The Australian government is ramping up efforts to support the domestic holiday industry, but ASX travel stocks aren’t responding.

Tourism Australia launched its “Holiday Here This Year” campaign to convince Aussies to take local holidays while international borders are shut, reported Business Insider.

It’s hoped the campaign will keep the tourism sector out of intensive care as COVID-19 decimated the industry.

No reprieve for Flight Centre share price

But investors aren’t impressed with ASX travel stocks tanking. The Flight Centre Travel Group Ltd (ASX: FLT) share price tumbled 6.5% to $13.45 in after lunch trade.

The Webjet Limited (ASX: WEB) share price is only faring a little better with a 4% drop to $4, while Qantas Airways Limited (ASX: QAN) share price declined 1.3% to $4.24.

In contrast, the S&P/ASX 200 Index (Index:^AXJO) is trading at breakeven with healthcare and tech stocks supporting the market.

Many losers and few winners in ASX travel sector

However, the underperformance of the Flight Centre share price is understandable. Holiday makers typically use the travel agent to make complicated multi-stop holidays. These tend to be overseas locations.

While Webjet is also more exposed to overseas travel, it’s a little better placed to capture the domestic air travel and accommodation market.

Qantas shareholders are also hoping local holidaymakers will help support the airline’s bottom line too.

Tourism Australia’s latest campaign

There’s no mention of how much money the federal government is throwing behind the campaign. But Tourism Australia contracted comedian Hamish Blake and entrepreneur Zoe Foster-Blake to be the faces of the movement.

The celebrities will be spruiking locations arounds Australia that have been popular with international tourists.

The national drive will complement initiatives undertaken by state governments around the country. These include Tasmania’s “Make Yourself at Home” program, where residents can claim back what they spent on accommodation and travel experiences in the state.

The Northern Territory has a similar initiative that rebates travellers up to $200 for every $1000 they spend on travel bookings.

Foolish takeaway

The campaign could make a big difference to small and medium sized businesses that rely on tourists, but its unlikely to have much of an impact on most ASX stocks.

Even leisure facilities owner Ardent Leisure Group Ltd (ASX: ALG) isn’t responding favourably to the news today with its share price slipping 1.6% to 62 cents.

Given the big dent left by the coronavirus, no one government initiative can offset the damage.

These Dividend Stocks Could Be Your Next Cash Kings (FREE REPORT)

Motley Fool Australia’s Dividend experts recently released a brand-new FREE report revealing 3 dividend stocks with JUICY franked dividends that could keep paying you meaty dividends for years to come.

Our team of investors think these 3 dividend stocks should be a ‘must consider’ for any savvy dividend investor. But more importantly, could potentially make Australian investors a heap of passive income.

Don’t miss out! Simply click the link below to grab your free copy and discover these 3 high conviction stocks now.

Click Here For Your Free Stock Report

Returns As of 6th October 2020

More reading

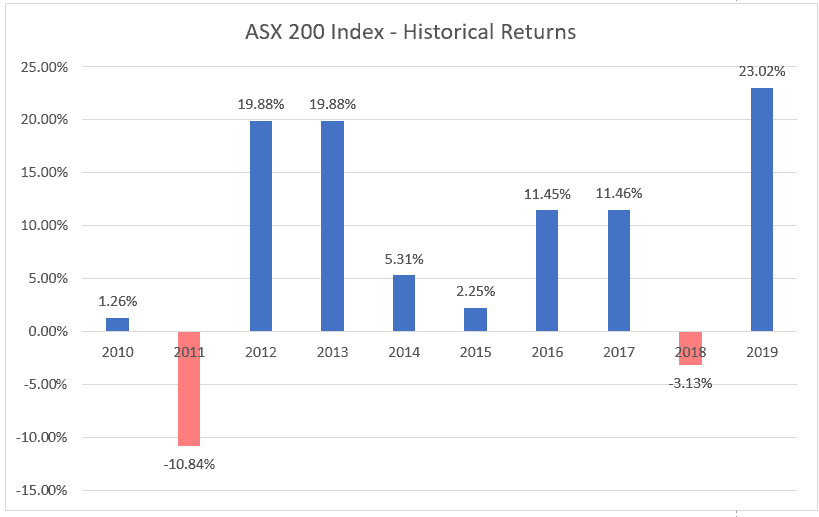

- Here are 10 years of ASX 200 historical returns

- Ramsay (ASX:RHC) share price firms as its UK hospitals reopen to private patients

- Why Brickworks, Flight Centre, Whitehaven, & Zip shares are dropping lower

- ASX 200 flat: Bank of Queensland impresses, CSL guidance update, AUSTRAC clears Afterpay

- Why ASX gambling shares like PointsBet (ASX:PBH) have surged in 2020

Motley Fool contributor Brendon Lau owns shares of Webjet Ltd. The Motley Fool Australia owns shares of and has recommended Webjet Ltd. The Motley Fool Australia has recommended Flight Centre Travel Group Limited. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy. This article contains general investment advice only (under AFSL 400691). Authorised by Scott Phillips.

The post Why the Flight Centre (ASX:FLT) share price slumped despite new tourism campaign appeared first on Motley Fool Australia.

from Motley Fool Australia https://ift.tt/33TMSoc