemic crunch.

Over the past five years, the company has paid out $10.49 in fully franked dividends. In FY22, it paid out $1.70, giving it a current trailing dividend yield of 3.8%.

In the first half of FY22, Wesfarmers earned $17.6 billion in revenue, with 51% of that coming from Bunnings. Yet investors pushed down the share price amid sliding profits due to pandemic headwinds. Net profit after tax (NPAT) in H1FY22 was down 14% year over year.

With the pandemic hopefully fading, and Wesfarmers expanding its reach with a new health division, this is an income stock to consider.

Motley Fool contributor Bernd Struben does not own shares in Wesfarmers.

Macquarie Group Ltd

What it does: Macquarie is a financial services giant. It provides banking, asset management, and advisory services.

By Brooke Cooper: Macquarie is an S&P/ASX 200 Index (ASX: XJO) staple and one of the marketâs largest companies. Itâs also been tipped as a long-term winner by broker Morgans, The Motley Fool Australiaâs James Mickleboro recently reported.

The broker likes the companyâs exposure to infrastructure and renewables, as well as its growing position in the Australian mortgage market.

Macquarie is currently trading with a yield of around 3.6%, having paid out $6.22 per share in dividends over the past 12 months. And Morgans expects that to grow in the future.

The broker believes the stock will offer investors $7.07 per share in dividends this financial year. It’s also tipping $7.47 per share next financial year.

Motley Fool contributor Brooke Cooper does not own shares in Macquarie Group Ltd.

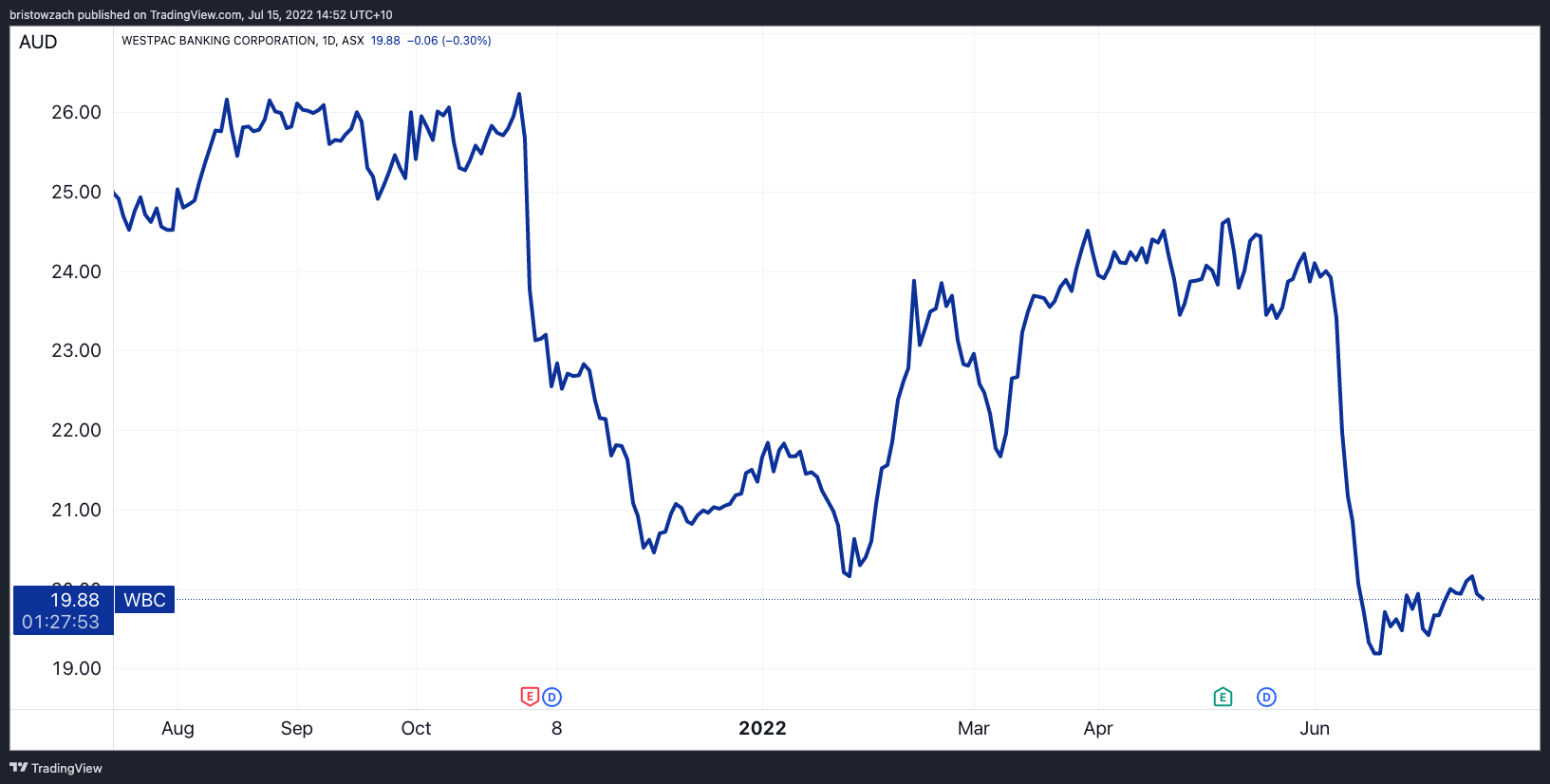

Westpac Banking Corp

What it does: Established in 1817, Westpac is Australiaâs oldest bank. As well as the eponymous Westpac brand, it owns the Bank of Melbourne, Bank SA, RAMS, and St George brands.

By James Mickleboro: It has been a difficult 12 months for this big four bank. Since this time last year, the Westpac share price has lost 20% of its value.

This has been driven partly by concerns that Australia could fall into a recession, which could put pressure on loan growth and bad debts.

While this is disappointing, I think the risks are all known and priced in now and this could be a buying opportunity for investors. Especially those that are looking for attractive yields as inflation rears its ugly head.

Consensus estimates for Westpac dividends are $1.23 per share in FY22, $1.29 per share in FY23, and then $1.46 per share in FY24.

Based on the current Westpac share price, this will mean yields of about 6.1%, 6.4%, and 7.2% respectively.

Motley Fool contributor James Mickleboro owns shares in Westpac Banking Corp.

National Australia Bank Ltd

What it does: NAB is one of the big four banks in Australia. It provides banking and financial services here in Australia and New Zealand. NAB also has operations in the United Kingdom and the United States. It is valued at a $90.2 billion market capitalisation.

By Zach Bristow: Trading on a respectable 5% trailing dividend yield, the National Australia Bank Ltd (ASX: NAB) share price is another ASX dividend player worth mentioning.

NAB is forecast to print revenue of $20 billion this year, according to Refinitiv consensus data. On this revenue, it is projected to claim around $7 billion in net income. That’s around a 7% year-over-year gain.

That leaves a sizeable amount left over to return to shareholders.

Analysts forecast NAB to pay a $1.48 per share dividend in FY22, with this figure growing to $1.61 in FY23, and $1.73 in FY24, per Refinitiv.

This represents a growth schedule of 16.5%, 8.9%, and 7.4% over these coming two years. That’s well ahead of the current level of inflation.

Motley Fool contributor Zach Bristow does not own shares in National Australia Bank.

The post Top ASX dividend shares to buy in July 2022 appeared first on The Motley Fool Australia.

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.* Scott just revealed what he believes could be the “five best ASX stocks” for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now

See The 5 Stocks

*Returns as of July 7 2022

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#43B02A”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#43B02A”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Dicker Data Limited. The Motley Fool Australia has positions in and has recommended Dicker Data Limited and Wesfarmers Limited. The Motley Fool Australia has recommended Austbrokers Holdings Limited, Dusk Group Limited, Macquarie Group Limited, and Westpac Banking Corporation. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/mwpgtVs