Key points

- Consumer staples shares are often referred to as ‘safe’ shares

- But just how safe are they?

- Let’s crunch some numbers and see how they’ve performed recently

When it comes to investing, a popular opinion that you might come across (especially in times like these) is that consumer staples shares are ‘safe’ investments to hold during a market correction or crash.

If you weren’t aware, a consumer staples company is one whose primary business is producing food, drinks, alcohol, tobacco, or household essentials such as laundry powder, dishwashing detergent, or razor blades. If you can’t live (or live in a modern way) without it, chances are it’s a consumer staples product.

So you can see why some investors would regard a company that is in the business of supplying these kinds of products might be viewed as safe or recession-proof. No matter how bad the economy might get, we all still need to eat, drink, and clean our houses. Many of us would be loath to give up our vices as well.

So here on the ASX, most of our consumer staples companies are middlemen. Think Woolworths Group Ltd (ASX: WOW) or Coles Group Ltd (ASX: COL). Although these companies don’t technically produce most of the products they sell themselves, they still participate in the consumer staples value chain.

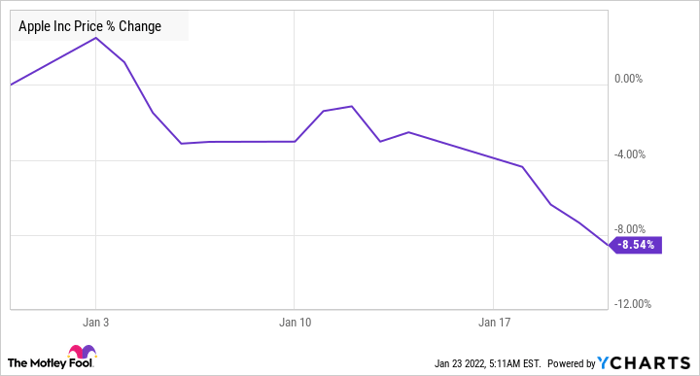

So let’s see how these companies have performed over the past month or so. As most investors would be aware, the past few weeks have been brutal for many ASX investors, with the S&P/ASX 200 Index (ASX: XJO) losing approximately 7.15% year to date in 2022.

Have ASX consumer staples shares protected their owners from the market selloff?

Well, if we take the Woolworths share price, we might be able to get some idea as to how consumer staples shares have performed in a period of market turmoil like we have seen recently.

Since the start of the year, the Woolworths share price has gone from $38.47 to the $34.51. That’s a fall of 10.3% — a performance that handily trails the broader market. What about Coles ? Well, it’s down by very similar amount — 9.9% at the time of writing.

So it’s not looking too good for consumer staples shares thus far.

Let’s take a few more consumer staples shares. There’s Treasury Wine Estates Ltd (ASX: TWE) and Metcash Limited (ASX: MTS). Treasury shares have lost 12.25% since the start of 2022, while Metcash is down 7.5% over the same period. Again, all ASX 200 underperformance.

So, all in all, it seems that ASX consumer staples shares have not delivered their investors any protection from the selloff we have seen on the share market over the year so far. In fact, all of the big consumer staples shares we have discussed today have been crushed by the market during this downturn.

Let’s be clear, there’s nothing wrong with consumer staples shares. But the evidence here clearly shows that they are not immune to underperforming the market in a downturn. It just goes to show that, as Mark Twain once said, ‘what gets us into trouble is not what we don’t know. It’s what we know for sure that just ain’t so’.

The post Are ASX consumer staples shares really ‘safe’ to hold in a market selloff? appeared first on The Motley Fool Australia.

Should you invest $1,000 in Woolworths right now?

Before you consider Woolworths, you’ll want to hear this.

Motley Fool Investing expert Scott Phillips just revealed what he believes are the 5 best stocks for investors to buy right now… and Woolworths wasn’t one of them.

The online investing service he’s run for over a decade, Motley Fool Share Advisor, has provided thousands of paying members with stock picks that have doubled, tripled or even more.* And right now, Scott thinks there are 5 stocks that are better buys.

*Returns as of January 13th 2022

More reading

- 2 ASX dividend shares Morgans rates as buys

- 5 things to watch on the ASX 200 on Tuesday

- Here are the top 10 ASX shares today

- Here are the 3 most heavily traded ASX 200 shares this Monday

- Why are these beaten-up small cap ASX tech shares seeing 52-week lows today?

Motley Fool contributor Sebastian Bowen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia owns and has recommended COLESGROUP DEF SET. The Motley Fool Australia has recommended Treasury Wine Estates Limited. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Bruce Jackson.

from The Motley Fool Australia https://ift.tt/3tTQIv9