This online luxury retailer could be an ASX growth share to buy according to analysts at Bell Potter.

The broker believes Cettire could be a top option due to its strong long term growth outlook in a huge market. The broker explains:

Cettire has a rapidly growing global online luxury personal goods retailing platform in a large market with a structural shift to online well underway. We believe CTT will continue to outperform its peer group consisting of global luxury retailers and local e-commerce players given its <1% market share in a growing market, which could remain more resilient than other discretionary categories in a likely recessionary environment.

Bell Potter currently has a buy rating and $4.00 price target on its shares.

Another ASX growth share that analysts are bullish on is Lovisa.

Morgans is a fan of the growing fashion jewellery retailer. This is because it believes Lovisa is well-positioned to continue its strong growth over the long term thanks to the popularity of its offering and its large global expansion opportunity. It said:

LOV grew substantially in FY23 to finish the year with an 801-store network in 39 countries. We believe it plans to enter mainland China in FY24, paving the way for significant longer-term growth. We have increased our finance cost estimates in FY24 and FY25, leading to 7% and 3% lower forecast NPAT. We have increased our long-run earnings estimates.

The broker has an add rating and $27.50 price target on its shares.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has positions in Lovisa. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Lovisa. The Motley Fool Australia has recommended Cettire and Lovisa. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/JPx0Fr9

If you’re not a fan of stock picking, then exchange-traded funds (ETFs) could be the answer.

That’s because they provide investors with access to large numbers of ASX shares through a single click of the button. This means that you can diversify a portfolio almost instantly.

The good news for income investors is that there are plenty of options for them out there.

For example, two ASX ETFs that offer a source of income and could be worth considering are listed below. Here’s what you need to know about them:

This is a low-cost, diversified, index-based exchange-traded fund that aims to track the ASX 300 index.

This index is home to Australia’s leading 300 listed companies. This includes shares such as BHP Group Ltd (ASX: BHP), Macquarie Group Ltd (ASX: MQG), Newmont Corporation (ASX: NEM), and TPG Telecom Ltd (ASX: TPG).

And while not all members of the index pay dividends, the ETF still trades with an attractive dividend yield of 3.8%.

Vanguard Australian Shares High Yield ETF (ASX: VHY)

This popular ETF gives investors low-cost exposure to a group of 70+ ASX shares that are forecast to have bigger dividend yields compared to the market average.

This includes all the big names such as companies like BHP and Commonwealth Bank of Australia (ASX: CBA), as well as smaller names like Dicker Data Ltd (ASX: DDR) and Lottery CorporationLtd (ASX: TLC).

Importantly, Vanguard limits how much it invests in any particular industry or company to ensure that you’re holding a truly diverse group of shares.

The Vanguard Australian Shares High Yield ETF currently trades with a dividend yield of 5.1%.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Dicker Data, Lottery, and Macquarie Group. The Motley Fool Australia has positions in and has recommended Dicker Data and Macquarie Group. The Motley Fool Australia has recommended Tpg Telecom and Vanguard Australian Shares High Yield ETF. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/bLYutcB

In an article published on Friday, Marc Jocum from Global X said thematic ETFs provided a great way to invest in megatrends with less risk.

He commented:

Predicting what will happen in the short-term is challenging given the constantly evolving market environment.

However, if investors extend their time horizons to multiple years, they can be prepared for a future marked by long-term structural shifts known as “megatrends”.

Jocum said megatrend investing was all about long-term thematics. He said the idea was to invest in powerful, potentially transformative global trends that are set to play out over years and decades.

ASX ETFs and the 3 investment megatrends of 2024

Artificial intelligence

Jocum said ChatGPT was a catalyst for investor interest in AI in 2023, but it had only scratched the surface.

He commented:

AI is at a crucial juncture in its adoption cycle … Global X believes sales growth across the AI category can potentially exceed 50% in the year ahead, well above the 5% sales growth expected in the broader share market.

The addressable market for AI services, including the full ecosystem of hardware, software, and data, is set to expand in the coming years, estimated to grow by double digits to $1.6 trillion by 2028.

Jocum said identifying individual stocks set to benefit from the AI trend was difficult. He said some companies may not be able to leverage AI capabilities without undermining traditional revenue streams.

For diverse exposure to this megatrend, investors may consider exploring exchange traded funds (ETFs) that track a basket of artificial intelligence benefactors, semiconductor companies or technology stalwarts.

ASX ETFs offering exposure to the AI megatrend include:

ASX ETF

Share price

Growth over 12 months

Global X Robo Global Robotics & Automation ETF (ASX: ROBO)

$74.10

8.5%

Betashares Global Robotics and Artificial Intelligence ETF (ASX: RBTZ)

$13.41

26.5

Uranium and ASX ETFs

Jocum explained that nuclear energy had become a key element in the world’s green energy transition.

He said:

At the 2023 United Nations Climate Change Conference (known as COP28), a declaration was signed among 22 countries to triple nuclear energy capacity globally by 2050.

It also invited international financial institutions (such as the World Bank) to encourage the inclusion of nuclear energy in lending policies.

The uranium price has skyrocketed by 112% over the past 12 months to US$106 per pound on Friday.

Many countries are building nuclear reactors to supplement their domestic energy supply.

Miners are firing up uranium assets that were previously on care and maintenance for years.

Jocum said:

An important distinguishment between a ‘fad’ and a long-term structural theme is whether there are strong governmental or institutional initiatives.Â

Considering climate change is at the front of minds for global nations, combined with favourable momentum in public and private markets, the uranium industry is positioned to grow …

He said Australia has lots of uranium but only delivered 8% of global production. This is because mining is banned in most states.

He commented:

Investors wanting to get exposure to the uranium decarbonisation theme should expand their investment universe to consider global players …

As uranium lacks a liquid spot market like gold and copper, investors could consider investing in an ETF tracking a broad range of global companies involved in uranium mining and the production of nuclear components.

ETFs offering exposure to the uranium megatrend include:

Jocum said China’s economic weakening in 2023 had led to a changing of the guard in emerging markets:

… investors are looking past China, with eyes locked on India as the bright star of emerging markets.

In Global X’s opinion, India has emerged as one of the better structural opportunities backed by significant economic, social and political drivers. This changing of the guard in the emerging market leader is a monumental shift in the investment landscape.

Jocum said that 10 years ago, India accounted for just over 5% of the emerging markets sector. That has now tripled to 16%. By contrast, China’s market share has contracted by a third since the pandemic.

Jocum said global companies like Apple Inc (NASDAQ: AAPL) were diversifying their supply chains from China to India. This could lead to further infrastructure development and economic growth.

Traditionally, Australian investors looking for exposure to India had to invest through instruments like mutual funds as many brokers cannot access Indian equities.

However, with the average Indian mutual fund charging 1.2% in fees and the fact that most active funds underperform the market over the long-term, investors can look to pay a fraction of the cost and get exposure to an Indian share market index like the NIFTY 50.

ETFs offering exposure to the emerging markets megatrend include:

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bronwyn Allen has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Apple. The Motley Fool Australia has recommended Apple and Betashares Global Uranium Etf. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/ZRdacPY

First, I want to feel comfortable that the company is going to continue paying market-beating yields in the year ahead.

I’d also strongly preference companies paying fully franked dividends. That way, I should be able to hold onto more of that passive income at tax time.

Why I’d snap up New Hope shares for passive income

On the back of elevated coal prices, New Hope has been a leading yielder among ASX 200 dividend stocks in both 2022 and 2023.

Despite coal prices and New Hope’s dividends coming down in 2023, the miner still paid a fully franked interim dividend of 40 cents per share on 3 May. New Hope paid eligible investors the final dividend of 30 cents per share on 7 November. That equates to a full-year payout of 70 cents per share.

New Hope’s recent share price of $5.33 sees this ASX 200 dividend stock trading at a fully franked yield of 13.1%.

Can the ASX 200 dividend stock maintain this high yield?

The 13.1% yield we calculated above, and the dividend yields you generally see quoted, are trailing yields. Future yields may be higher or lower, depending on a range of company-specific and macroeconomic factors.

For New Hope, the coal price is obviously key. But with thermal coal prices already down some 50% over the past year, I believe 2024 should see prices stabilise or even tick up from here.

And if the New Hope share price rises over the coming months, its trailing yield will fall. However, the realised yield for investors who buy in at today’s prices won’t be impacted.

As for why I remain optimistic about the outlook for passive income for this ASX 200 dividend stock, we turn to the miner’s most recent quarterly update, which covered the three months to 31 October.

Over the quarter New Hope produced two million tonnes of saleable coal. That was up 1% from the prior quarter, and it puts the company on track to meet its FY 2024 guidance.

Impacted by the slumping coal price, New Hope’s underlying earnings before interest, taxes, depreciation and amortisation (EBITDA) dropped 8.5% quarter on quarter to $245 million.

But the company’s balance sheet remains very strong.

New Hope reported closing cash and cash equivalents of $812 million. That was before paying out the final dividends.

And the ASX 200 dividend stock is getting a boost from higher interest rates. New Hope said it was “now earning material net interest income on its positive cash balances”.

That leaves the miner well-funded to finance a range of maintenance and infrastructure projects to support its future planned production ramp-up.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Bernd Struben has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/xz49rjH

Bell Potter thinks investors should be buying this footwear focused retailer’s shares.

It currently has a buy rating and $2.35 price target on them. This implies potential upside of 12.5% for investors over the next 12 months.

In addition, the broker is forecasting an 11.1 cents per share dividend in FY 2024. This equates to a yield of 5.3%, which boosts the total potential return to approximately 18%.

Analysts at Goldman Sachs believe that this insurance giant’s shares could offer big returns over the next 12 months. This is thanks to favourable tailwinds and strong premium increases in the insurance market.

Goldman has a buy rating and $18.52 price target on the ASX dividend share, which suggests potential upside of 14.5%.

And with Goldman forecasting a 59 US cents per share dividend in FY 2024, which equates to a 5.5% yield, the total potential return increases to 20%.

Finally, Citi sees the potential for big returns from the shares of this residential and land lease developer and retail, logistics and office real estate property manager.

It has a buy rating and $5.10 price target on the ASX dividend share, which implies 12% upside from current levels.

In addition, the broker expects a 27 cents per share dividend in FY 2024. This represents a ~6% dividend yield, lifting the total potential return to 18%.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Citigroup is an advertising partner of The Ascent, a Motley Fool company. Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has recommended Accent Group. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/5jMeS2n

I think that buy-and-hold investing is the best way to grow your wealth in the share market.

I’m not alone. Legendary investor Warren Buffett once quipped that his “favourite holding period is forever”.

And you only need to look at the Oracle of Omaha’s success over multiple decades to see how effective the strategy can be.

But not all shares will necessarily make great buy-and-hold investments. So, let’s take a look at three roaring ASX shares that I would happily hold for the next 20 years.

Buy and hold these ASX shares

The first ASX share that I would buy and hold is the family safety app company Life360 Inc (ASX: 360).

Goldman Sachs analysts estimate that the company is “exposed to a US$12bn global TAM with a large opportunity to expand its product suite, grow average revenue per paying circle (ARPPC), increase payer conversion, and lift penetration rates outside of the US.”

This gives Life360 a huge runway for growth over the next couple of decades.

Another ASX share that I would buy for the long term is Nextdc Ltd (ASX: NXT). It is one of the leading data centre operators in the Asia-Pacific region.

With more data going to the cloud, data centre demand is expected to increase materially over the next decade. This should also be boosted further by the rise of generative artificial intelligence (AI) services like ChatGPT.

Goldman Sachs highlights that the “DC industry will benefit from a ‘third wave of demand’ with generative AI requiring 5-10x more compute vs. traditional search.”

This bodes well for NextDC’s earnings growth over the next couple of decades, in my opinion.

Finally, I believe Xero Ltd (ASX: XRO) could be another ASX share to buy and hold for the long term.

This is because the cloud accounting platform provider has a massive global market opportunity and a product that is regarded as the best in its class by many.

Goldman Sachs estimates that Xero’s addressable market comprises more than 100 million small to medium-sized businesses worldwide, or NZ$76 billion in value. This compares to its current subscriber base of approximately 4 million.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has positions in Life360, Nextdc, and Xero. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group, Life360, and Xero. The Motley Fool Australia has positions in and has recommended Xero. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/arkBfUo

ANZ Group Holdings Ltd (ASX: ANZ) shares are traditionally a very popular option for passive income investors.

And it isn’t hard to see why.

Each year, the banking giant shares a sizeable portion of its profits with its shareholders.

This usually means that its shares offer a dividend yield that is well ahead of average on any given year.

But will this remain the case in the future? Let’s find out what sort of passive income a $10,000 investment could generate from ANZ shares.

Passive income from ANZ shares

Firstly, let’s see how many shares you can buy with a $10,000 investment.

With the ANZ share price ending the week at $27.26, investors will end up owning 367 units if they put this amount into the bank’s shares.

Moving onto income, according to a note out of Goldman Sachs, its analysts are expecting the ANZ dividend to come in at a fully franked $1.62 per share in FY 2024.

This means that you would end up with income of $594.54 for the year.

And if you keep holding on the bank’s shares into 2025, you can expect another juicy pay check to come your way.

Goldman is expecting another fully franked $1.62 per share dividend in FY 2025. This will mean another $594.54 passive income boost for the year.

And then for a third year in a row, the broker expects ANZ to pay out $1.62 per share in dividends in FY 2026.

All in all, if Goldman is accurate with its forecasts, this will mean income of almost $1,800 for investors across the next three years from a $10,000 investment.

The broker currently has a buy rating and $27.85 price target on ANZ’s shares.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has no position in any of the stocks mentioned. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/uJ21kKW

Next week the Reserve Bank of Australia (RBA) will be meeting for the first time in 2024 to decide on interest rates.

This meeting comes at a very interesting time given how last week the Australian Bureau of Statistics revealed that inflation continued to ease during the December quarter.

In light of this, the market is now expecting the RBA’s next move for rates will be lower and not higher. This is very welcome news for borrowers.

But what could happen at next week’s meeting? Let’s take a look at what the economics team at Westpac Banking Corp (ASX: WBC) is expecting from the central bank.

Westpac on the RBA and interest rates

According to the bank’s latest weekly economic report, its team expect the RBA to keep its powder dry on Tuesday. Chief Economist, Luci Ellis, said:

The data flow since November has pointed in this direction, and today’s CPI release seals the deal: the RBA will keep the cash rate on hold next week, and it is unlikely to raise rates further this cycle.

And while Ellis has suggested that the central bank’s rhetoric at Tuesday’s meeting may not change as much as borrowers would like, she believes that it may not be long until the RBA will be confident enough to state that inflation is under control. She said:

[The RBA] is unlikely to rule out further rate increases entirely in their post-meeting communication. But the case to raise rate from here is steadily losing traction. We expect that over coming months, further declines in inflation and soft outcomes in the real economy will give the Board enough confidence that inflation will return to target on the desired timetable. They will therefore have scope to reduce some of the current restrictiveness of policy.

When will rates fall?

Westpac isn’t expecting interest rates to fall in the very near future, but does believe that the first cut will come in 2024.

Ellis advised that the Westpac economic team “expect the first rate cut no earlier than September.” This would take the cash rate to 4.1%.

The good news is that Westpac then expects further cuts to 3.85% by December, 3.6% by March 2025, 3.35% by June 2025, and then finally 3.1% by September 2025.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor James Mickleboro has positions in Westpac Banking Corporation. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has no position in any of the stocks mentioned. The Motley Fool Australia has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/ajJR4mv

Building a diversified portfolio of ASX shares and exchange-traded funds (ETFs) is one of many different ways to invest in the Australian economy.

Given the choice, my preference right now would be to invest in Washington H. Soul Pattinson and Co. Ltd (ASX: SOL) shares. This appeals to me more than buying into an ETF such as the Vanguard Australian Shares Index ETF (ASX: VAS).

Now, the VAS ETF is not a bad investment. It has plenty of positives, including diversification, dividend yield and franking credits, and a low management fee. Investing in the Vanguard Australian Shares Index ETF can work well as a strategy for people wanting to take a more passive hand-off investment approach.

But I’d prefer to buy Soul Patts shares for a few different reasons.

Concentrated investments

I like that, as an investment house, Soul Patts has flexibility in its choice and allocation of investments, depending on the size of the opportunity.

Its biggest strategic positions include TPG Telecom Ltd (ASX: TPG), New Hope Corporation Ltd (ASX: NHC), Brickworks Limited (ASX: BKW), Pengana Capital Group Ltd (ASX: PCG), Apex Healthcare, Tuas Ltd (ASX: TUA) and Aeris Resources Ltd (ASX: AIS).

The VAS ETF is heavily invested in a small number of miners, banks and others, while its allocation to smaller businesses is very limited.

I like that Soul Patts has the freedom to allocate its capital wherever it likes. In its FY23 presentation, it described its investment style as “active and thoughtful” with an “unconstrained mandate”, and it did not invest to replicate any index.

I think concentrated investments in the right areas can lead to portfolio outperformance for Soul Patts shares.

Defensive setup

Soul Patts invests heavily in a number of industries that can provide defensive and resilient cash flows.

Banking and retailers, which make up a sizeable portion of the S&P/ASX 300 Index (ASX: XKO), are not defensive in my mind if a recession comes along. Miners are not exactly resilient in all conditions, but they can provide returns that are largely uncorrelated to the rest of the market.

Soul Patts invests in fairly defensive/uncorrelated areas like telecommunications, resources, swimming schools, property, healthcare, agriculture and more.

Strong dividend income

The VAS ETF typically offers a good dividend yield, but the distributions are not consistent. That’s mostly because an ETF passes through the investment income it receives, and dividends from the underlying holdings can change year to year â just think about how the BHP Group Ltd (ASX: BHP) dividend has bounced around.

Soul Pattinson has grown its dividend every year since 2000. While its starting dividend yield isn’t as high as the VAS ETF, the dividend is consistently growing. Having said that, growth is not guaranteed.

Soul Patts shares have outperformed

Past performance is not a guarantee of future returns, but Soul Patts’ portfolio has done well at beating the market over time.

At July 2023, the end date of its FY23 result, it said its total shareholder return (TSR) was 11.3% per annum over five years, 12.4% per annum over 10 years and 12.5% over 20 years, beating the All Ordinaries Accumulation Index (ASX: XAOA) return by 3.6%, 3.9% and 3.5% per annum, respectively.

I think Soul Patts’ investment choices now and in the future can enable it to deliver outperformance over the next decade. For example, in recent times, it has ramped up its investments in credit, unlocking equity-like returns.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Motley Fool contributor Tristan Harrison has positions in Brickworks and Washington H. Soul Pattinson and Company Limited. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Brickworks and Washington H. Soul Pattinson and Company Limited. The Motley Fool Australia has positions in and has recommended Brickworks and Washington H. Soul Pattinson and Company Limited. The Motley Fool Australia has recommended Tpg Telecom. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/ZAKzqrn

When it comes to buying ASX dividend shares, some beginner investors are seduced by the lure of high payouts. But there’s much more to picking the right passive income stocks for your portfolio than just dividend yield.

Is the company retaining enough profit to reinvest for future growth? Are its dividends sustainable? Does the stock have a decent track record of growing its shareholder payouts? Is the yield rising sharply on the back of recent share price falls, and if so, why are investors selling? And so it goes on…

To help sort the income-stock treasure from the traps, we asked our Foolish writers which ASX dividend shares they think should be on your buy list right now. Here is what the team came up with:

7 best ASX dividend shares for February 2024 (smallest to largest)

Why our Foolish writers love these ASX passive income stocks

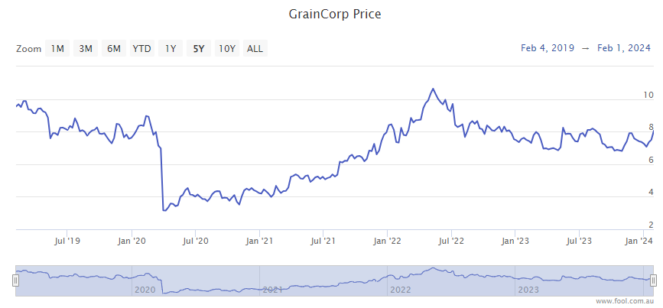

Graincorp Ltd

What it does: GrainCorp is a 100-year-old agribusiness and processing company that connects growers and producers with local and international customers. It manages a wide range of grains, pulses, oilseeds, biofuel components, animal feeds, and oils and shortenings used in food production.

By Bronwyn Allen: I used CommSec’s stock screener to identify the S&P/ASX 200 Index (ASX: XJO) stock with the best five-year growth rate for dividends. Up came Graincorp shares with an impressive 82.3% growth rate over five years and 22.1% over 10 years.

Among the nine analysts covering the stock on CommSec, five rate Graincorp a strong buy, three a hold, and one a strong sell.

While the long-term dividend growth rate is great, ag stocks can be volatile. The consensus expectation for Graincorp dividends in 2024 is 30.8 cents per share, well down on the 54 cents paid last year.

However, on today’s share price of $7.92, 30.8 cents still equates to a reasonable dividend yield of 3.9%, plus 100% franking.

Motley Fool contributor Bronwyn Allen does not own shares of Graincorp Ltd.

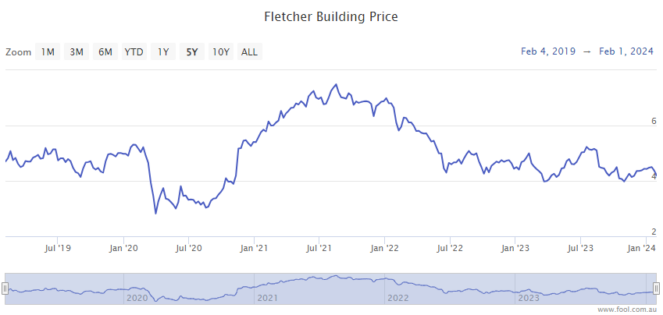

Fletcher Building Ltd

What it does: Fletcher Building is a New Zealand company that makes and distributes construction materials.Â

By Tony Yoo: This Kiwi outfit has been a consistent dividend payer over the past four years. The yield is already excellent at 7.4%, but if you include supplemental distributions, that is bumped up to 8.5%.

The cyclical nature of the construction industry is such that now might be a cheap time to buy a stock like Fletcher Building before the real estate market heats up from interest rate cuts. The current share price is around 19% off last August.

Pleasingly, revenue, operating margin and net profit before abnormals have all trended up over the past four financial years. According to CMC Invest, nine out of 11 analysts currently believe Fletcher Building shares are a buy.

Motley Fool contributor Tony Yoo does not own shares of Fletcher Building Ltd.

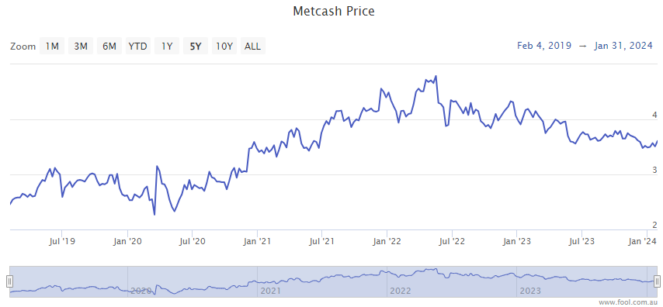

Metcash Limited

What it does: Metcash distributes food and drink to independent supermarkets and liquor stores around the country, including IGA supermarkets, IGA Liquor, Cellarbrations, The Bottle-O, Porters Liquor, Thirsty Camel, Big Bargain Bottleshop, and Duncans. It also has a hardware division that owns Mitre 10, Home Timber & Hardware, and Total Tools.

By Tristan Harrison: A number of ASX dividend shares have rallied in the last few weeks and months, reducing their dividend yields, but Metcash hasn’t seen that, making it look much better value relative to others.

Using Commsec forecasting, Metcash is projected to pay a very healthy grossed-up dividend yield of around 8%.

Furthermore, I think Metcash is one ASX stock that could strongly benefit from potential interest rate cuts, which could lead to stronger demand for its hardware division. Before economic conditions weakened, the hardware division was the most profitable, so a rebound in demand would be very helpful.

Population growth is also a useful tailwind for Metcash, with more people equating to more households and potential customers. The company recently announced it’s in the running to acquire Superior Food Group, which could further boost earnings.

In my opinion, the Metcash share price is good value. It’s priced at 13x FY24’s estimated earnings.

Motley Fool contributor Tristan Harrison owns shares of Metcash Limited.

Super Retail Group Ltd

What it does: Super Retail Group is a retailing conglomerate behind the popular Rebel, Super Cheap Auto, Macpac, and BCF chains.

By Sebastian Bowen: I’ve long been impressed with the performance of Super Retail Group. Sure, this company does operate in the usually-cyclical consumer discretionary sector. However, its stores — particularly Super Cheap and BCF — are famously recession-resistant.

Its recent numbers also suggest resistance to both high inflation and high interest rates, too. This alone makes it a good candidate for a dividend investor, in my view.

But what’s really caught my eye this February is Super Retail’s chunky dividend. At recent pricing, this company offers investors a yield close to 5%, which typically comes with full franking credits attached for an added bonus.

As such, I think you could do far worse than this company for a passive income investment today.

Motley Fool contributor Sebastian Bowen does not own shares of Super Retail Group Ltd.

NIB Holdings Limited

What it does: NIB is a private medical insurance provider to residents of Australia and New Zealand. After privatising in 2007, the company has grown to serve more than 1.5 million people. NIB also has a substantial presence in travel insurance and National Disability Insurance Scheme (NDIS) plan management.

By Mitchell Lawler: Jostling with heavyweights, such as Medibank Private Ltd (ASX: MPL) and Bupa, the smaller NIB has managed to grow at an above-industry rate for the last 20 years.

Dividends are dependent on profits. The business continues to report strong policyholder growth and attractive net margins. In particular, the international inbound health insurance segment posted a 15.7% policyholder increase in FY23, delivering a sensational net margin of 13.1%.

Furthermore, the core Australian resident offering continues to expand, increasing its policyholder count by 4.7% in FY23. As immigration into Australia surges, NIB could be well-positioned to reap the rewards.

Investors can secure NIB shares on a 3.6% dividend yield right now. It may not be quite as generous as other alternatives. However, I believe this company’s dividends have plenty of room to grow.

Motley Fool contributor Mitchell Lawler does not own shares of NIB Holdings Limited.

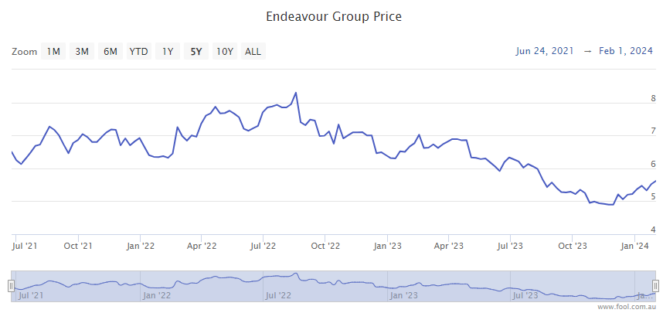

Endeavour Group Ltd

What it does: Endeavour is the drinks giant behind the BWS and Dan Murphy’s brands, as well as a large network of hotels/pubs.

By James Mickleboro: I think Endeavour would be a great ASX dividend share to buy due to its leadership position in a market that has defensive qualities.

In addition, the company still has plenty of growth opportunities. It added 39 retail stores to its network in FY 2023, bringing its network to 266 Dan Murphy stores and 1,435 BWS stores. While these may sound like large numbers, management isn’t stopping there, with plenty more store openings planned.

Goldman Sachs expects this to underpin the payments of fully-franked dividends per share of 21 cents in FY 2024, 23 cents in FY 2025, and 25 cents in FY 2026. This will mean yields of 3.8%, 4.2%, and 4.5%, respectively.

The broker also sees value in Endeavour shares at current levels. It has a buy rating and $6.40 price target on them. This represents more than 11% upside from Friday’s closing price of $5.74.

Motley Fool contributor James Mickleboro owns shares of Endeavour Group Ltd.

BHP Group Ltd

What it does: BHP is the largest company listed on the ASX. It has top-tier mining operations in Australia, North America, and South America. The diversified resources company earns most of its revenue from iron ore, with copper coming in at number two and coal also providing significant income.

By Bernd Struben: BHP is well known for its reliable, fully franked dividends. And BHP’s share price and dividends are closely aligned with the price of iron ore, which topped US$220 per tonne in mid-2021.

The retrace in the price of the industrial metal in the latter half of 2022 and much of 2023 to below US$100 per tonne also saw BHP’s dividends come down from the all-time highs of late 2021 and 2022.

Though at yesterday’s closing price of $47.61, BHP still trades at a healthy 5.5% trailing yield.

When it comes to the outlook for the iron ore price, I’m in agreement with Citi’s analysts. They see it rebounding to US$150 per tonne (up from the recent US$136 per tonne) in the first quarter of 2024. This would bode well for BHP’s share price and dividends.

Motley Fool contributor Bernd Struben does not own shares of BHP Group Ltd.

Wondering where you should invest $1,000 right now?

When investing expert Scott Phillips has a stock tip, it can pay to listen. After all, the flagship Motley Fool Share Advisor newsletter he has run for over ten years has provided thousands of paying members with stock picks that have doubled, tripled or even more.*

Scott just revealed what he believes could be the ‘five best ASX stocks’ for investors to buy right now. These stocks are trading at near dirt-cheap prices and Scott thinks they could be great buys right now…

Citigroup is an advertising partner of The Ascent, a Motley Fool company. The Motley Fool Australia’s parent company Motley Fool Holdings Inc. has positions in and has recommended Goldman Sachs Group. The Motley Fool Australia has positions in and has recommended NIB Holdings and Super Retail Group. The Motley Fool Australia has recommended Metcash. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

from The Motley Fool Australia https://ift.tt/zJfERox