One critical action to take if you want your S&P/ASX 200 Index (ASX: XJO) shares to perform better than the market is to invest in stocks that others are ignoring.

After all, if you are only going for investments that everyone else is into, you can’t expect to receive results different from the average.

Shaw and Partners portfolio manager James Gerrish recently told his Market Matters newsletter that consumer staples is the big play for his team in 2024.

“The Australian consumer staples sector has struggled over recent years, but as Market Matters looks to position portfolios more defensively, it’s been on our radar of late,” he said.

“People have to eat.”

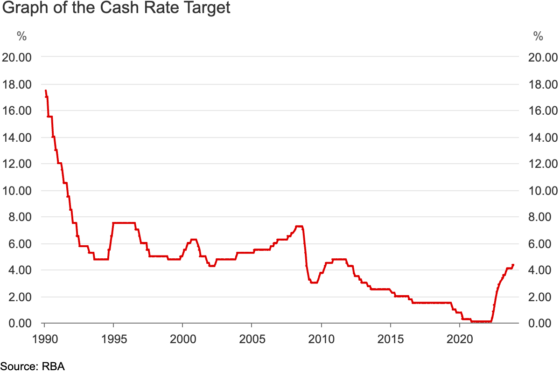

This might be considered a contrarian view, as many experts are forecasting a reduction in interest rates. That would boost public confidence and spending, which would conventionally be considered a boon for the consumer discretionary sector.

But Gerrish likes staples for similar reasons.

“With interest rates set to fall through 2024/5, inflation under control and supply chain issues in the rearview mirror, the outlook has improved for the sector.

“The peak cost of living has passed, with spending growth on the horizon, helped by solid immigration, with supermarkets likely to be a key beneficiary.”

Helpfully, he also picked out two ASX 200 stocks from the industry that are ripe for buying now:

‘An opportunity’ imminent?

On Thursday, groceries distributor Metcash Limited (ASX: MTS) confirmed it is in discussions to acquire the Superior Food Group business from private equity owner Quadrant.

Metcash shares were immediately placed in a trading halt.

Gerrish reckons there could be a major buying opportunity opening up if the $500 million transaction goes ahead.

“Speculation has been around the funding of the purchase, with many expecting a capital raise should the deal progress,” he said.

“At this stage, Metcash has several alternatives from a funding perspective, but if they do undergo a discounted equity raise as part of a wider funding package, it could provide an opportunity in the stock.”

Gerrish’s team is “long and bullish” on the owner of the IGA supermarket brand.

These ASX 200 shares are looking cheap

Woolworths Group Ltd (ASX: WOW) shares have gone largely sideways over the past three years.

With cost-of-living pressures bearing down on many Australian households, politically the company and its rival Coles Group Ltd (ASX: COL) are in strife.

“The ACCC is investigating ‘price gouging’, which will inconvenience Woolworths.”

The Woolies stock price has also dipped this year because of a $1.7 billion write-down of its New Zealand supermarket business.

Gerrish’s team reckons this trough makes the stock “even more attractive”.

“When we saw the banks endure a Royal Commission, it ultimately delivered an excellent buying opportunity.

“If Metcash raises capital, it may create some sentiment selling across the sector.”

His analysts like Woolworths as a buy below $36.

It closed Friday at $36.44.

The post ‘Attractive’: 2 ASX 200 shares to buy right now from the boom sector for 2024 appeared first on The Motley Fool Australia.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

See The 5 Stocks

*Returns as of 10 November 2023

(function() {

function setButtonColorDefaults(param, property, defaultValue) {

if( !param || !param.includes(‘#’)) {

var button = document.getElementsByClassName(“pitch-snippet”)[0].getElementsByClassName(“pitch-button”)[0];

button.style[property] = defaultValue;

}

}

setButtonColorDefaults(“#0095C8”, ‘background’, ‘#5FA85D’);

setButtonColorDefaults(“#0095C8”, ‘border-color’, ‘#43A24A’);

setButtonColorDefaults(“#fff”, ‘color’, ‘#fff’);

})()

More reading

- Top brokers name 3 ASX shares to buy next week

- Top ASX dividend shares to buy in February 2024

- Guess which ASX 200 stock is halted on $500m acquisition talks

- Top brokers name 3 ASX shares to buy today

- How big could the 12-month return be on Woolworths shares?

Motley Fool contributor Tony Yoo has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has positions in and has recommended Coles Group. The Motley Fool Australia has recommended Metcash. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/of6Lt3c